I Let 9,343 IPOs Speak for Themselves. Here's What They Said.

No opinions were harmed in the making of this analysis.

IPOs are bullshit.

IPOs can be great opportunities.

I don’t care about IPOs.

Just like that, a handful of words to please everyone. Or annoy them. Depends on your personality.

At least one of those three got a reaction out of you. That was the point: to make you catch yourself having an opinion. Got it? Good, because we don’t care. Mine included. Opinions are a last resort for when you have no data.

And with IPOs, we have plenty. So check your emotions at the door, shut down the limbic system, and fire up the cortex.

Let’s hear what the data has to say.

On Paper

Normally, this is where I'd find a clever way to say that before you analyze something, you should define it properly. This time, I'll do it by breaking the fourth wall. It’s done. Pardon my impertinence.

Stripped to the facts, an IPO is:

The first sale of a company's shares on a public market. The sellers are the company, its existing shareholders, or most often, both.

A prospectus, written by the company, its lawyers, and its bankers, with a stated purpose: to give investors the information they need to make an informed decision.

One or more investment banks that run the process for a fee: 7% of the deal in most cases.1

Shares sold at the offer price, allocated mostly to institutions. Retail investors, by contrast, buys on the open market, at the market price, starting on the first day of trading. The pop is the gap between the offer price and the first closing price.

Humans, stakes, incentives, and imperfect information. Time to put on our game theorist hats.

Three things jump out:

A timing asymmetry: it's literally the insiders who decide when to go public.

An information asymmetry: the prospectus that’s supposed to tell investors everything they need to know is written by people whose incentive is to sell at the highest possible price.

A power asymmetry: insiders have been shareholders since day one. VCs have been shareholders for 8 to 10 years or so. Most employees have been shareholders for several years. The institutions get to buy at the offer price, just before listing. Retail almost always buys after everyone else.

"Show me the incentive and I will show you the outcome," as dear old Charlie would say. But I find him too realist cynical for this post. I don't need to take selfishness as an axiom. I have data. Plenty of it.

If you like Charlie Munger, irony, microcaps too good to stay microcaps, data-driven analysis, Charlie Munger, or irony, this newsletter is for you.

The Raw Reality

When?

