30% of my portfolio is in this company: revenue and EPS up 3x in 3 years, trading at 12x EBITDA, 50% below peers.

The downside is bounded, the upside is not. That is why I sized it big.

This is my highest-conviction idea at 30%, my largest position at the time of writting. . I put another 10% of my portfolio into it a few days ago.

So I'm putting 15,000 words behind that conviction. All of it: arguments, numbers and assumptions. Nothing held back.

May you have as much fun reading it as I had writing it.

Take a highly regulated, highly fragmented industry, so interdependent that one large player relies on dozens of others, each of which relies on dozens more.

Add critical, certified products, installed for years across hundreds of platforms, with a customer base that would be an understatement to call “conservative.”

Let that run for a few decades and you end up with large industrial groups carrying hundreds of product lines. Somewhere in that pile of parts, some become too small to remain part of their “internal priorities.” But they cannot disappear. Hundreds of machines depend on them.

When capitalism does its job well, the smaller company steps in to arbitrage the constraint. That’s the better owner principle.

It buys mature product lines the larger players want to shed, takes over the rights and the customers, then runs them through an optimized cost structure.

Call it industrial recycling, with better margins. Many companies have created a lot of value this way. TransDigm did it in proprietary aerospace components. HEICO did it in replacement parts and approved repair.

Today’s company has turned this mechanism into a business model, one its legacy business sharpens: each side feeds the other.

Revenue up nearly 80% in a year. Margins expanded. Management still guides the company to nearly triple revenue again by 2029, while keeping the kind of margins most industrial businesses would politely call unreasonable.

And yet the stock is down by half because Mr. Market had one of his recurring mood disorders. A quarter came in with little growth, a pause management had been flagging for quarters. But the market decided that a timing issue was a thesis problem. Helpful, as always.

He did the same thing a year ago. It worked out nicely for whoever was buying.

Here's Innovative Aerosystems (ISSC).

Table of Contents

1. Short-form Thesis

2. The Business Model

Where It Sits in the Industry

The Proprietary Cockpit Stack

ThrustSense Autothrottle

The Future

The Acquisition Engine: Industrial Recycling

The Seller

The Product

The Buyer

The Precedents

The Synergies Between the Two Models

Cross-Selling

Portfolio Completion

More Cash Flow to Finance R&D

3. Acquisitions

Wave 1, First Steps

Wave 2, Great Leap Forward

Wave 3, Preparing the Future

The Patterns

4. The Operational Trajectory

The Origin of Growth

Margins

The May 14, 2026 Sell-Off and Mr. Market’s Mistake

The Math Behind IA Next 2029

5. The Capital Structure

6. Governance and Alignment

The Engineer Who Allocates

Alignment

The Board and the Shareholder Base

The Real “Governance” Risk

7. Valuation

Qualitative Valuation

The Discount

The Risks

Discount vs Risks

The Assumptions

Ground Rules

The Scenarios

The Inputs

Verdict

8. Conclusion

1. Short-form Thesis

Company: Innovative Aerosystems (formerly Innovative Solutions & Support).

Ticker: NASDAQ:ISSC

5-word business model: ISSC makes aircraft cockpit parts.

Price: $17.

Market Cap: $300M.

EV/EBITDA: 12.3x.

Distance From ATH: -45%.

The setup is fairly simple.

After the May 14 sell-off, the market values ISSC at around $300M.

Management is targeting $250M in annual revenue by 2029, at a 25-30% Adj EBITDA margin, which works out to $63-$75M of Adj EBITDA versus $25M in FY2025.

At the current 12.3x EV/EBITDA multiple, that gives a 2029 EV between $775M and $920M.

Net of debt, the equity is then worth around 2.5x. No re-rating needed, despite trading 50%+ below peers. No significant change in the business. Just the same old business.

Proportionally, the downside is sharply limited. Even if the company misses guidance. Even if the company is "frozen."

Still, whether the guidance is credible is the question that matters. The past says yes.

The acquisition strategy already has a three-year track record:

In 2025, ISSC almost doubled the footprint of its Exton facility, from 45k to 85k sqft, and more than tripled production capacity, for a total cost of (only) $6M.

Since June 2023, six asset purchase agreements have been signed, three of them in the February-March 2026 window alone, totaling $87.7M in cash deployed. Most of its growth comes from acquiring product lines that the giants no longer want.

Revenue also almost doubled between FY2024 and FY2025 (tripled since FY2022), and net margin moved from 14.8% to 18.7% over the same period (20.6% to 24% on operating margin).

The pipeline is set to widen further. Honeywell will spin off its Aerospace segment as HONA in 2026. That’s a $17.4B revenue business about to become a standalone pure-play, with the portfolio discipline that comes with it, and therefore more legacy lines to divest to credible, established buyers. ISSC has already proven that credential to Honeywell, more than once. Either way, Honeywell is only one seller out of five or six. Collins, GE Aerospace, Garmin, Moog, and Elbit each have their own legacy lines to rationalize.

The remaining job is “simply” to keep going. Acquire and integrate another $130-$140M of revenue by 2029.

If everything looks so rosy, why the Q2 FY2026 sell-off?

First, the price was already stretched after a 3.8x in four months. Fair to say the market had gotten well ahead of itself, and the smallest hiccup was going to cool it down. Despite my own conviction, I had trimmed 25% of my position at that point.

Second, management had been guiding to a weaker Q2 FY2026 for several quarters, flagging an F-16 trough between two production cycles tied to the line transition from Honeywell to ISSC. Q2 FY2026 came in at $22.4M of revenue, +2.0% YoY, and the market treated it more or less like a broken thesis.

Nothing new. The stock fell from $20 to $8 between August and November 2025 for the same reasons: a revenue air pocket tied to a line transition. The stock then ran almost 4x over the next four months.

The May sell-off changes nothing about the thesis. It's just Mr. Market being Mr. Market. At least it handed me a discount I was glad to take.

All that’s left is to show this reading holds up to the facts and the math.

One click away from not missing the next undiscovered compounder.

