Atlas Salt: The Best Risk/Reward Setup I’ve Seen in My Career

500+ hours of work condensed into 40,000 words, for free.

I do not write that lightly.

At first glance, the company is easy to dismiss. It operates in a corner of the economy most investors do not even know exists, with no close publicly listed peer, and almost no natural public-market investor base.

The fact that the project exists at all is unusual: North America has not seen a comparable new entrant emerge in a generation. In this market, a company needs a rare combination of scale, cost advantage, logistics, customer relevance, and timing before it can even matter. This company has all of them.

Disclosure: I have skin in the game. I’ve been a shareholder for months, and I bought more during the writing of this investment thesis. That creates an obvious bias. The only honest way to handle it is to make the machinery visible: every assumption, every number, every calculation, and every place where the conclusion could be wrong. Do not take my word for it. Check the work. Then check it again.

The aim of this piece is to make the entire chain explicit: the upside, the downside, the assumptions, and the asymmetry between them. I spent over 500 hours on this thesis, condensed into 40,000 words, because the full answer emerges when you grasp the whole picture.

That level of work is deliberate. I spend 90 hours a week analyzing businesses, writing, reading filings, rebuilding models. This newsletter is where I publish the work, and I want it held to the same standard.

If this is the kind of work you want more of, join the list.

The valuation section includes the full DCF, with every figure and assumption made explicit.

There is a second thesis tied to this one: a different way to own the exact same setup. It rests entirely on the work below, so read this first. I save it for the end.

Table of Contents

01. An Overview of the Company

02. The Salt Market

The $26 Billion Picture

Not All Salt Is Created Equal

One Molecule, Three Jobs

TINA

The Implication for an Upstream Producer

How the Market Actually Works

The Buyer Side

The Seller Side

Demand That Does Not Bend

A Supply Base Frozen Since 2001

Import Dependence, Weeks Away

Pricing Without a Market

Where the Margins Are

Climate & Environment: The Objections That Do Not Stick

Where This Leaves Us

03. Atlas Salt’s Mine: Great Atlantic Salt

The Deposit

Transport Logistics as a Moat

The Operational Design

The Social Component

Permitting

Jurisdiction and Community

Environmental Profile

04. The Business Model

The Product: One Feedstock, Several Commercial Formats

Where Atlas Plans to Sell

How It Actually Sells: CIF, DAP, FOB

The Contracts

Scotwood Industries: Commercial Offtake + Canadian JV

Sandvik Mining: Equipment + Vendor Financing

Hatch Ltd.: Lead Engineering & IPD Partner

Continental Conveyor: Material Handling + IPD Partner

05. Management and Alignment

The Operators

Patrick Laracy: The Founder Who Stayed

Rowland Howe: The Man Who Knows the Competition

Nolan Peterson: The Executor

The Construction Bench

The Cap Table

The Royalty

What Laracy’s Alignment Means for Shareholders

The Net Read

06. A Quick Look at the Financial Statements

The Wrong Place to Look for Value

Balance Sheet Snapshot

The Cash Question

The Next Step

07. Financing

What Atlas Needs to Fund

The Debt Architecture

The Cost of Financing

What to Watch

08. The NPV: Decoding the C$920M Headline

The Revenue Side

The Price

The Volume Schedule

The Escalation

The Cost Side

The Build

Sustaining Capital

Operating Cost

The Royalty and the Taxes

The Sensitivity Analysis

The Discounting Mechanics

Why 8%?