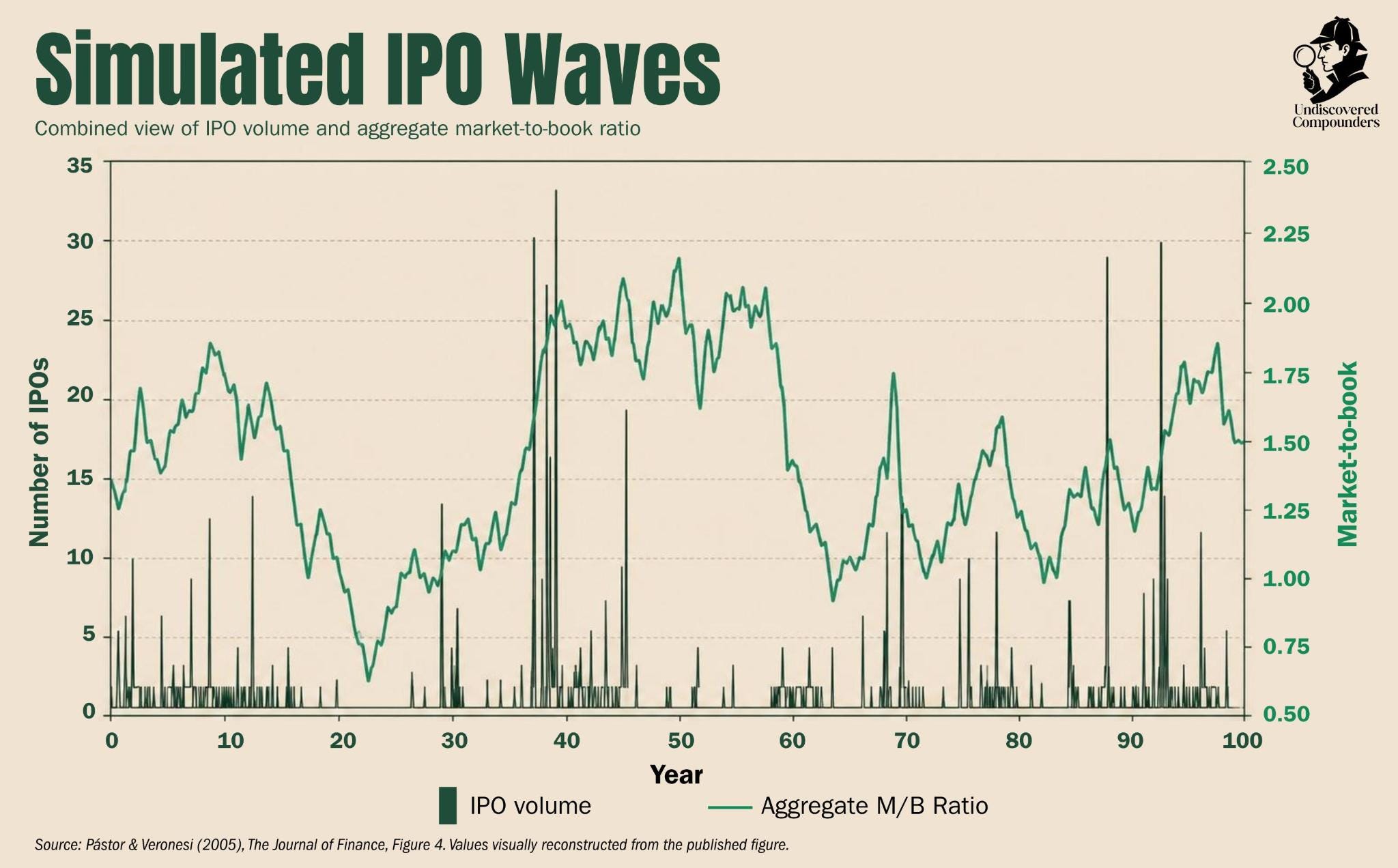

First things first: timing. Here's the number of IPOs plotted against market valuation (market-to-book ratio).

A neutral eye sees three things:

IPOs cluster mainly at valuation peaks.

The sharper the recent rally, the more of them flood in.

When the market falls, locally or globally, they drop off sharply, or vanish outright.

All three boil down to one number: on average, major IPO waves come after a market run-up of about +31% annualized over the two preceding quarters.2

The timing asymmetry clearly favors insiders and VCs.

Whether it's deliberate or not isn't our concern. Their gains don't necessarily mean a loss for retail. An equilibrium where everyone wins is still theoretically possible: insiders, institutions, VCs, and IPO buyers.

Let's test that against reality.

Who Gets What?

Unfortunately, I had trouble finding data that breaks down each player's performance in detail. But there's enough to sketch most of the picture.

Insiders and VCs are usually locked up for six months. When the lockup expires, average trading volume rises 40%, with a -1.5% abnormal return over three days.3 Both the volume and the negative abnormal return are larger when VCs are involved.4

But jumping from that to "VC = predator" is a bit hasty.

First, VC-backed IPOs perform better than smaller, non-VC-backed ones.5 Second, their alpha is highest while VCs stays invested (1.2pp/month) and drops once they exits (0.65pp/month).6 Their contribution to the "community" is real, as long as they're still around.

On insider performance, I found nothing worth noting. As for VCs, their returns tend to track the market, just far more volatile and amplified (beta of 1.9).7

Fortunately, the data is richer for institutions.

Institutions get 3.3x more shares than retail. So the lion's share. No surprise, they're the bigger fish. But the split is asymmetric: institutions receive more shares in underpriced IPOs than in overpriced ones (75% vs 68%), that is, when the pop is fat rather than thin.8

That's the short term. The longer term matters too (a few months out). IPOs with high institutional allocation post a +4pp/month alpha; the low-allocation ones, nothing.9 Yes, per month. That’s not a typo. To say institutions are better served, serve themselves more, or both, on the best deals, is still a neutral read.

But money doesn't wait. Which is why institutions are far less patient than retail: within two days of the IPO, they've flipped 41.5% of their allocation, versus 18.6% for retail.10

The numbers are clear: institutions, too, cash in on their power asymmetry. But it still says nothing about how retail performs.

The Final Problem, Our Final Problem

You’re retail, with retail problems and retail questions. But above all, you’re neutral. So you figure none of the data above gives you even the faintest lead. Bravo, lovely mindset. Especially on a subject this divisive, in a period that’s even more so.

Let’s hear the data instead.