2. The Business Model

Even knowing the company very well, I have to say that the description of its business model in the 10-K is fairly vague, to put it politely. The investor presentation is a much better starting point:

At the center: the physical structure of the cockpit. Around it: all the electronic systems bolted on top to make the cockpit work. ISSC designs these systems, manufactures them, installs them, and supports them across their full lifecycle. That is complete vertical integration, all under one roof in Exton, Pennsylvania.

In a field where every component requires FAA (Federal Aviation Administration) certification and where the slightest modification triggers a long and often painful recertification cycle, that vertical integration is clearly a competitive advantage.

It obviously didn’t come from nowhere.

This moat was built over 37 years of work and relationships, which today allows ISSC to equip aircraft under OEM contracts with the sector’s biggest players. The legacy business has been generating cash for decades (with ups and downs) and accounted for all of the P&L through FY2022. The sector itself acts as a barrier to entry. An operator does not have the luxury of choosing its supplier. It buys what is approved for its aircraft. That’s the rule. And often only one company has gone through the long certification process for its product on that specific aircraft. When Lockheed Martin builds or upgrades an F-16, it has to buy the display generator and flight control computer produced by ISSC. No one else has the right to manufacture them (under Honeywell licensing since September 2024), and no one else wants to do it at that scale.

The second component is what kept that business model alive for 37 years: innovation. The ThrustSense® Autothrottle, the first FAA-certified turboprop autothrottle (which literally saves lives), has been generating cash flow since at least 2019 and will continue to do so for years, if not decades. The current pipeline is a loaded one, with UMS2 and Liberty Flight Deck at the front, and will not contribute meaningfully to revenue before 2027-2028, subject to a regulatory schedule that is notoriously hard to pin down. Behind these innovations, ISSC has a clear vision: autonomous flight. But one thing at a time.

ISSC keeps the cockpits of yesterday in service and is figuring out what the cockpits of tomorrow look like.

That leaves the third engine: acquisitions. That engine kills three birds with one stone:

It adds certified installed base to the mature stack.

It gives ISSC the technical building blocks it was missing in the forward-looking pipeline (things that would have taken years to develop internally).

And it comes with a customer base ready to cross-sell into.

I'll break them down one by one. But first, let's put ISSC back in context.

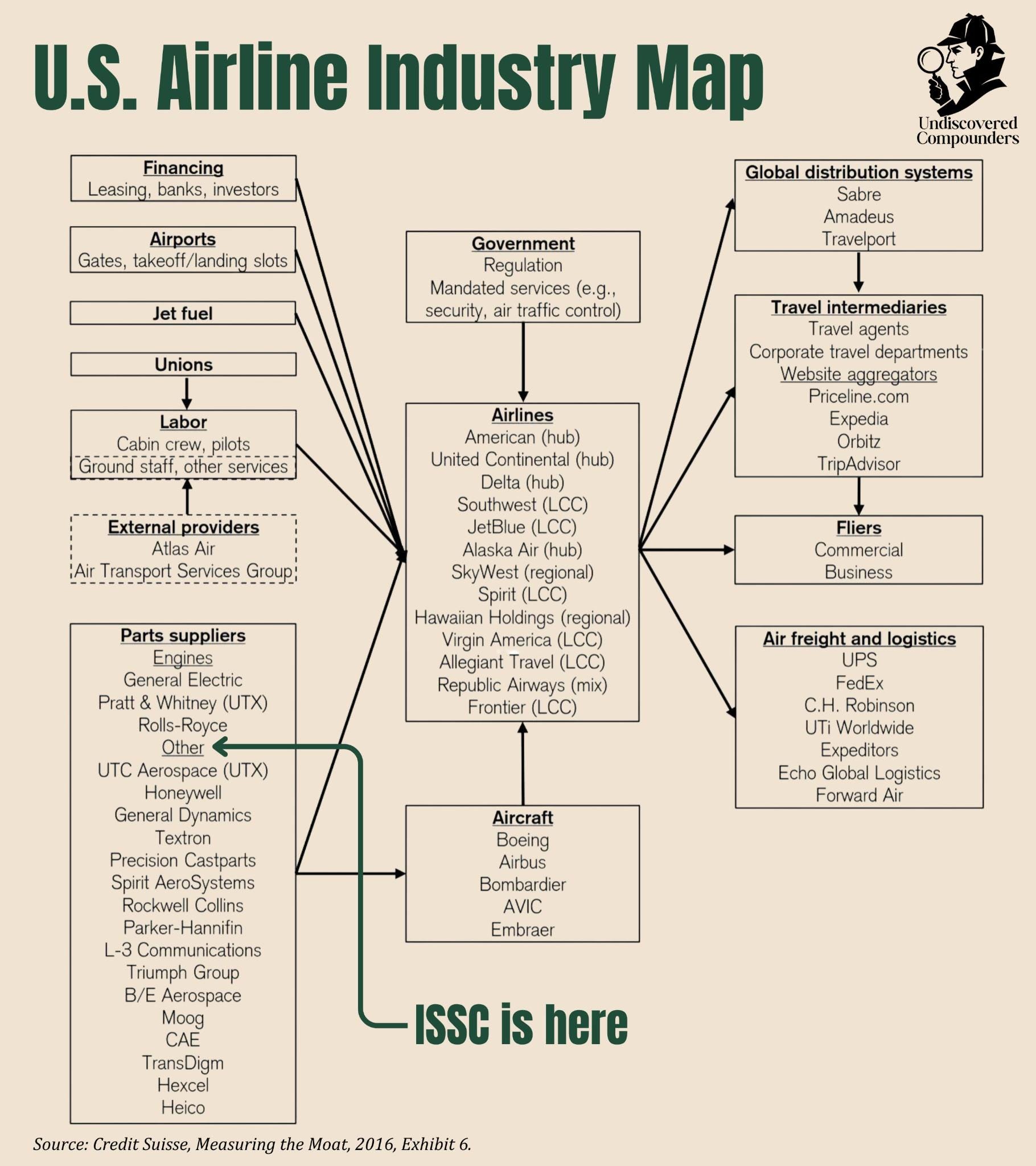

2.1 Where It Sits in the Industry

I would have liked to write a full section on the industry and where ISSC fits into it. I’m going to skip it. Three reasons:

We have little visibility into ISSC’s specifics: what it sells, at what price, and to whom. “Professional secrecy.”