My Choice of Discount Rate

09. Risks

The Financing

The Build

The Commercial Ramp

The Salt Price

The Permitting Tail

The Port Agreement

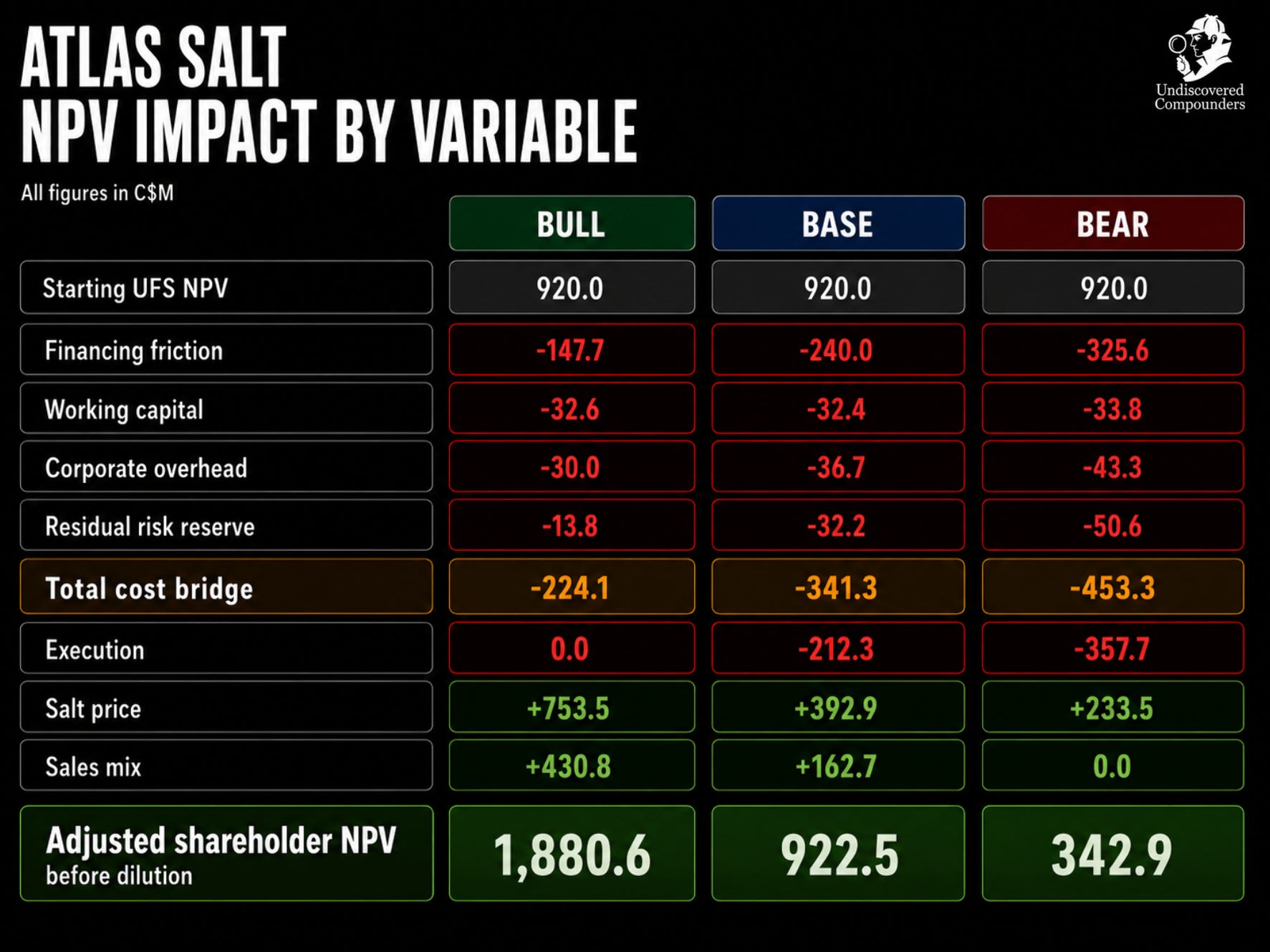

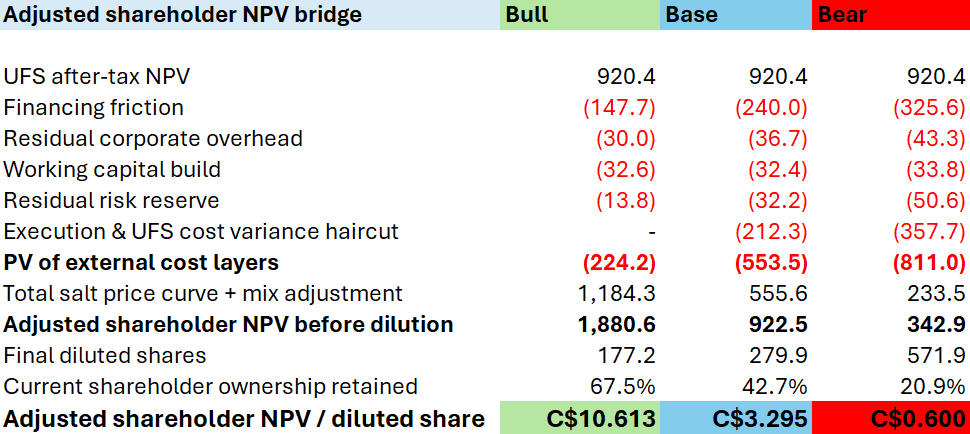

10. Valuation

The Ratio and Its Double Reading

Qualitative Valuation

Quantitative Valuation

Financing Costs

Working Capital and Corporate Overhead

Residual Risk Reserve

Execution

Salt Price

Sales Mix

Dilution

How Much Is Atlas Salt Worth?

