10 Charts, 10 Lessons: The 2026 Investor’s Reality Check

To be honest, a few of these charts come with multiple lessons.

2025 was a masterclass in noise and uncertainty. 2026 is shaping up to be another.

Clear thinking grounded in real data is the only compass that helps us navigate these choppy, twisting waters.

Here are 10 charts to help you stay clear-headed when it counts.

Narrative Follows Price.

All-Time Highs Are Common, and Few Lead to Deep Drawdowns.

Returns After All-Time Highs ≥ Returns at Any Other Entry Point.

Never, Ever Stop Compounding.

Opportunity Cost Is Often The Biggest Cost.

Drawdowns Are Inevitable.

Even with a portfolio built knowing all returns over the next five years (and reset every five years), you’d still experience 50% drawdowns.

That’s the ultimate proof that:

Volatility is intrinsic to markets and, in many ways, the price of long-term performance.

In investing, the real risk isn’t volatility; it’s permanent loss of capital.

The Deeper the Drawdown, the Longer the Recovery (for Those That Recover).

The Market Always Gives You “Good” Reasons To Sell.

Bull Markets Beat Bear Markets.

Don’t Pay Attention to Strategists or Price Predictors.

So-called “strategists” often do little more than extrapolate the recent past into the future, repackaging what the consensus already believes.

Look at how they cut their estimates after prices fell amid tariff fears, and then raised them again after the market rebounded. They’re reacting to price, not forecasting it.

Most “forecasts” are shaped by career incentives: it’s safer to be wrong with everyone than to be wrong alone, even if the consensus is wrong more often than not.

If you’re investing your own money, you need your own view.

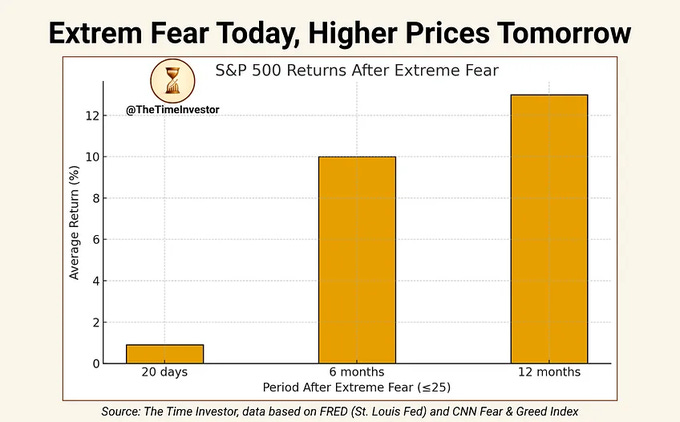

Be Greedy When Others Are Fearful.

And voilà. I hope this added a bit of perspective.

Thank you for your time and attention.

Well done to those who noticed there weren’t 10, but 11 charts.

Sincerely,

The Time Investor

Regarding the chart being out of bubble usually is more costly, doesnt it only apply to investing in the index? Investors didn’t get their money back in Cisco after 25 years if invested during the height of the previous bubble. For active investors aiming for above average returns, their holdings will not represent the market. Therefore, I believe this doesn’t apply to them.

I think market valuations (such as price-to-book ratio, EV/EBIT, etc.) are quite indicative of the next 5-10 years. High valuations mean lower returns in the future and vice versa.

The high valuations in the US mean, for example, that it may better in the long term to invest in cheaper global stock markets. We saw this in 2025, when many global markets in USD had significantly better returns than the US stock market.