The industry is genuinely complex, with a lot of players and a lot of moving parts.

And it’s honestly not relevant to the thesis.

For your viewing pleasure, here’s a snapshot of the sector anyway. Don’t bother thanking me.

But we still need a general overview.

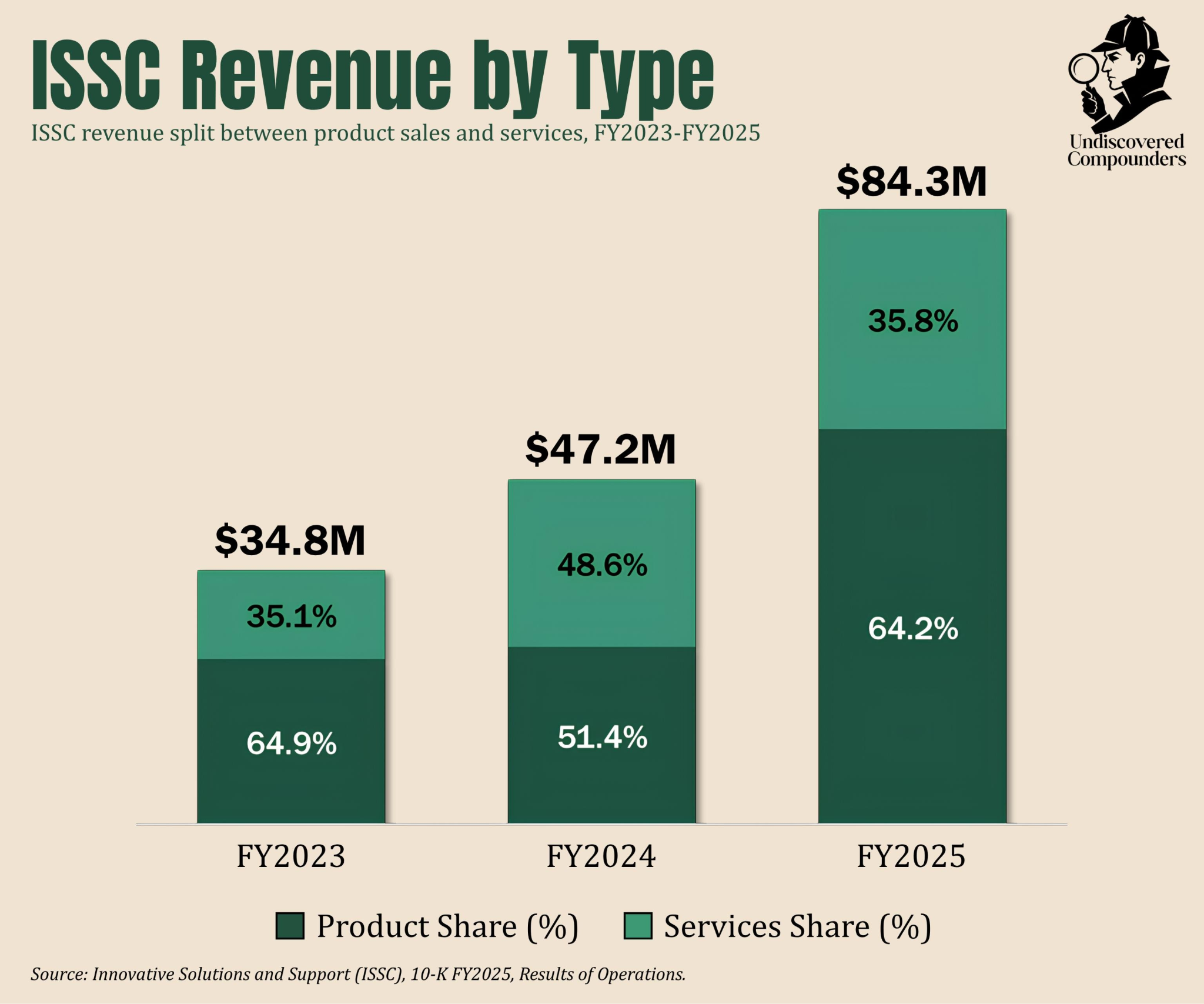

ISSC sells products that run from a replacement seal worth a few dozen dollars to the ThrustSense autothrottle, somewhere between $70k and $100k per aircraft by my estimate. And services too: from overhauling a cockpit component for a few thousand dollars to an Engineering Development Contract (EDC) that can run into the millions.

The product/service split is the only breakdown management fully discloses. That answers the what. Not the who, and not the how.

Start with the how. There’s OEM (the new stuff, gear fitted to an aircraft still in production) and there’s the aftermarket, which is everything else. Roughly, aftermarket = MRO + retrofit.

Maintenance, Repair & Overhaul (MRO) is everything that keeps already-installed equipment running. It’s recurring revenue, and it isn’t optional: an aircraft has to go through inspections at intervals the regulator sets, or it stays on the ground. No recession in this corner of the market. Just the same old business.

Retrofit means fitting new or upgraded equipment onto an aircraft already in service. Higher margin, and strongly countercyclical: when there’s no budget for a new aircraft, you modernize the old one.

Here’s the part management doesn’t push hard enough, in my opinion. On most of the products ISSC builds (or whose production lines and patents it buys), it is the only provider cleared to service them and supply parts.1 No competitor is allowed to touch a box that ISSC alone is certified to maintain.

If the aftermarket is so attractive, why bother with OEM at all? Why supply low-margin gear to Pilatus, Boeing, Textron? Because today’s OEM is tomorrow’s aftermarket. Every unit fitted on the production line creates an installed base that throws off MRO and parts revenue for decades.