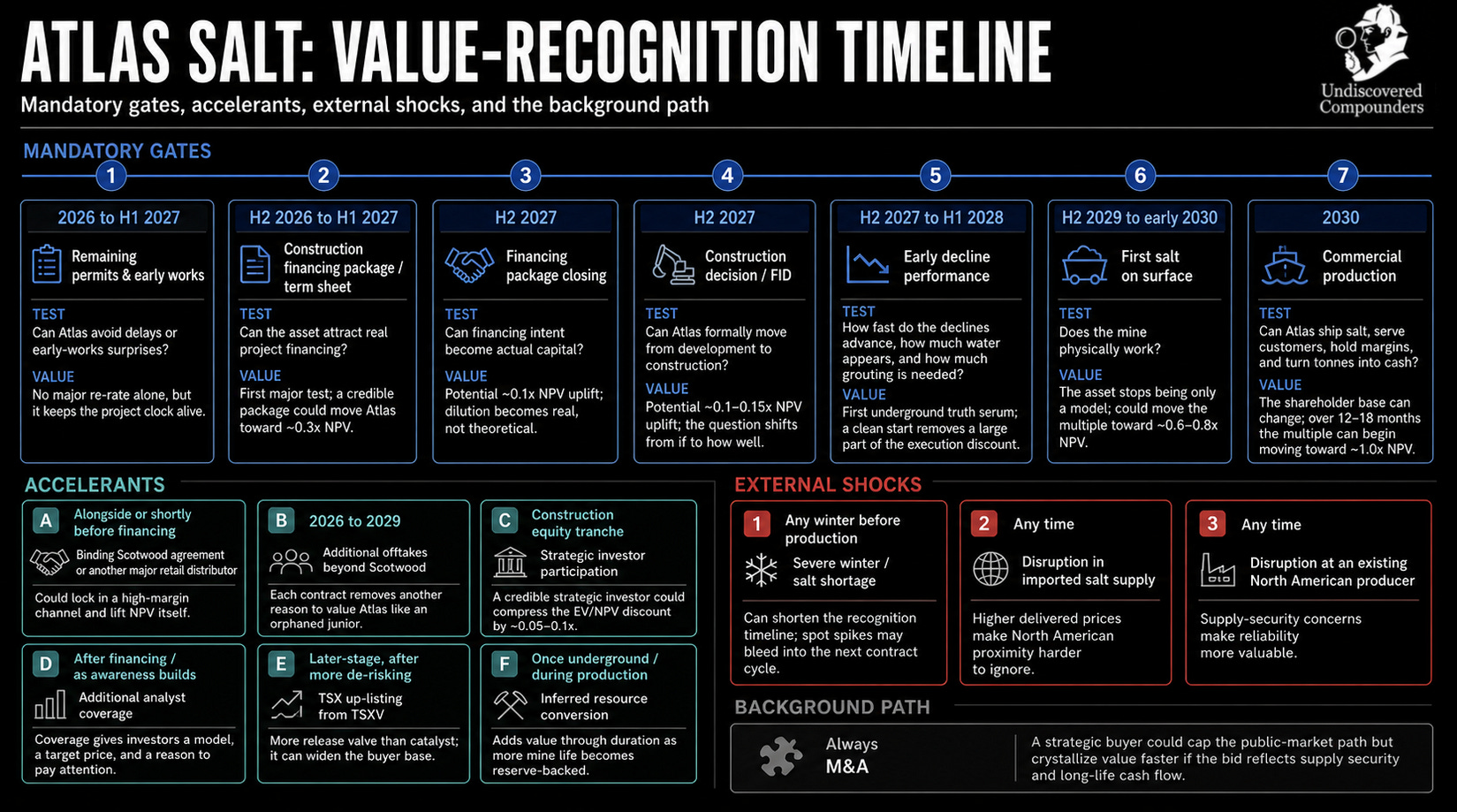

11. Repricing

Recognition

The Critical Gates

The Variables

The External Catalysts

Timing and Sequence

Sit-on-your-Ass

Someone Else Pays

Why M&A

When M&A

Management’s Take

Signals to Watch

12. My Final Take

13. A Better Way to Play the Setup

01. An Overview of the Company

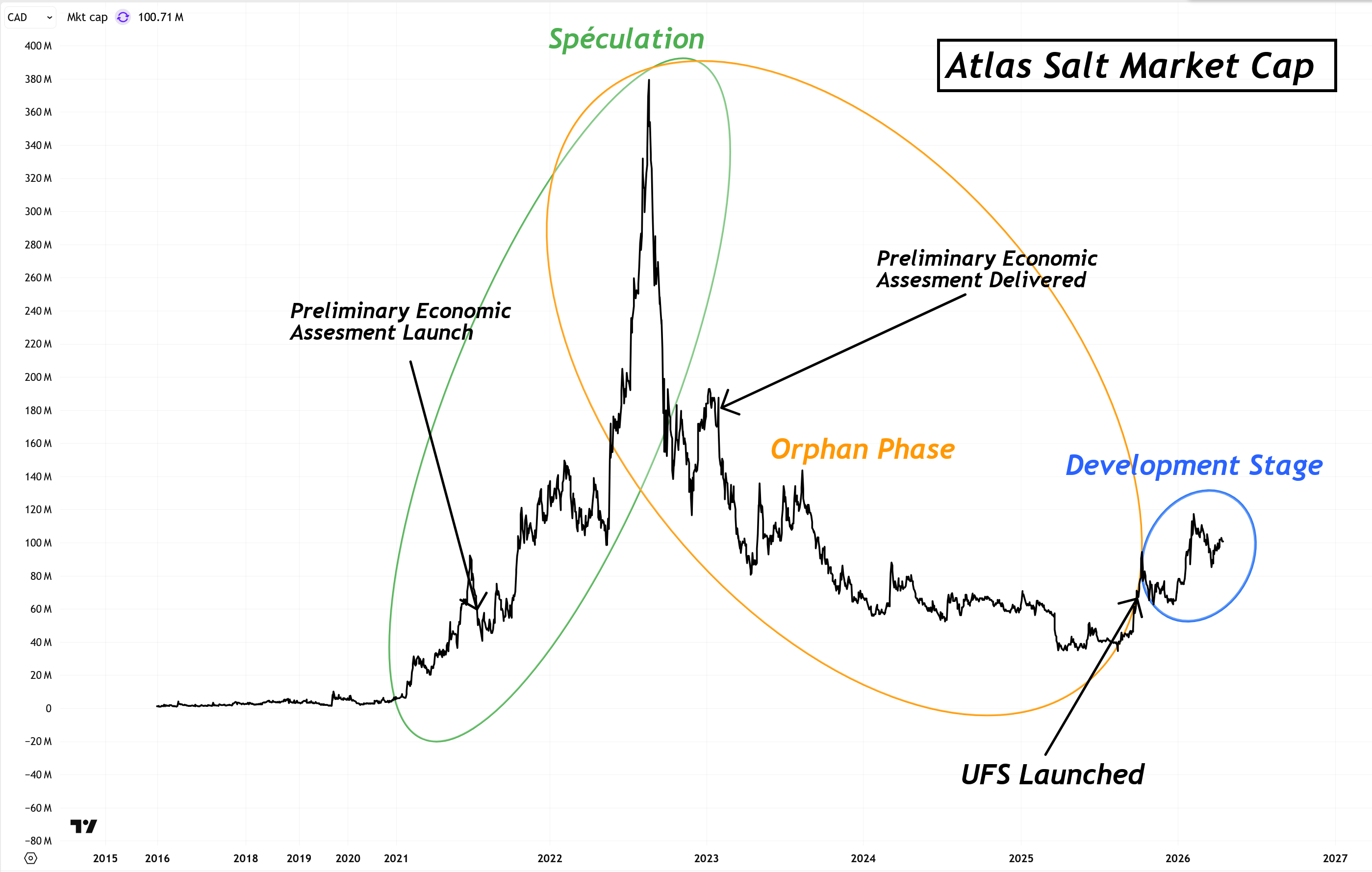

The company is Atlas Salt Inc., listed under the ticker SALT on the TSX Venture Exchange and SALQF on the OTC market in the United States. Its market cap is around C$120 million (US$88M).

The project, Great Atlantic Salt, is a planned underground salt mine in Newfoundland and Labrador (NL), Canada, wholly owned by Atlas Salt.

If that sentence made you want to stop reading, that is exactly why I think it is so cheap.