Not Short Term

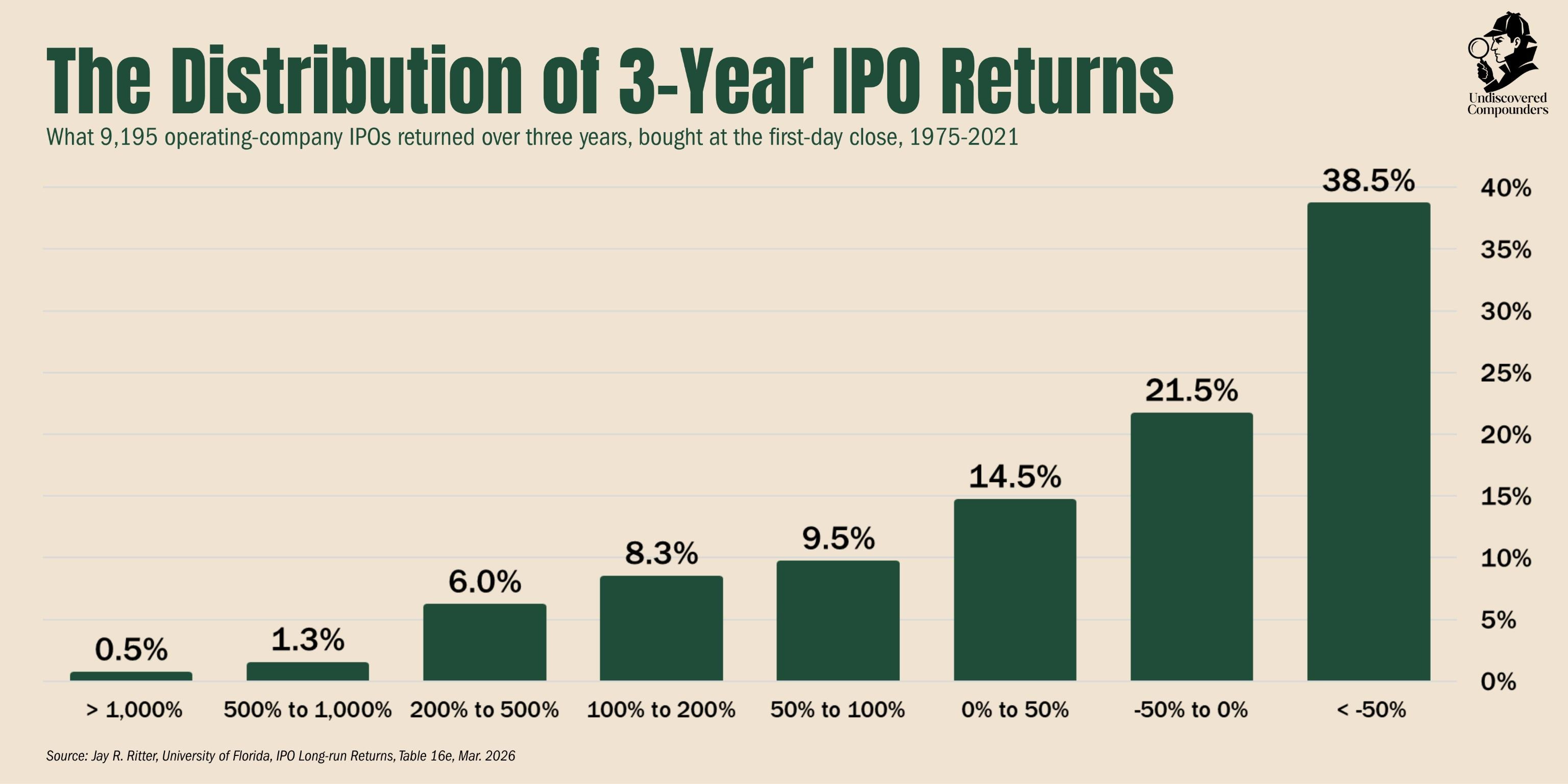

Here's the 3-year performance of more than 9,000 IPOs.

A few key numbers11:

60% of IPOs are in the red at three years.

16.1% are multibaggers after three years.

On average, IPOs return 19.1% over three years, versus 39.6% for the market.

That average is heavily flattered by the 0.5% of firms with exceptional returns: the median falls to -25.7%.