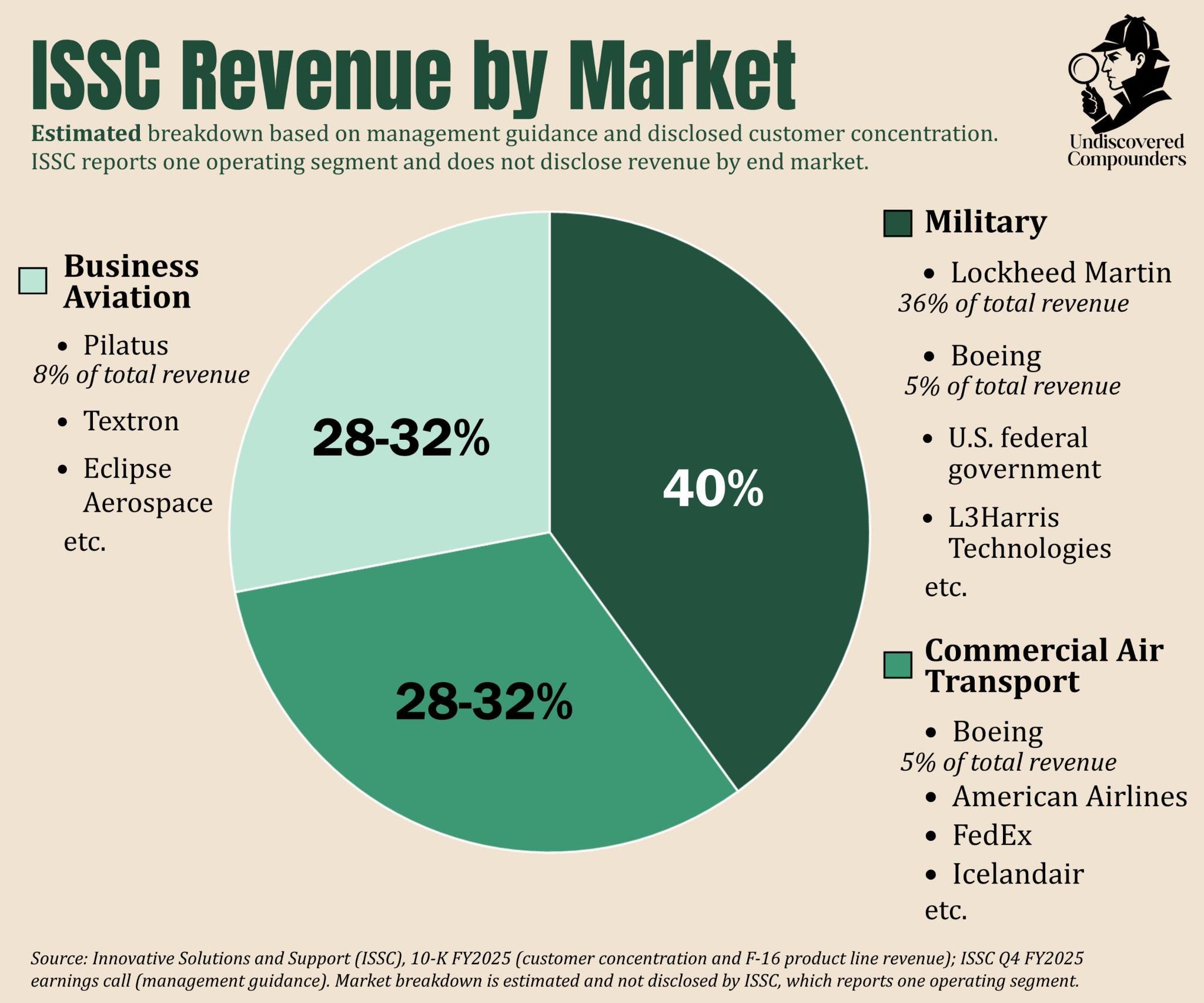

Management gives no number, but my guess is revenue runs around 80% aftermarket (20% OEM), a good chunk of it MRO. My main argument is the way ISSC’s customer base has shifted, and its tilt toward the military, which carries relatively little OEM.

The military, precisely, that’s one answer to the who. But who are the others? The question matters, because the who drives a lot: type of contract, margin profile, and the rest.

No disclosure here either, just my estimates. They can swing hard from one quarter to the next, even one year to the next. The constant is the weight of the military, which four years ago didn’t account for more than 10%.

Here's what matters about each.

Military: combat and transport/refueling aircraft flown by armed forces, not necessarily American ones. Usually long-dated contracts with low gross margins, offset by near-zero SG&A. No advertising to pay for, the contract funds the engineering, the customer comes back.

Commercial air transport: think airlines and cargo. Big customers with big fleets, on frequent and heavily regulated maintenance cycles.

Business aviation: aircraft or small fleets owned by individuals and companies. Everything is smaller (the aircraft, the customer, etc.), and the market is far more fragmented.

ISSC supplies OEM parts to all three markets. Which means it supplies their MRO and retrofit too.

The big picture is clear enough. Time to get into the details.

Make the time spent on these visuals worthwhile. Share this article with your friends and colleagues. Let's make Undiscovered Compounders a little bit more undiscovered.