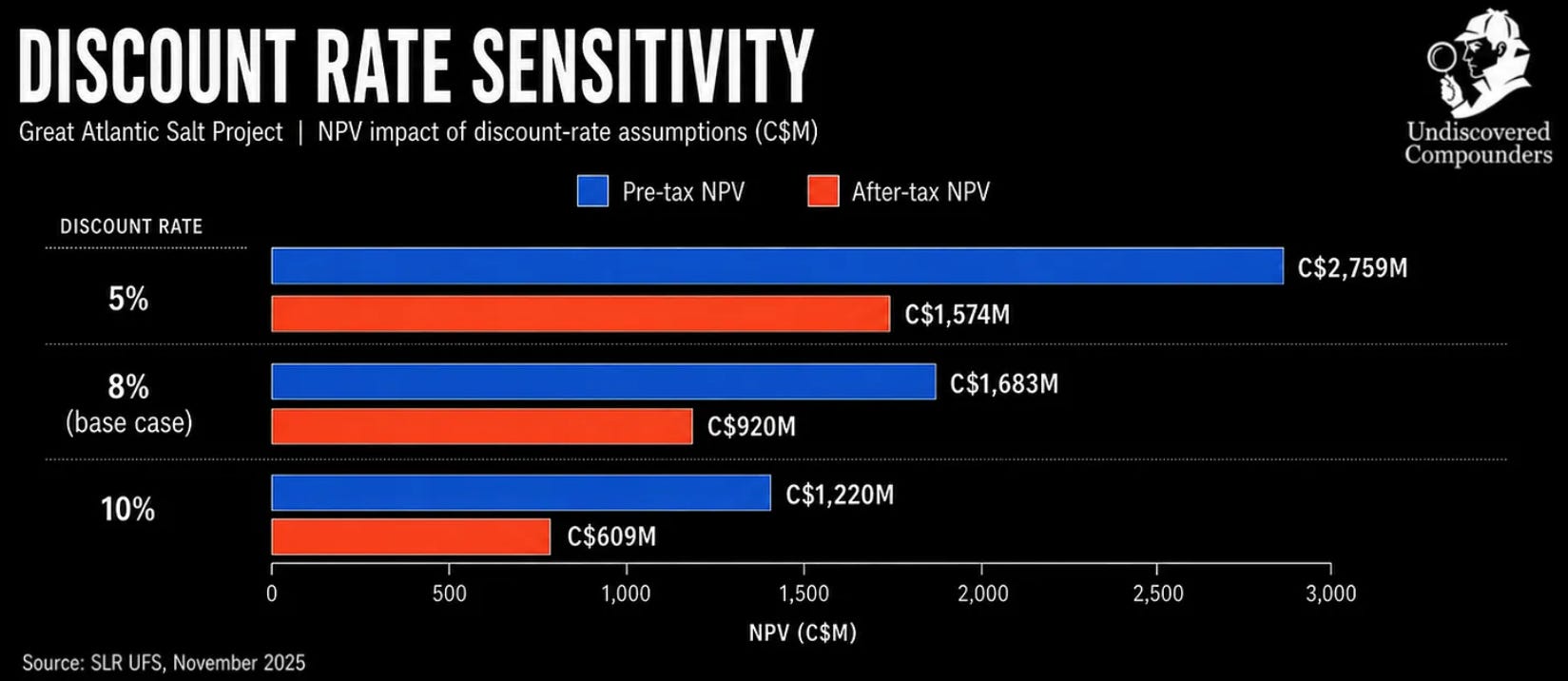

The 2025 Updated Feasibility Study (UFS) gives Atlas a 24.25-year reserve-case mine plan:

95.0 Mt of Probable Reserves,

C$272 million of average annual pre-tax cash flow,

and a C$920 million after-tax NPV at an 8% discount rate.

That is only the reserve case. The 95 Mt sits inside a much larger resource envelope: 288 Mt of additional Indicated Resources + 868 Mt of Inferred Resources, to which the UFS assigns no value.

Atlas trades at a P/NPV of approximately 0.13x,1 about 1/2 to 1/3 of the level at which comparable feasibility-stage mine developers typically trade, even though many of them arguably carry more risk than Great Atlantic Salt.

In the last eighteen months, Atlas has rebuilt the team around construction. A new CEO was hired. The project now has tier-one names attached across the build chain: non-binding MOUs on equipment, financing support, distribution, and engineering/delivery. Early works have started on site. The project-financing process is now underway.

The stock still trades as if almost none of that progress has been priced in.

And that is before the main point of the thesis.

My conviction is that the UFS materially understates Great Atlantic’s earning power. Most of the next 40,000 words are the work behind that sentence.

The first step is the salt market itself. A large part of the story, and a large part of the mispricing, sits there.

02. The Salt Market

In January 2026, for the second consecutive year, parts of Ontario ran out of contracted deicing salt supply and turned to the spot market. Emergency spot prices reached nearly C$300 per tonne, more than 4x normal bulk pricing, in a matter of weeks.2

More than a hundred trucks lined up outside Goderich, the world’s largest underground salt mine, waiting for product the mine couldn’t deliver fast enough. Municipalities were rationing supply, spreading salt at just a quarter of normal rates, while private contractors scrambled for every tonne of deicing salt they could find. They were paying nearly C$300 per tonne for what little they could get. They had to. And in a hard winter, they will again.

This is what an undersupplied and fragmented market looks like when winter hits. And yet, the salt market has no exchange ticker, no ETF, and no CNBC segment. A product as old as civilization, a use case nobody finds exciting, and a US$26 billion market that Wall Street can’t be bothered to cover.3 Precisely the kind of sector worth digging into.