Performance comes down to two variables: size (large = >$100M in sales) and profitability. Here's their average underperformance versus the market over three years:

Small and unprofitable: -40.9%

Small but profitable: -25.9%

Large but unprofitable: -2.7%

Large and profitable: -3.4%

To put it coldly: the 3-year IPO is a losing game on average, worse at the median, and worse still for small companies.

I spent almost as much time writing this piece as I did making these visuals and the ones that follow. Sharing helps spread the knowledge (and makes the time spent on these damn charts worth it too, I'm not gonna lie).

Three years is a long time. Some of you may want a shorter horizon.

Short Term

Institutions are better served on the best deals. The consequence: the retail buyers who do get an allocation get it more often, and in larger size, on the bad ones. The phenomenon is so common it has a name: the winner's curse12 (I didn't pick the name, promise. No judgment, remember).

Fine: retail investors who get an allocation are disadvantaged from the start. But they’re only a small minority of retail : the vast majority buy on the open market.

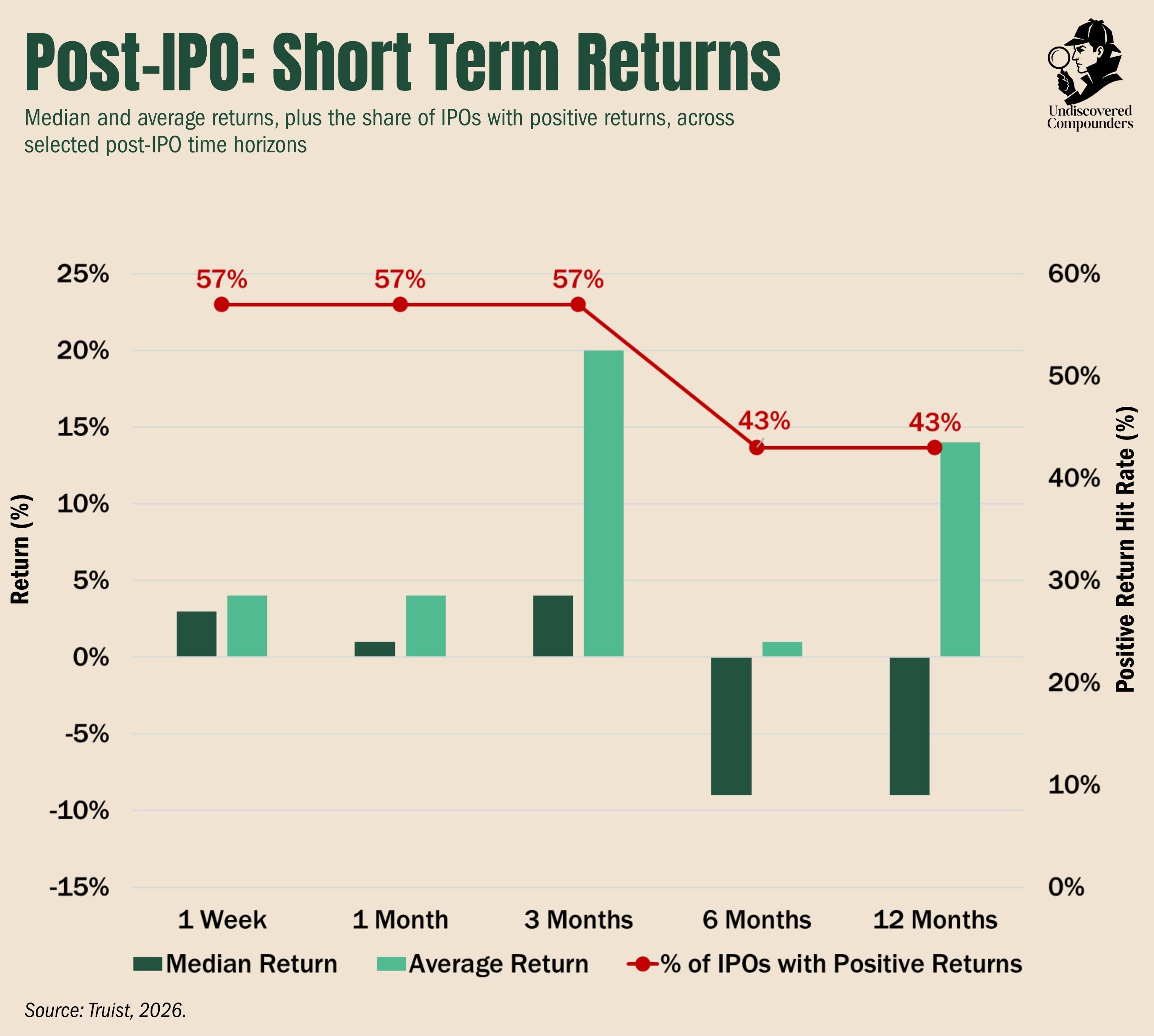

For a very short-term view, here are the numbers on the biggest IPOs over the past 15 years:

Roughly, it's a coin flip: a little more than half of IPOs are in the green early on, a little less after a year. The turning point comes around six months: the share of companies still positive drops from 57% to 43%, and the median return falls with it. That lines up with the end of the insider and VC lockup, and the hype cooling off.13

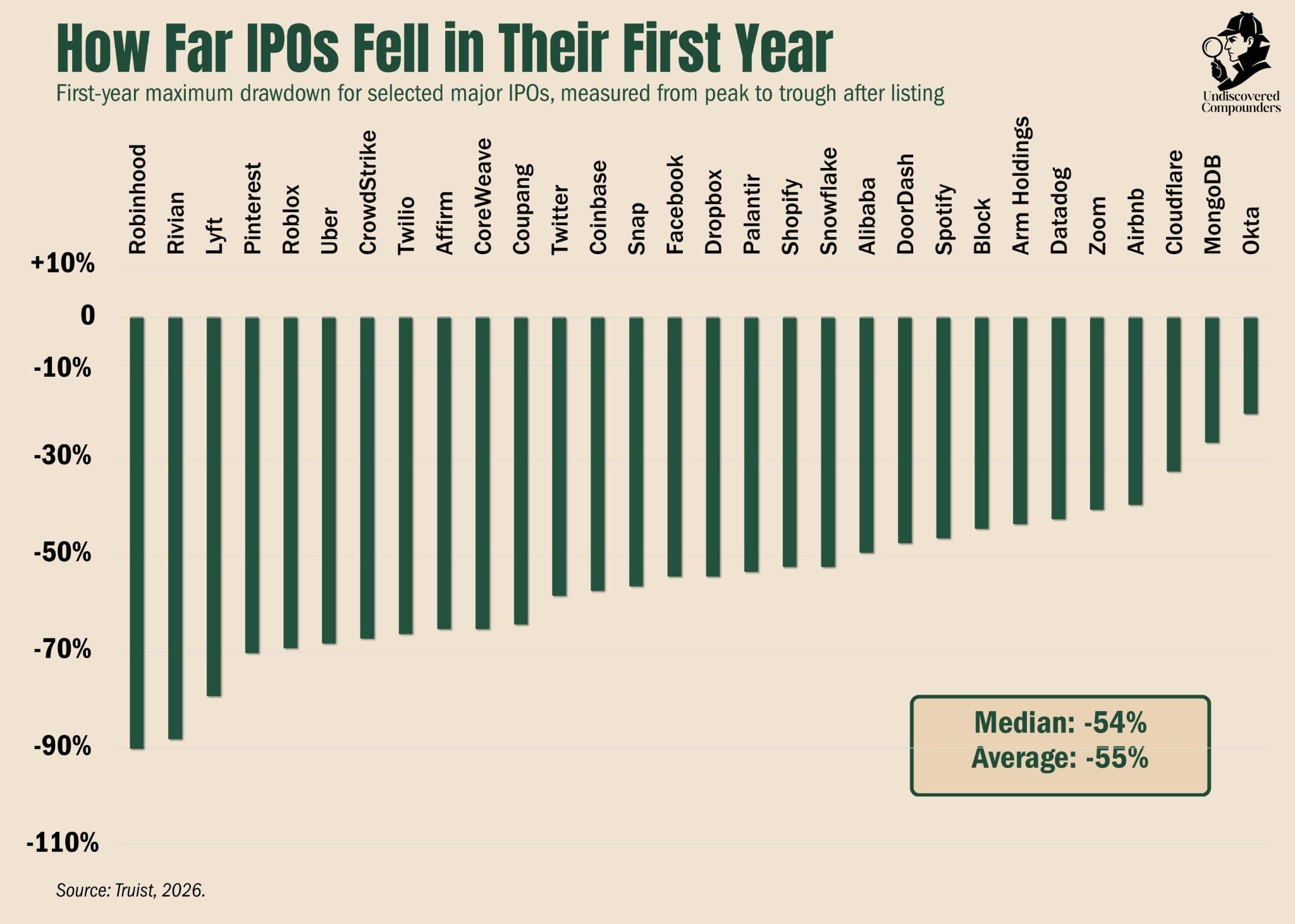

The last piece of the puzzle only comes into view when you look at the biggest IPOs of the last 15 years one by one.