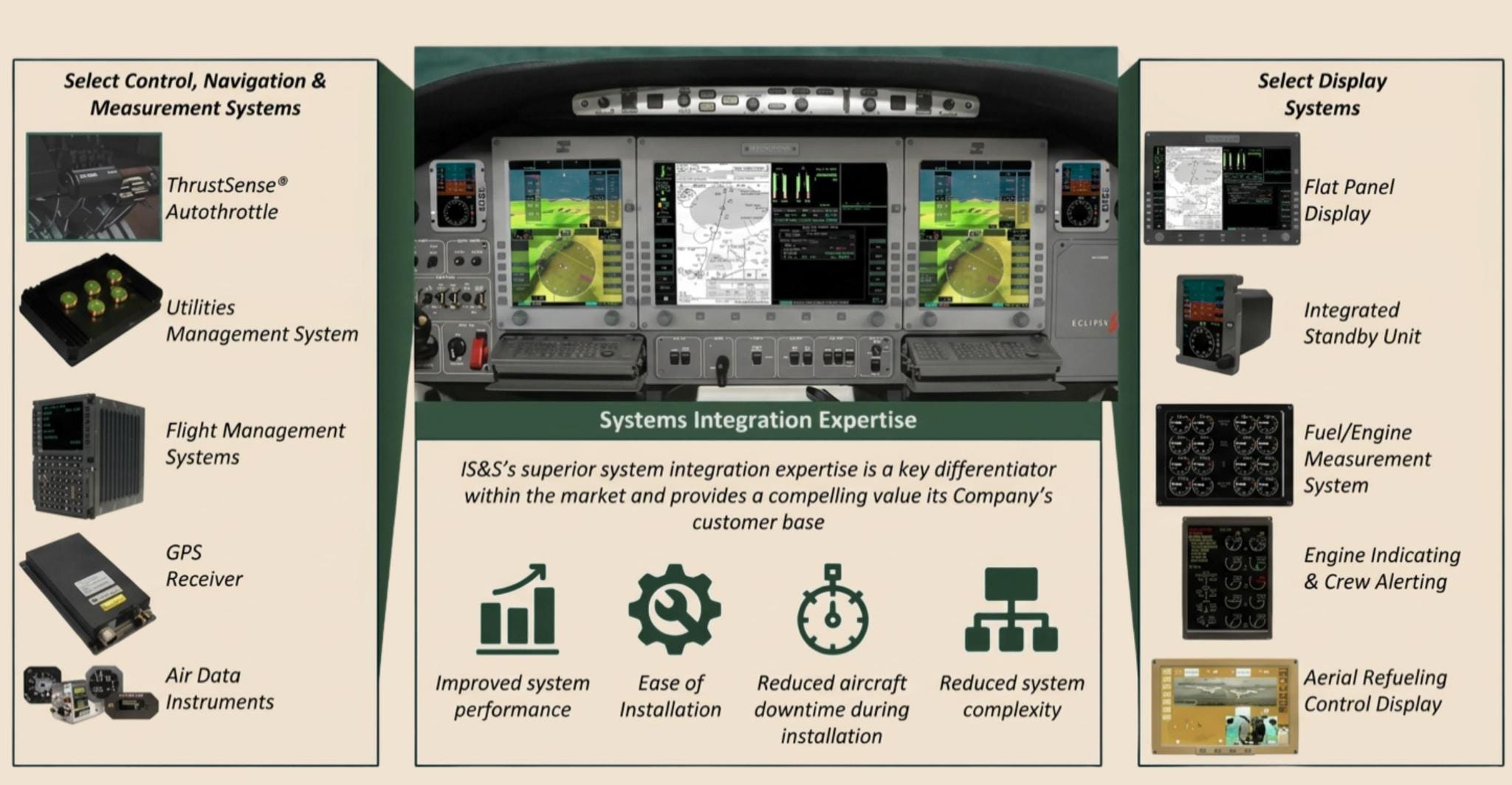

2.2 The Proprietary Cockpit Stack

Historically, ISSC’s proprietary business is made up of 6 certified product categories, all manufactured in the one and only factory in Exton, Pennsylvania:

Sensors, to collect information (altitude, speed, etc.);

Displays, to show it;

Communication, to communicate;

Navigation, to navigate;

Actuators, to activate the physical flight controls;

Control Systems, to run it all.

The details matter little. The central idea is that its products cover most of the building blocks of a modern cockpit in the segments where ISSC currently operates, with one exception. An in-house autopilot is missing. Or rather, was. We will come back to that.

Among them, one product is nonetheless worth detailing, because it demonstrates what ISSC intends to replicate in the coming years.

2.2.1 ThrustSense Autothrottle

In 2016, ISSC identified a need the market had not met: no autothrottle for turboprop aircraft.

Very roughly:

Turboprop = propeller + turbine, slow, short-haul, economical.

Jet engine = pure jet, fast, long-haul, more expensive to operate.

The autothrottle is what allows engine power to be managed automatically throughout the flight, without the pilot having to touch the throttles manually (takeoff and landing included). That lifts an enormous cognitive load off pilots, and takes away one more chance of a serious, even tragic, mistake.

Every modern commercial jet has one, but not turboprops. Such is capitalism: no manufacturer had ever deemed the market attractive enough to invest in.

ISSC sees the need and, confident in its engineers and its company culture, invests. Three years later, in April 2019, the FAA certified its ThrustSense Autothrottle for retrofit on the King Air.2

It thus became the first autothrottle in the world certified for a PT6 engine (Pratt & Whitney), meaning the engine that powers the vast majority of civil turboprops. In practice, being certified for PT6 means covering most of the global turboprop market. That’s all. To this day, ThrustSense is the only FAA-certified autothrottle for PT6.

After that, foreign certifications follow quickly, and Textron, one of the major players in the sector, signs a multi-year OEM contract to integrate ThrustSense into the newly manufactured King Air 260 and 360. ThrustSense is therefore integrated into older turboprops and new ones alike.

The military spots the opportunity and selects ThrustSense in late 2024 for its militarized version of a civil turboprop.

In reality, the military had no choice. There is currently no other autothrottle for PT6 turboprops. Developing one would take years and a string of certifications.

Here, it is clearly worth acknowledging the prowess of the current CEO, Shahram Askarpour (Vice-President of Engineering until 2012, then President until 2022). He is the one who spotted the need, who had the technical vision and the engineering skills to create this product.

And his transition as CEO has not stopped the company from preparing for the future.

2.2.2 The Future

Two significant products are in the pipeline.

Utility Management System 2 (UMS2), the next generation of the UMS delivered on Pilatus aircraft. Think of the UMS as the brain of the cockpit, monitoring and controlling most of its other components. The main addition in this new version is the integration of a neural network that brings AI to increase the level of cockpit automation. The first UMS2 deliveries to Pilatus for their PC-24 model are expected in the coming weeks. Seen that way, it looks like nothing more than a product upgrade that will at best generate a bit more revenue. But the UMS2 is platform-agnostic. It can also serve business aviation and the military, subject to regulatory approvals that will take time. AI, and a new pool of potential customers. And that is not the biggest innovation.

Liberty Flight Deck (LFD). The “Deck” here is the most important part. Before the LFD, ISSC sold cockpit components here and there, one autothrottle for X, one UMS for Y, and so on. The LFD is literally a complete, turnkey cockpit, with all systems talking to each other natively. And here, ISSC takes a different route. Other competitors already sell complete flight decks (Garmin, Honeywell, Collins), but most remain largely proprietary. You buy the whole ecosystem, or nothing. LFD is fully open-architecture. You can connect competitors’ products to it, you can upgrade it modularly. That is a massive commercial argument, especially when clients (airlines and operators) complain at every opportunity about lock-in by the major integrators.