The $26 Billion Picture

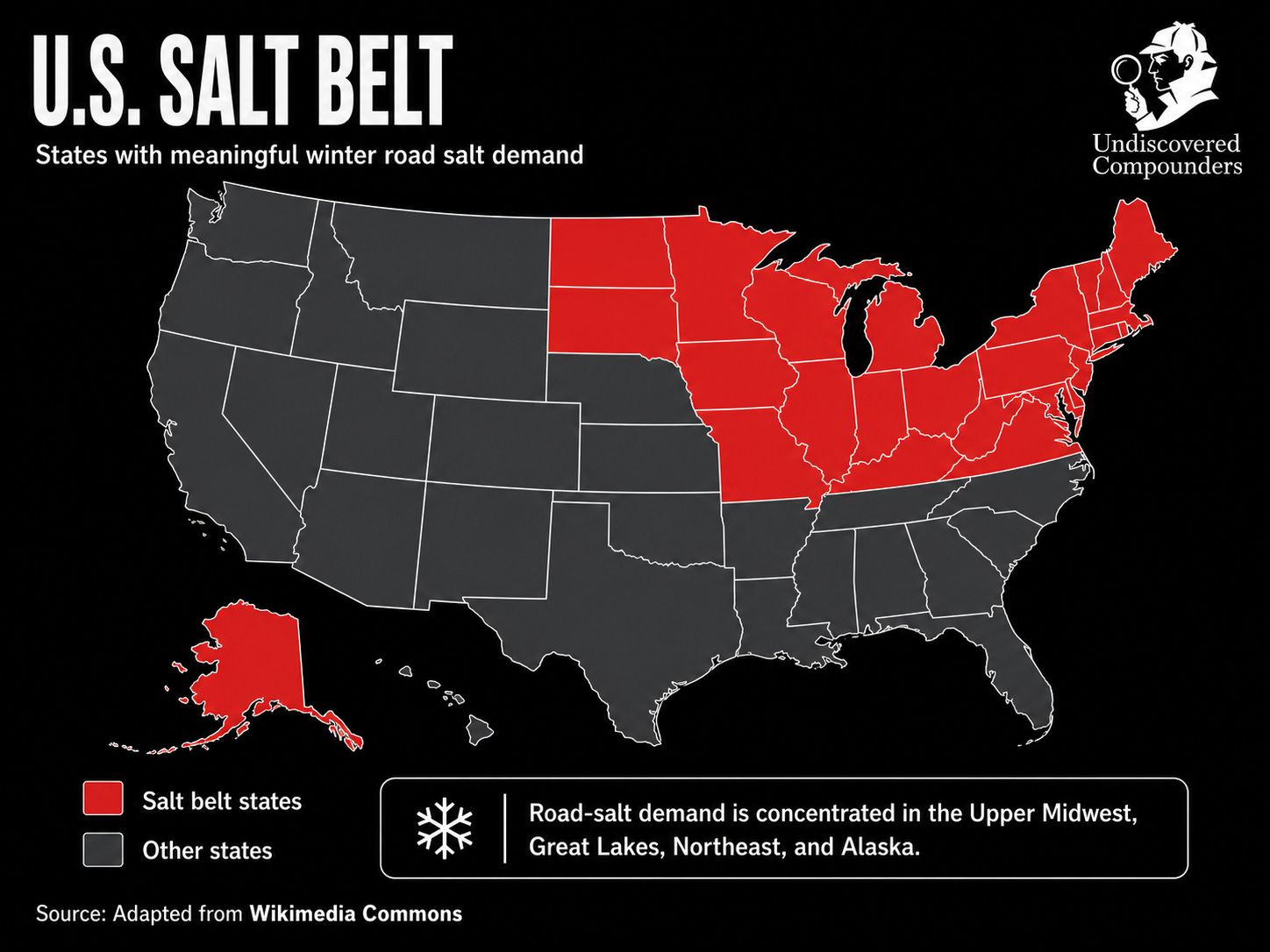

The global salt market is worth around US$26 billion, with annual production of approximately 270 million tonnes. Deicing is only about 13% of global salt demand, and even that demand is not spread evenly across the map. It sits where winter actually forces governments to act: North America and Northern Europe. Northern Europe matters, but it is approximately one-quarter the size of North America’s deicing market. So we start here.

And even North America is too broad. Road salt is not really a continent-wide market. It is a logistics market wearing a commodity label. The core sits in the East, where winter is frequent and unforgiving. For Atlas, the relevant map is therefore much smaller: eastern Canada and the U.S. East Coast.

The eastern North American deicing market consumes between 30 and 36 million tonnes of salt in any given year, depending on winter severity.4 This is, for all practical purposes, one cross-border physical market, even if it remains fragmented commercially and logistically. Canadian rock salt moves into American cities, and American production moves north into Canada.5 In plain terms, the border is broadly administrative.

The U.S. accounts for the majority of this consumption and provides by far the most granular public data. The analysis that follows relies on U.S. data because that’s where the data is, but in practice, market dynamics are similar enough on both sides of the border for the U.S. data to be useful.

In most commodity markets, a persistent supply gap attracts capital, but not in eastern North American salt. When a product can cost more to ship than to produce, every additional kilometer is a burden. That is where the economics are decided, including Atlas Salt’s future economics.

Not All Salt Is Created Equal

Walk through any Department of Transportation (DOT)6 yard in February and you’ll see the same molecule in three or four different forms. A dome of dry rock salt. Tanker trucks of clear liquid brine. A second pile, slightly damp and faintly brown, coated with magnesium chloride and an organic additive. At the spreader, an operator sprays more brine onto the dry salt as it leaves the spinner.

At the center of all of it is sodium chloride. The variations are delivery systems around one feedstock.

The standard taxonomy sorts salt by production method and hides the chain underneath.

Rock salt comes straight out of a mine.

Brine is rock salt dissolved in water (in winter maintenance).

Vacuum pan salt is produced by evaporating purified brine back into crystals.

Only solar salt takes a different path: seawater or lake water evaporated by the sun in coastal ponds.

All four are sodium chloride and all four can melt ice.7 The market is still not a four-way contest. Vacuum pan salt does not belong on highways, it is too expensive for that. Its markets are food, pharma, and industrial applications. Brine reaches the road as a liquid for anti-icing and pre-wetting, and the brine DOTs spray is almost always made on-site by dissolving rock salt in water. Collapse the chain, and the deicing market has two real upstream inputs: locally mined rock salt and imported rock and solar salt from coastal evaporation ponds.8 Everything between the mine and the road is downstream chemistry around one of those two.

One Molecule, Three Jobs

Winter maintenance runs on three operations.

