Simplify and Conquer

The François Rochon Way.

Would your portfolio have performed better in 2025 if you had been forbidden to touch it since December 31, 2024?

For many investors, the answer is yes. The longer the period, the higher the odds that the answer becomes “yes.”

That’s because the distribution of opportunity costs is far more asymmetric than the distribution of capital costs.1

Translation: thousands of hours analyzing companies and sectors, writing theses, building valuation models. All that, only to destroy value in the end.

Incredibly frustrating, isn’t it? But what if it’s actually liberating?

This phenomenon stems from a very specific property: the quality of the output doesn’t directly depend on the quality and quantity of the inputs.

In our investing world: performance doesn’t depend on hours worked. When you think about it, that’s an extremely rare phenomenon in nature. But that’s exactly what makes investing so unique, and so liberating.

From that property comes an incentive with incredible power: simplify, simplify, and simplify.

If we take it a step further, it’s an incentive to build an investing process that is both:

as simple as possible without sacrificing relevance, and

explicit and repeatable, so you can refine it over time through feedback (without adding complexity).

That’s exactly how François Rochon thought about it, and acted. Result:

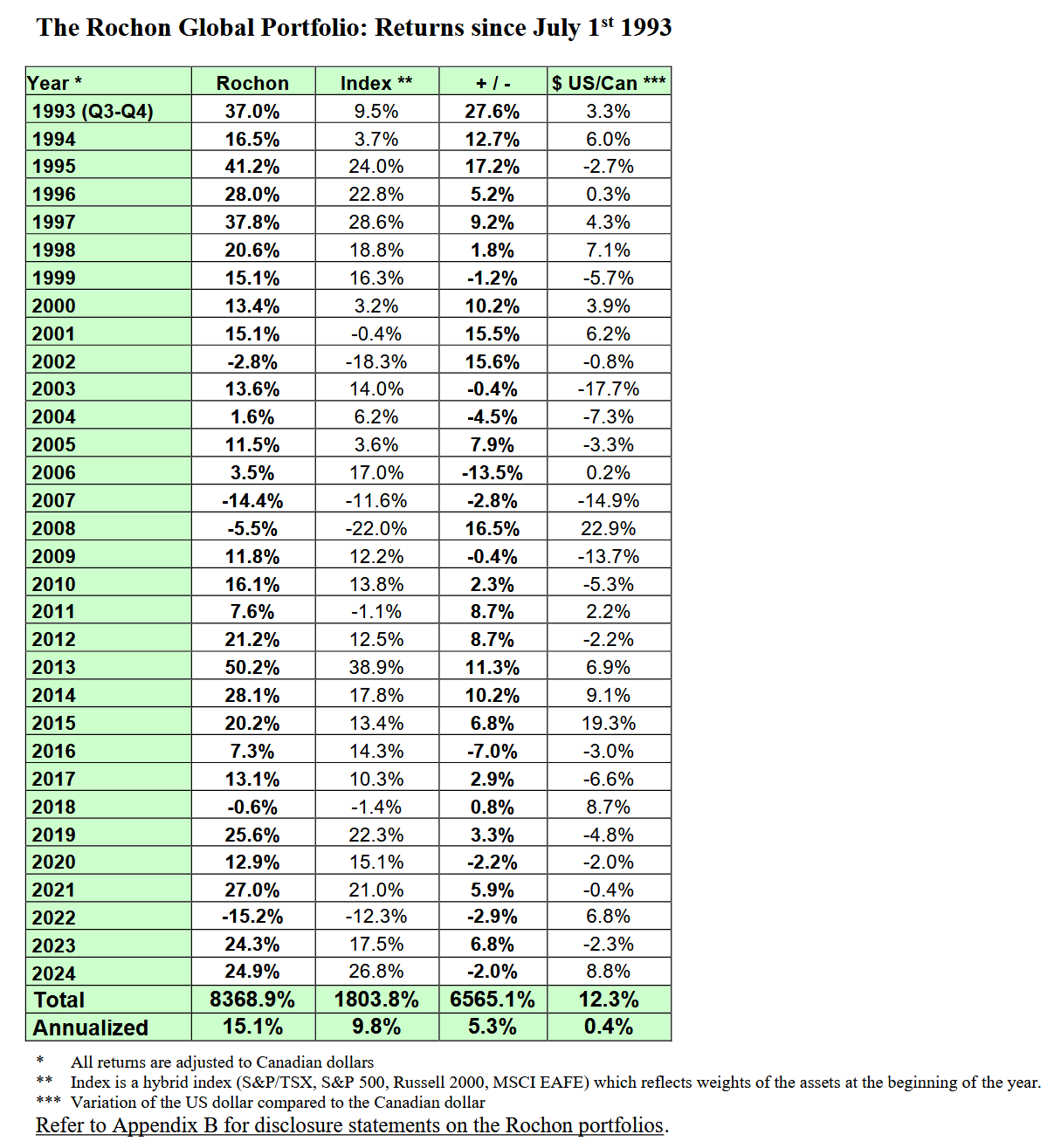

15.1% annualized for 30 years

Worst calendar-year drawdown: -15.2% (2023)

Better yet: he shared his entire strategy in 2017 in a one-hour Talks at Google (and it has surprisingly few views).

The advantage of a simple system is that it takes five minutes to explain.

1. The Foundations: Invert? Always invert

“Index ETFs.” Some of you thought it so loudly while reading the intro that I heard you from the future.

Yes, it’s an excellent way to simplify things and earn “acceptable” returns. But no. François Rochon doesn’t want acceptable returns.

In fact, his core premise is precisely that he does not want the performance of his benchmark, the S&P 500. He’s aiming for 15% per year.

To get there, he studies the best by asking what he would have to do to achieve market returns… and then he does the opposite.

That leads him to 3 simple ideas, but ones he takes very seriously:

To own a few selected companies

To develop the right behaviors (rationality, humility, and patience)

To be able to think for himself

2. The Art of Science & The Science of Art

As a trained engineer with a passion for art, François Rochon approaches investing through both lenses.