“The Company believes that its new Liberty Flight Deck (LFD) will be a key driver of its next phase of growth.” 10-K FY2025

First commercialization targeted for 2027 in the business jet aftermarket, and 2030-31 for OEM platforms.

The last comparable phase of innovation dates precisely from the early 2000s. So, why a turnaround 20 years later?

This is going to sound a bit harsh, but I think the main cause is the death of founding CEO Geoffrey Hedrick in early 2022. He had a vision when he created his company, a vision suited to his time, and it worked. He was also an engineering genius, with over 100 patents to his name. But the market evolved, and he failed to adapt. The company struggled from 2006 until his death. His capital allocation was equally questionable, far too conservative for this sector. On several occasions, reading through old analyst commentary, I came across recommendations urging strategic shifts that he dismissed out of conviction.

The arrival of the former VP Engineering, an engineering genius (yes, him too), Shahram Askarpour, as CEO was the triggering event. He sought to reorient the product mix and target military clients, put a strong focus on innovation, and used his network and reputation to make acquisitions. And it shows perfectly in the non-financial data. Engineering headcount has grown by more than 50% in each of the last two fiscal years. The number of patents has more than tripled in 3 years (international & trademarks included). Management and the core engineering team average more than ten years of tenure at the company.

The 30x from the Covid trough to the 2026 high is not a consequence of a 37-year-old business model. It is the reward, earned year after year, of an exceptional management team and its employees who transformed this company from a barely surviving business into a recognized player.

Shahram Askarpour has transformed the company in a few years, and I am convinced he is the primary architect of its success.

That is why the avionics giants chose them when it came to selling their orphan product lines. They needed a credible buyer, and ISSC had become one.

2.3 The Acquisition Engine: Industrial Recycling

Acquiring orphan product lines from sellers for whom the sale is immaterial, and who want quality buyers to avoid alienating their customers.

2.3.1 The Seller

Of 6 acquisitions, Honeywell Aerospace is the source of 5 of them. Honeywell Aerospace is a $17.4B revenue business in 2025, currently being spun off under the ticker HONA, expected by Q3-2026.

For HONA, a product line generating $5M or $10M per year, even a profitable one, is a rounding error. But a rounding error that ties up resources (engineers, certifications, factory space, etc.). For an efficient capital allocator, the equation is relatively simple: these product lines are generally worth more sold than kept.

But that was the old reality for Honeywell. Honeywell Aerospace is being spun off in the coming months. To understand the impact this will have on ISSC, it is better to treat this spin-off as a source of answers rather than questions:

“Honeywell has been over the past couple of years divesting a number of their avionics product lines. The exact nature of their purpose they will not share with us, other than these are the kind of the previous generation of the product lines and now they’re moving on with their latest and greatest.” Conf Call June 2023, CEO.

3 years later, we have the answer. All those divestitures were preparation for this spin-off. And the Form 10 adds even more clarity: HONA intends to focus on its recent innovations. I use the term “innovation” again, but we are objectively talking about a different level of technology than ISSC’s (to be fair, ISSC is a dwarf compared to HONA): a touchscreen cockpit with native cloud, software to navigate in GPS-degraded environments, and even electric propulsion systems. The future, basically.

On the other hand, an autopilot designed 20 years ago installed on tens of thousands of civil aircraft (KFC 325) is not the future, nor Honeywell’s priority. Same goes for military display generators on aging F-16s (still in production 50 years later), or electrical generators on even older F-15s. That is precisely why it has been selling them to ISSC since June 2023.

Once listed, the incentives will be even stronger. HONA will be scrutinized quarter by quarter on its margins and strategic focus, and anything that is not the “future” stands a good chance of becoming sellable.

Obviously the pattern is not specific to Honeywell. It is in fact a classic cycle among the aviation giants: they acquired a line 15 years ago, integrated it efficiently, then moved on to the next generation, which eventually made it irrelevant. It may be awkward to have in the portfolio, but the line exists physically, and the aircraft that carry it and need maintenance or even part replacements also exist, and often for decades. They certainly want to get rid of it, but they do not want to sell it to a company that will manage the line poorly and anger their clients (those clients very often remain clients on other products, it is a very closed ecosystem), and they choose, in their view, the best buyer to protect their reputation.

When Moog sells its S-TEC line (autopilot product line, well played if you have been following) in February 2026, it does not explain why in detail, but this is precisely the mechanism I just described.

2.3.2 The Product

First important point: ISSC only acquires product lines certified by the FAA (USA) or EASA (European Union), or both. Without that, the aircraft has no right to fly.

Second important point: these certifications do not transfer automatically. When Honeywell sells a product line to ISSC, ISSC must obtain its own TSO authorizations (Technical Standard Orders, the FAA’s minimum performance authorizations required to manufacture and sell specific avionics equipment) for each product (still simpler than a full certification from scratch since the design data already exists). Askarpour estimates this at around one year per transaction to migrate all TSOs. Obviously, no newcomer can enter a product market without having paid this entry cost (both time and money), for a market that often represents only a few thousand units per year at the end of the chain.

And these aircraft fly for a long time. A very long time. ISSC’s 10-K states it clearly: its products equip aircraft “in service for up to fifty years.” A King Air rolling off Textron’s production lines in 2026 will need ISSC-certified parts in the 2050s. And for the lines Honeywell manufactures today and will sell off in 15 or 20 years, there will be several more decades of demand after their sale. Concretely, ISSC’s future acquisition pipeline is already on Honeywell’s assembly lines.

To top it all off, the installed base is aging. The average age of the global commercial fleet reached 14.8 years at the end of 2024 (a record), and the curve has been rising for 20 years. Blame the airlines that do not have the balance sheets to renew at the historical rate (or rather a supply chain that extracts maximum value upstream and a hyper-competitive sector). So you keep the aircraft, you replace the parts, and that is exactly where ISSC fits.

2.3.3 The Buyer

On the first deal in June 2023, Honeywell received 7 bidders. Of those 7, ISSC was the one chosen, as it was for the four following acquisitions. ISSC's CEO puts the choice down to one thing: “We had unique capability at IS&S that made us a very attractive buyer.” Fine, but which ones?

