$1 ≠ $1

Even Buffett falls for it.

Is $1 equal to $1?

I hope your brain says “yes.” I’m sure your actions say “not really.”

Buffett, Munger, Lynch, etc. No one is immune.

The bias doesn’t disappear with experience. It just wears a different disguise.

A short walk is all it takes to see it.

No Country for Old Men

You’re out for a quiet walk.

It’s summer. The hot wind stimulates your sudoriparous glands, when suddenly you spot a $100 bill on the ground.

Being naturally anxious, you hesitate. What if it belongs to the wrong person? A dealer. Or a psychopath. These days, who knows.

Decision made. You leave it right there. Either way, you didn’t lose anything and you didn’t gain anything. So everything’s fine.

Except it isn’t.

In reality, your anxiety just made you $100 poorer. An anchoring bias made you compare your new empirical wealth to your wealth from a now-dead past.

But the moment that $100 entered the equation, your baseline shifted. Finding it raised your potential wealth by $100. Walking away cost you that $100 of potential.

Anchoring, loss aversion, and regret aversion aside1:

Not earning $1 = Being $1 poorer

Not losing $1 = Being $1 richer

And that’s the point: you’re about to lose millions (maybe billions) of dollars you’ll never earn. The more you trade (buy/sell), the more you’ll lose.

For better and for worse.

I Love You… Me Neither

The moment you buy a stock, you’re buying a range of futures.

Your potential wealth now includes whatever that stock can still become

The moment you sell, you collapse that range into a single outcome.

That’s why your realized path will almost always lag behind your full set of potential paths, which brings us to this hard-to-swallow equation:

Empirical Wealth ≤ Theoretical Wealth.

To turn ≤ into =, you’d need to sell only when the stock’s remaining upside is worse than your best alternative, every time. Which is literally impossible, you’ll agree.

The whole investing game is making decisions that:

maximize your potential wealth (your analysis skills),

while minimizing the gap between theoretical and empirical wealth (your psychological skills).

But you’re playing the I Love You… Me Neither game against a serious opponent: the asymmetry of stock returns (max loss = -100%, while max gain → +infinity):

I love you: own a multi-bagger that compounds for decades.

Me neither: selling it too early for a lower-performing stock blows up your opportunity cost.

If you’ve been investing long enough, you probably have a few scars that never fully healed