For him, the “science” side is the “Stock Selection Process”. And the advantage of an explicit process is that it’s easy to lay out.

Here is François Rochon’s Stock Selection Process (verbatim):

Financial Strength

ROE > 15%

EPS growth > 10%

Debt/Profit Ratio < 4x

Business Model

Market Leader

Competitive advantages

Low cyclicality

Management Team

High level of ownership

Constructive acquisitions

Good capital allocation

Market Valuation

5-year valuation model

Try to purchase at half the estimated value in 5 years (≈15% annual return)

If you’re thinking: “Wait, how do you judge a competitive advantage? That’s not as measurable as ROE or low cyclicality,” congratulations: you’re exactly right. And you’ve just handed me a perfect transition.

That’s where art fills in the gaps left by science (in this context only!).

According to François Rochon, competitive advantage isn’t something you can fully objectify, it’s something you recognize when you see it.

His method is to find what he calls “masterpieces”: rare, unique businesses (pieces of music) where the presence of a competitive advantage (the quality of the work) is so obvious that almost no one can reasonably deny it.

Examples he gives: IKEA, GEICO, Apple, McDonald’s, Gillette, The Washington Post, Disney, National Cash Register Co., etc.

This system stays simple by drastically shrinking Rochon’s investment universe. In 2017, that universe was limited to 125 companies.

We’ve covered the “business” side of investing. Now let’s move to the main component: psychology.

3. His Behavioral Edges

If you spend any time on social media, you’ve definitely run into people giving all kinds of advice about “behavioral edge”: mindset, discipline, “controlling your emotions,” etc.

The problem is that this kind of advice is often more useful to the people who write it than to the people who read it. (And I include myself in that.)

However, none of the advice-givers out there has a track record as exceptional as Rochon’s over 30 years (and yes, I include myself again.)

So I’ll point out that even if Rochon’s advice sounds… basic, it’s probably deeper than it looks.

To avoid misrepresenting his thinking, I’ll quote François Rochon directly on each of his behavioral edges.

Humility

We do not believe that we can predict macroeconomic events.

One key element is to define our circle of competence2 and to know where are the limits of its circumference.

We recognize our mistakes and try to always strive for improvement.

A small detail: François Rochon includes a “podium” of mistakes in every letter to his partners.