First, ISSC manufactures 100% of its products in its Exton factory in Pennsylvania. A major difference, given that nearly the entire sector outsources a significant portion of its subassemblies. Less subcontracting = better margin on products, which is good news for ISSC, and for Honeywell. Obviously, ISSC gets new product lines that bring in a material amount of cash flow, and Honeywell gets rid of lines that are too old (whose customers sometimes complain that they had been neglected by Honeywell, with delays, lower quality, etc.) and finds a player for whom those lines matter and who has every incentive to manage them effectively. It is even one of the main levers that drove ISSC’s Adj EBITDA from $11M in FY2023 to $25M in FY2025.

“Typically Honeywell has outsourced a lot of these manufacturing of their subassembly. And there are opportunities there for us to take a look at some of the outsourcing they do because we have full in-house capability.” Conf Call, June 2023, CEO.

Second, ISSC has room. A lot of room. ISSC prepared the reorientation of its business model toward M&A and optimized the setup of its current factory, doubling the floor space and tripling production capacity in anticipation of this M&A. Honeywell therefore finds itself facing a player that has already prepared the ground and is ready to integrate these lines quickly and efficiently.

Third, they showed they were capable. Once the first transition was completed, then the second, ISSC built a reputation as an efficient acquirer and integrator. Once again, the aerospace world is a fairly closed one, everything gets around quickly, and ISSC’s reputation also reaches the 5-6 other giants ready to get rid of their lines. Moog’s divestiture of its autopilots to ISSC in 2026 is in part a reward for ISSC’s previous successes.

ISSC deserves credit for its execution, but it did not invent the business model.

2.3.4 The Precedents

To understand ISSC’s future potential, you have to look at those who came before.

TransDigm ($80B) and HEICO ($40B) spent decades doing something similar to what ISSC does.3

TransDigm acquires companies that own proprietary and sole-sourced aircraft components while HEICO is best known for creating alternative parts that compete with the OEM. Both exploit a similar asymmetry to ISSC: products that don’t die, margins majors tend to leave on the table, customers who pay for reliability, all in a niche, heavily regulated sector with recurring revenue.

Can ISSC become the “next” TransDigm or HEICO? The current math allows it. My read: very unlikely. Three questions crystallize the uncertainty:

Does the company have the human capabilities to execute this transformation?

Will ISSC be able to make enough acquisitions for that?

Will the acquisitions be sufficient?

The first is too uncertain to attempt an answer. The only thing to say is that so far, management has executed the transformation very well over the last 3 years. But there is a real key personnel risk with CEO Shahram Askarpour, who is 68 years old. HEICO has had and will have multiple generations of Mendelson. More on that later.

For the second question, one argument is worth (re)mentioning. The global fleet is aging, increasing the need for MRO and retrofit of older aircraft, exactly the kind of lines ISSC targets through these acquisitions. So demand for these products has a future. On the supply side, today’s new aircraft will become tomorrow’s old ones, and therefore a new pool of lines for ISSC. Relevant, yes. Sufficient to cross tens of billions in market cap, hard to tell. No doubt it will be more complex than acquiring private companies outright, like TransDigm does.

On the other hand, ISSC has something HEICO and TransDigm don’t have at the same level: a clean-sheet R&D engine on top of its M&A pipeline. Its own proprietary R&D has historically been a source of revenue and cash flow, and the company continues to fill its innovation pipeline for the years ahead with UMS2 and the Liberty Flight Deck.

The third question is the most important but also the most complex. Clearly, ISSC doesn't have TransDigm's pricing power and probably never will. The TransDigm level is, in my view, out of reach for ISSC. On HEICO, I'm less categorical. Obviously, the comparison isn't perfect, particularly on the Parts Manufacturer Approval segment, where ISSC has no presence. But ISSC's model has its own advantages, notably enormous cross-selling opportunities. The “yes” isn't obvious, but neither is the “no”.

All of this remains speculation over several decades, and obviously won’t constitute a bull case, but the pattern was worth mentioning.

2.4 The Synergies Between the Two Models

This is what makes the ISSC opportunity so attractive and, in my view, completely underestimated by the market.

3 major synergies stand out.

2.4.1 Cross-Selling

By acquiring these product lines, ISSC enters into commercial relationships with new clients and can also offer them its other products. In a sector this conservative, it’s a way to expand its customer base without having to spend millions on marketing and customer relations, and above all, a lot of time.

This applies to existing products:

“We benefit from deep customer relationships which have further strengthened following the Honeywell transactions. This gives us the opportunity to cross-sell our broad portfolio of existing products to customers. As an example, some of the radio products recently acquired from Honeywell were coupled nicely with our cockpit offerings in the C-130 platform.” Conf Call Q1-2026, CEO.

But also for future products. When Liberty Flight Deck is certified for the business jet aftermarket, the customer base will already exist and be well established. Same for UMS2, which is platform-agnostic. ISSC innovates where demand meets expertise. My guess is that cross-selling drives more of those R&D decisions than the filings suggest.

2.4.2 Portfolio Completion

Earlier, I told you that ISSC had every product needed to offer an integrated cockpit suite except one: a certified autopilot.

The gap is enormous. The FMS calculates the route, the FPDS displays it, the UMS controls all the subsystems... but no autopilot to fly the aircraft. Not for Part 23, and even less so for Part 25:

Part 23 is the standard for light aviation (turboprops, light jets, etc.). These aircraft carry fewer passengers (≤19) and are less regulated.

Part 25 covers large business jets and large commercial transports (A380, Boeing 737, etc.). Extremely regulated, but significantly larger in value than Part 23.

To create a certified Part 25 autopilot from scratch, you are looking at 5 to 7 years from design to first sale, and tens of millions of dollars out of ISSC’s pocket. Or rather, used to be.

In February and March 2026, ISSC acquired two complementary autopilot product lines for approximately $25M cash combined. Together they cover the spectrum from small General Aviation (all civil aviation except airlines) aircraft up to certain Part 25 applications. Among others, they acquired the lines for:

The KFC 230, a next-generation digital autopilot developed by Honeywell only 4 years ago. It becomes “the workhorse for our own autopilot.”