Anti-icing happens before snow falls or freezing rain begins. Crews spray a liquid brine onto dry pavement hours ahead of the event, typically a 23.3% NaCl solution, the eutectic concentration9 of sodium chloride in water. The brine leaves a thin salt film on the pavement and stops ice from bonding to the asphalt. When the storm arrives, plows can clear the road. Anti-icing has become standard practice across most snow-state DOTs because it prevents snow and ice from bonding to the pavement, making plowing more effective and materially reducing the amount of chemical needed versus reactive deicing alone.10

Deicing is the reactive application during and after the storm: dry or pre-wetted salt spread onto bonded snow and ice to break the bond so plows can scrape it off. This is what most people picture when they think of “salting the roads.”

Pre-wetting is the in-between move. Liquid brine is sprayed onto the dry salt at the spinner, just before it hits the pavement. Wet salt sticks to the road instead of bouncing into the ditch. It dissolves faster and starts working sooner. Agencies that use pre-wetting properly report 20% to 30% reductions in total salt usage at the same level of service.11

Less rock salt, then? Atlas is going to mine rock salt. Bad for business, right? No. Where brine is used, it is usually made on site by dissolving rock salt in water. Treated salt is rock salt coated with small amounts of chloride brine and, in some cases, organic additives. The dry salt is rock salt.

A single tonne mined in Goderich or Cayuga, or eventually in the future Atlas Salt’s Great Atlantic Salt, can leave the mine and end up on the road as dry crystals, as 23% brine, or as treated salt with a chemical coating. The downstream chemistry is the buyer’s local decision. The upstream supply is the same molecule from the same kind of mine.

TINA

Calcium chloride and magnesium chloride sometimes get called “alternatives” to road salt, which misreads what they do. Their economics, at 3 to 5 times the cost per tonne, rule them out as primary deicers. Their job is narrower: extending the working temperature range of a rock salt program.

Sodium chloride starts losing effectiveness around -10°C. Calcium chloride works down to approximately -25°C, magnesium chloride down to about -15°C. When pavement temperatures collapse, agencies do not switch to calcium chloride across the board. They spike a calcium chloride solution into their brine, or coat their rock salt with it, and get the extra temperature range without paying full alternative-chloride prices on every tonne. Most treated salt is some version of this: rock salt with a brine coating that extends its useful range by 10 to 15 degrees.

Acetates and formates are a separate category. Potassium acetate, sodium acetate, calcium magnesium acetate, and related products do not contain chloride; they are therefore generally less corrosive. That matters mainly in two places. Airports, where chloride contact with aircraft is a non-starter and deicing products must meet specific aviation standards. And a small set of bridges and parking structures where corrosion risk can justify paying 10 to 20 times the cost of rock salt.12 Everywhere else, acetates and formates remain a rounding error in volume.

Sand and abrasives are also used, but they play a different game. They do not melt anything; they provide traction on top of ice when temperatures drop below what any chemical can fix, or on rural roads where the cost-benefit math does not justify a chemical program at all. Most agencies that use sand still mix in 5% to 10% salt to keep the stockpile from freezing solid.13

I will leave the final word to the United States Geological Survey14:

“No economic substitutes or alternatives for salt exist in most applications.”

The Implication for an Upstream Producer

A rock salt mine sits upstream of the entire deicing system. Dry tonnes for direct application. Brine feedstock for anti-icing programs. Base material for treated salt and pre-wetted formulations. Almost every operation, every chemistry trick, every “smart-salting” innovation municipalities have adopted over the last two decades starts with rock salt.

Atlas sits at that input point: dry salt for direct use, feedstock for brine and treated products, and emergency tonnage when winter breaks the procurement plan. It is building a feedstock source for a system already under strain, and in hard winters, one setback away from breaking.

Let’s focus on the strain.

How the Market Actually Works

The Buyer Side

The buyers split into three tiers.

The first is government: state and provincial Departments of Transportation (DOT), counties, municipalities, the people who keep highways open or get blamed if they do not. Together they account for approximately 70 to 80% of North American deicing rock salt consumption (a national average; the split varies meaningfully by state and by density of development).15

The second tier is commercial. Professional snow management companies servicing parking lots, warehouses, hospitals, and corporate campuses under seasonal contracts, plus the facility managers of large retailers and logistics operators who buy directly. About 15% to 20% of volume.

The third is retail. Homeowners buying 10 kg bags at Home Depot, Walmart, grocery stores, and hardware stores. The remaining 5% to 10%, give or take, is an entirely different economic creature. The buyer here is the person who slipped on their own porch last February and decided never again.

The three tiers buy on completely different terms.

Government buys most of its deicing salt on the calendar. A state DOT or provincial transportation agency signs its contracts months ahead of winter, usually between May and August, for a season that won’t start until November. The salt is usually delivered in September and October, stored in the salt domes and sheds you see along the highways, and used through April. The public buyer usually does not buy from a single national supplier; it carves its territory into zones (e.g., Massachusetts has eighteen contract zones) and each zone is awarded to a single vendor for the entire season. The contract sets a volume band: the buyer commits to a minimum, usually 60-80% of estimated quantities, and the vendor commits to a maximum of 110-140%.16 Anything above that contracted band falls outside the contract economics. Once the protected tonnage is gone, buyers are competing for uncommitted supply at market prices. Call it spot, emergency supply, or panic procurement; the mechanism is the same. Ontario in January 2026 was just the mechanism in public view. Counties and municipalities buy in smaller quantities, sometimes through their own contracts, more often through pooled bids run by a state or provincial agency to capture the volume discount.17

Commercial buyers play a harder game. Their contracts are usually signed between a property owner or facility manager and a snow management contractor, not directly with a salt supplier. The pricing model determines who carries the weather risk:

In a per-push contract, the contractor gets paid each time crews service the site.