Beyond the humility and honesty that takes, it’s also a goldmine for any investor who wants to learn from other people’s mistakes. That will be a future post.

Rationality

We try not to be affected when others make more money than us in stocks.

We try to be impervious to stock market quotations in the short term

We accept that we don’t know the future and focus on what we can have some control (our own process).

Even though he didn’t include it in the “rationality” section, this quote captures the essence of Rochon’s rationality for me:

“We believed that if we owned great companies run by great managers, things would work out in the end. They did. So we’re going to keep doing that.”

Thanks to François, there’s no need to wait 30 years to validate the idea. It worked, and it still works.

It seems reasonable to bet that it will keep working.

Patience

Patience is not the ability to wait, but the ability to keep a good attitude while waiting.

However, patience is not the same thing as being stubborn.

To avoid that mistake as much as possible, the good attitude is to focus on what is happening to the company, not the stock.

From these three tendencies emerges a broader one, something many great investors preach, and Sir John Templeton captured perfectly:

“To obtain better results than the others, you must do something different from the others.”

4. I Am, Therefore I Think for Myself

This trait is inevitable: it’s baked into the very origin of François Rochon’s investing system.

When he asks himself what to do to avoid average returns, he imposes an implicit condition: act differently.

And to act differently, you have to think differently. Paraphrasing him a bit, that becomes: be impervious to fads and popular beliefs. Don’t be afraid to underperform your peers for a while.

François Rochon has held positions that underperformed for years. Positions that were hated by the public, before watching them explode in a matter of months.

Few investors have a mindset as independent and as consistent as François Rochon. Let me show you:

“Good businesspeople are like artists: they build with passion, they create something innovative and unique, and they aim to make it last, something that inspires others. My job, then, is to estimate what that remarkable business should be worth and try to buy it at roughly half of what I believe it can trade for in five years if things go as planned, about 15% a year.”

Sounds like a slightly trivial summary of the post, doesn’t it? This is an excerpt from something François Rochon wrote in 2005.

The video I used as a reference for this post is from 2017. He’s still applying the same strategy today.

To me, it’s the clearest sign that his performance came from his ability to think for himself consistently, for decades, without being stubborn in the face of reality.

And voilà. Full circle.

We’ve just seen the three pillars of his strategy:

To own a few selected companies

To develop the right behaviors (rationality, humility, and patience)

To be able to think for himself

One last question to close.

What’s stopping you from following his system, or even following his positions directly, to get closer to his performance?

That’s the kind of question every investor should answer honestly.

Personally, I want to take advantage of the fewer constraints that come with a smaller capital base to aim for more than 15% a year. (At least until the next real bear market. I’m joking, but…)

That’s my answer. What’s yours?

I’ll leave you alone with your honesty.

(And a quick reminder: Part 2 of my series 50 Ideas to Think Like a High-Level Generalist comes out on Sunday.)

Take care.,

Flo

Losses compound with a maximum cost of -1x, while missed gains can easily add up to 10x, 20x, 100x, etc., over decades.

The circle of competence is defined here as the boundary beyond which the effort required to learn and understand is no longer worth the potential upside (too uncertain, too complex, too widely known, etc.).

For me, this also raises the question of which stock market to invest in at all. Currently, I'm quite attracted to the Japanese stock market, as deeply undervalued stocks can be found there. Many of these companies also hold substantial cash and financial assets on their balance sheets.

Additionally, the Tokyo Stock Exchange is now requiring companies trading below book value to publish plans for improving their capital efficiency – which adds an interesting catalyst for value realization. Furthermore, the risks regarding balance sheet manipulation and governance seem very low to me. Further, the 6 -12 month momentum of these stocks is strong. About 700 stocks alone may trade at or below 0.5 of book value.

It is almost as good as it gets!

see also here:

https://borjaclavero.substack.com/p/equity-markets-forecast-q4-2025

https://www.gmo.com/europe/research-library/gmo-7-year-asset-class-forecast-4q-2025_gmo7yearassetclassforecast/

Great piece as always.

It's quite impressive that his investment record matches his desired return on a purchase (half of estimated value after 5 years)!

He did the impossible in active management; he did what he said he would.

This is my first time coming across this great investor. Thanks for sharing.