The KFC 325, whose autopilot is installed on tens of thousands of aircraft. Aircraft to which ISSC will now be able to sell its UMS2 and Liberty Flight Deck once certified. And above all, an enormous client base for future MRO and upgrades.

For $25M, ISSC bought future clients and everything needed to offer a full cockpit suite to those same customers. According to its CEO, with these acquisitions it have become “probably the largest autopilot supplier right now in the market covering the spectrum of aircraft”.

2.4.3 More Cash Flow to Finance R&D

You make avionics components, you watch the market and its inefficiencies, and you find ideas that could address them and that require R&D. You go to a bank to borrow a few million and explain that you want to borrow to fund R&D that may or may not turn into future cash flow, and if it does, only in a few years (regulation doesn’t rush). Best case, you get a polite “no.”

You want to buy product lines that the giants want to get rid of, often at low prices. You have the expertise and infrastructure to do it. You go to a bank, explain the situation, the quick cash flows, and it lends you $20M over 5 years. Perfect. You buy the line. You integrate it quickly, generate your quick cash flows, to the point where you pay back the debt in a few quarters. You repeat this across several deals, and each time, you allocate part of the cash flows to R&D. In the end, you’ve managed to double your R&D budget in 3 years, and the cherry on top is bigger than the cake: you have more revenue and cash flow even without the R&D needing to pay off.

You are now able to innovate significantly more and create a new generation of products.

The first scenario is obviously fictional, and ISSC did not make these acquisitions in order to fund R&D more freely, but it shows how the acquisitions enhance innovation and therefore ISSC’s historical business.

To temper expectations, this synergy is probably limited at this stage. UMS2 started being funded before the acquisitions. Liberty Flight Deck is probably the only product directly benefiting from this R&D facilitation. What is certain, however, is that ISSC now holds all the cards to focus on R&D when it finds an opportunity worth the time and money.

Now that we have a clear picture of the business model, we can look at the acquisitions.

3. Acquisitions

6 deals in 3 years for a total of $87.7M cash. 5 were done with Honeywell and 1 with Moog.

Analyzing them one by one would be the best way to miss the strategy behind these acquisitions, but a short summary of each doesn’t hurt.

These 6 acquisitions can be split into 3 waves.

3.1 Wave 1, First Steps

Some context. In June 2023, ISSC sat at $34M of revenue, $11M of EBITDA, and a market cap of around $100M. The deal itself was $35.9M. A good third of its market cap. For a microcap that had been going nowhere since 2006, this was objectively a big bet. The risk was partly cushioned by the financing: $20M in term loan and the rest from its own cash.

With that, ISSC bought lines of inertial reference units (IRU, used to calculate trajectory data without GPS) and communications/navigation radios installed on thousands of aircraft (mostly Part 25). Why these lines in particular? For 3 reasons.

First, the basic financial logic is attractive: ISSC had about 50% of its production capacity sitting unused at the time, and these new products require the same infrastructure and the same engineers as the existing ones. So integration costs are low and integration is fast. On top of that, post-integration margins on these lines are similar to ISSC’s margins at the time. The lines can generate meaningful cash, and quickly.

Second, the logic is also strategic: portfolio completion & cross-selling. At the time, ISSC had a “limited capability” in inertial and comm/nav. This acquisition allowed it to complete and optimize the portfolio quickly. And these lines serve thousands of aircraft, which gave ISSC a network of customers it could never have built organically.

One last detail makes these lines particularly attractive for ISSC. An IRU or a comm/nav radio installed on a Boeing 737 never stays in service for 25 years without intervention. They need MRO. If Honeywell wasn’t interested in these lines anymore, it was even less interested in the MRO around them. Honeywell had stopped servicing this market for these lines years ago. An operator had to look for providers certified and authorized by Honeywell for MRO on these lines, and according to customer feedback, the offering was clearly insufficient.

For ISSC and its $100M market cap at the time, this was a windfall. So ISSC bought the exclusive IP rights and is more than happy to service the MRO on these lines. Every time an aircraft needs MRO, ISSC is the only authorized supplier. A perfect example of the better owner principle in M&A.

Theory is clean. Practice too.

A word on Adjusted EBITDA, because I can sense it irritates someone. I'm going to use it throughout. Management uses it for almost everything, and it's the clearest read on the business model once you strip out the noise.

Management's definition is surprisingly honest: net income before interest, taxes, D&A, transaction-related acquisition and integration costs, and non-recurring items. And yes, SBC is left in (Honeywell, for one, strips it out…). Nothing is swept under the rug. It's just the least-bad way to compare ISSC's performance after one acquisition or after three.

In either case the adjusted figure stays reasonably close to reported EBITDA: the spread between adjusted EBITDA and reported EBITDA has ranged from 4% to 14% over the last three fiscal years.

Management was projecting (on a trailing twelve months basis): +40% revenue, +75% adjusted EBITDA, and EPS accretive (one would hope). Based on these numbers and ISSC’s pre-deal reality, you get incremental EBITDA of $8M and therefore a payback in 4.5 years. To sum up, the line was acquired at a multiple of roughly 4.5x EBITDA.

Reality delivered: revenue +54%, adjusted EBITDA +75%, and EPS +28%. Clearly an economic and strategic success.

In July 2024, ISSC put another $4.2M on the table for a complementary comm/nav line. Just a small asset acquisition (no goodwill) that follows exactly the same logic as the first.

At this point ISSC has shown three things:

It has a strategic vision and is capable of executing it efficiently.

Even a modest pace of future acquisitions can structurally change the P&L.

It is ready for wave 2.

Wave is clearly an understatement. The impact looks more like a tidal wave. It radically transformed ISSC.

You can't understand the company as it is today without grasping everything its next acquisition implies.

3.2 Wave 2, Great Leap Forward

Pro subscriber can skip this section and jump straight to the full report below. Alpha doesn't wait.

One undiscovered company at the right price makes the cost of this newsletter trivial. I am convinced this company, at this price, is one. The next deep dive is already in the works.

By going Pro, you also get access to all previous deep dives of the same quality, and obviously, the ones to come (one to two per month, plus follow-ups).

Become a Pro Member

You can get free access to paid content by sharing this newsletter with your network. 3 new subscribers = 1 month, 8 = 3 months, 15 = 6 months.