Investing is Choosing Our Regrets

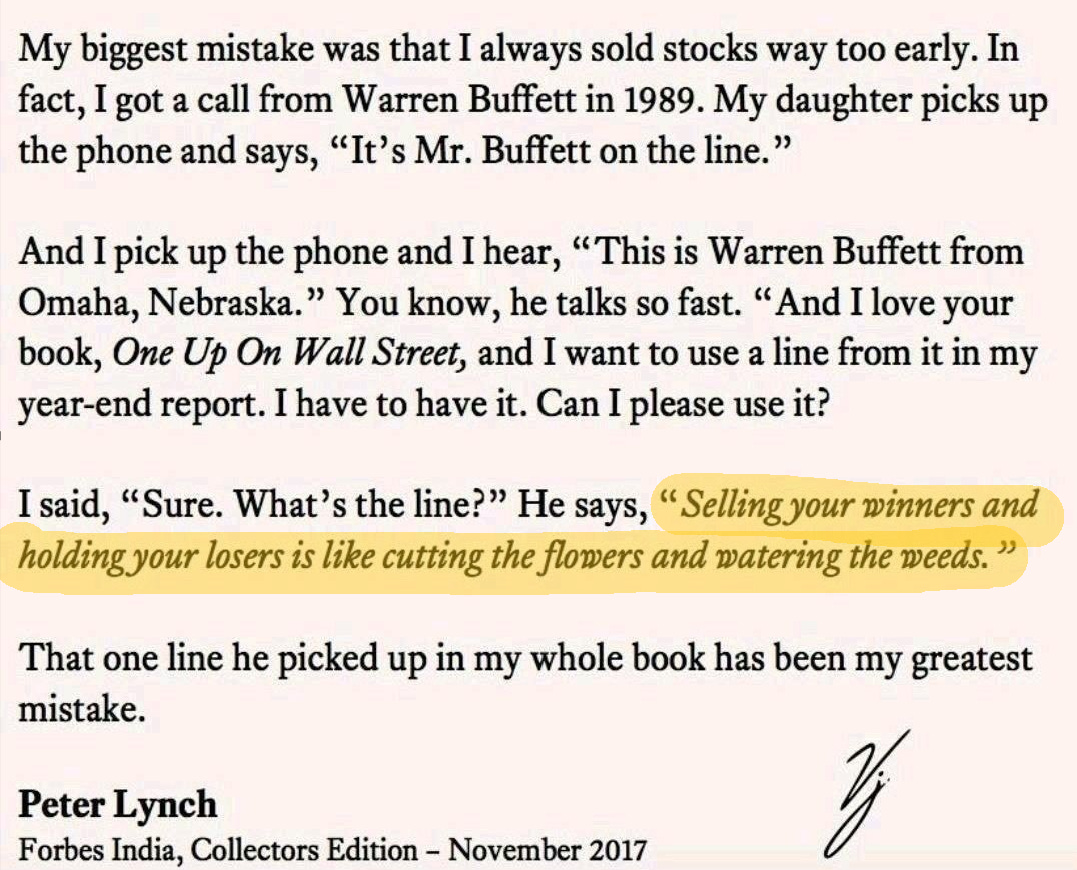

Peter Lynch has a perfect story for this.

This isn’t just Peter Lynch’s greatest mistake. It’s the biggest mistake of many of the greatest investors:

Buffett bought Berkshire Hathaway out of ego, calling it his “dumbest stock,” and estimated the opportunity cost at $200B by his own math (see the interview).

Peter Thiel invested very early in Facebook, taking a 10% stake for $100k. He cashed out at the IPO for $2B, which would be $100B today.

SoftBank bought 5% of Nvidia in 2017, sold after a 20-30% drawdown in 2019 for $3B. Today, it would be $200B, more than SoftBank’s market cap.

Those mistakes cost them far more than their “empirical” losses. And it’s always the same culprit: the asymmetry of gains.

And for us too, mere mortals, it’s often the #1 source of value destruction.

So I decided to follow Sun Tzu’s advice: “If you know neither your enemy nor yourself, you will be defeated in every battle.”

And even if I don’t have Peter Lynch’s phrasing, I do have tools he didn’t have back then: a lot of data, and a lot of compute.

Perfect for getting to know a mathematical enemy.

Do the Maths

To really see opportunity cost in all its forms, I simulated hundreds of millions of portfolios to answer four questions:

How does opportunity cost show up, and how does it grow?

How does it change depending on the portfolio’s structure?

How do buying and selling decisions impact it?

What, concretely, reduces it?

These simulations gave me some very surprising results, and they’ll have a direct impact on my investment process, without question.

Here’s the full analysis.

I Studied Millions of Portfolios. Here's What Actually Kills Compounding

Opportunity cost is one of the most destructive forces in investing. It is also one of the most overlooked.

Take care,

Flo

Anchoring is the tendency to rely too heavily on an arbitrary reference point (a “benchmark”) and adjust insufficiently from it, making subsequent comparisons and judgments less relevant.

Loss aversion is the tendency to feel losses more intensely than equivalent gains, which leads people to make decisions that are irrational relative to expected value.

Regret aversion is the tendency to choose the option that minimizes the chance of future self-blame, avoiding decisions that could feel regretful, even when they’re objectively superior.

the important thing is the amount of companies you can own for years if not decades are very small. Buffett's avg. holding period is ~5 years. sure the Cokes, Costcos, Fairfax Financials I would be fine owning for years but it's a small universe.

that being said Nick Sleep's line on opportunity cost is one of my favourites “the biggest error an investor can make is the sale of a Microsoft in the early stages of the company's growth. mathematically this error is far greater than the equivalent sum invested in a firm that goes bankrupt. the industry tends to gloss over this fact, perhaps because opportunity costs go unrecorded in performance records.”