In its first year, every one of these IPOs ran a max drawdown of dozens of percent. Every one.

Enough numbers. We have what we need to tell the story.

The Complete Statistical Story

Everyone but retail benefits from their respective asymmetries. Plenty of studies show how the IPO process and the incentives feed each other, making the game even more "biased," but each adds a layer of interpretation, and that's what kept them out of this post.14 Just in case: everything pointed to a structural, sustained disadvantage for retail.

That doesn't mean retail investors can't win. Short term, it's theoretically possible. You'd have to adjust raw data for fees, spreads, taxes, and above all for self-sabotaging psychology (still an objective fact, no?). But on paper, it's possible.

For long-term investing, the numbers leave no doubt: buying an IPO almost certainly means sitting through a drawdown in year one.

Yes, wonderful companies can go public. Yes, nearly every one of the world’s finest public companies went through an IPO. But there’s almost always a far better buying opportunity than the IPO itself. Usually within the first year.

If you're not chasing statistically rare short-term returns (days to a few weeks), there's no statistical reason to buy at IPO.

I don't think I can go further without interpretation.

“Those who do not know history are condemned to repeat it.” - George Santayana

Great opportunities exist outside IPOs too. Here's a great one.

Take care,

Flo

Refer friends and earn free months of paid access.

Zero downside (rare in this market).

Ritter, 2026, “Initial Public Offerings: Underwriting Statistics Through 2025,” University of Florida.

Pástor and Veronesi, 2005, “Rational IPO Waves,” Journal of Finance.

Field and Hanka, 2001, “The Expiration of IPO Share Lockups,” Journal of Finance.

Field and Hanka, 2001; Bradley, Jordan, Roten, and Yi, 2001, “Venture Capital and IPO Lockup Expiration,” Journal of Financial Research.

Brav and Gompers, 1997, “Myth or Reality? The Long-Run Underperformance of Initial Public Offerings,” Journal of Finance.

Basnet, Blomkvist, and Cumming, 2025, “Long-Run IPO Performance and the Role of Venture Capital,” British Accounting Review.

Cochrane, 2005, “The Risk and Return of Venture Capital,” Journal of Financial Economics.

The sample size is smaller here, 441 IPOs.

Boehmer, Boehmer, and Fishe, 2006, “Do Institutions Receive Favorable Allocations in IPOs with Better Long-Run Returns?” Journal of Financial and Quantitative Analysis.

The sample size is smaller here, 441 IPOs.

Boehmer, Boehmer, and Fishe, 2006, “Do Institutions Receive Favorable Allocations in IPOs with Better Long-Run Returns?” Journal of Financial and Quantitative Analysis.

The sample size is smaller here, 441 IPOs.

Boehmer, Boehmer, and Fishe, 2006, “Do Institutions Receive Favorable Allocations in IPOs with Better Long-Run Returns?” Journal of Financial and Quantitative Analysis.

Ritter, 2026, “Initial Public Offerings: Updated Long-Run Statistics,” University of Florida.

Rock, 1986, “Why New Issues Are Underpriced,” Journal of Financial Economics.

Author’s calculations using daily adjusted closing prices for the largest recent IPOs, measured from the first closing price and adjusted for splits and dividends.

Dorn, 2009, “Does Sentiment Drive the Retail Demand for IPOs?” Journal of Financial and Quantitative Analysis;

Derrien, 2005, “IPO Pricing in Hot Market Conditions,” Journal of Finance;

Ljungqvist, Nanda, and Singh, 2006, “Hot Markets, Investor Sentiment, and IPO Pricing,” Journal of Business.

The median return of -25.7% versus +39.6% for

the market is the number that should end most

IPO conversations before they start.

2 things I would add mate is :

1. u missed FIGMA stock from 150-15 in under 8 months.

2. you can short these IPO stained stocks by gettings leaps on them for cheap when they are high and use as a hedge.