In a per-inch contract, the price rises with snowfall depth.

In time-and-materials contracts, labor, equipment hours, salt, and other materials are billed as used.

In a seasonal flat-rate contract, the customer pays one fixed fee for the winter, regardless of how often it snows.

Each model transfers weather risk differently, but all of them end in the same place: the contractor has to source the salt.18 There are approximately 22,000 commercial snow contractors in the United States.19 Most of them buy from a regional bulk distributor. That layer exists precisely because integrated producers won’t build a commercial team, a dispatch desk, and a fleet of trucks to chase 22,000 individual contractors, many of them ordering a few hundred tonnes. The math only works at public-bid scale.

Retail does not really buy; it panics (yes, I’m still talking about deicing salt). When a storm is forecast, shelves empty. Season-to-season demand is more volatile than the two bulk tiers, but the long-run floor is the same: across much of the Northeast, homeowners and property managers are expected, and often legally required, to keep sidewalks and walkways clear. A slip-and-fall claim20 turns a ten-dollar bag of salt into cheap insurance.

Everyone needs salt before the storm. But not everyone can get it on the same terms. That is why a 10 kg bag of salt can end up costing several times more per-tonne than the bulk road salt purchased by a DOT, even before a storm hits.

The Seller Side

On the seller side, 4 structurally different types of players exist. Each controls a different bottleneck.

The first is the integrated producer. Compass Minerals owns the Goderich mine, operates the mine-site loading infrastructure, controls an extensive network of regional storage depots, contracts for bulk vessels, barges, rail, and trucking, and sells directly into public-sector contracts. This end-to-end integration took decades to build, but it allows the producer to invoice on a delivered-price basis. Almost all major North American rock salt producers are integrated this way, and that is part of what makes the segment effectively closed to direct competition.

The second is the port operator. Take Eastern Salt. It does not need to own the mine. It owns or controls the local bottleneck: bulk vessel unloading, storage, trucking, and relationships with public buyers. Eastern Salt buys imported salt from foreign producers, brings it into its terminal, stores it, and resells it at a delivered price to the same public buyers. Without this intermediary layer, distant importers would struggle to sell physical tonnes into the United States.

The third is the regional bulk distributor. Companies like Midwest Salt, Ninja De-Icer, or SISCU. They do not mine anything. They buy in volume from integrated producers, from port operators, and sometimes directly from exporters, then they store the salt in their own depots and resell it in flexible truckloads to the thousands of contractors no integrated producer wants to serve directly. They run 24/7 in season and deliver next-day, sometimes same day. They’re the lubricant that lets an already-tight system function, until the salt itself becomes the constraint. Lately, that has meant many winters (more on the causes and consequences later). Without them, the commercial tier collapses.

The fourth is the distant importer, mainly Chilean, Egyptian, and Moroccan producers. They load a bulk carrier at the port of origin, cross the ocean in two to four weeks, and unload dockside in Boston, Philadelphia, or Baltimore. They own nothing in the United States. They sell to a port operator or to a distributor with import capacity, and that buyer takes it from there. What makes their model economically viable despite the distance is their extremely low FOB port (Free on Board, the price at the port before shipping costs): dry climates that allow solar evaporation, lower labor costs, open-pit mines with no underground CapEx. Even after 2-3 weeks of ocean freight, the dockside cost in Boston can still remain competitive.

Integrated North American producer, port operator, regional distributor and distant importer. There is one box with no relevant occupant today: a North American producer that sells dockside without downstream integration, the way an exporter would, but a few days from the market instead of a few weeks. No great mystery here: no new rock salt mine has opened in North America in nearly twenty-five years, and the existing mines are almost all integrated by historical inheritance. Atlas Salt could therefore establish a new category, unless it is acquired first (a scenario we’ll cover later).

In short, here is the structure of the deicing rock salt market:

Demand That Does Not Bend

About 70% of U.S. roads are in snowy regions, and nearly 70% of the population lives there. Most deicing salt consumption is concentrated east of the Mississippi. Highway deicing alone accounts for about 41% of total U.S. salt consumption.21 That single application ties year-to-year deicing demand to one variable above all else: how harsh the winter is. “Harsh” here means the frequency of precipitation events that cross the freezing threshold, not temperature alone. Several low-snowfall icing events can consume more salt than a single large storm, which is “good” news for suppliers, because those events occur more often.22 Even during normal winters, North America still imports 8 to 10 Mt of deicing salt, leaving a clear source of demand for a new local supplier able to deliver more reliably.23 Atlas Salt is the only new local greenfield supply candidate positioned to fill that role. The only one in decades.

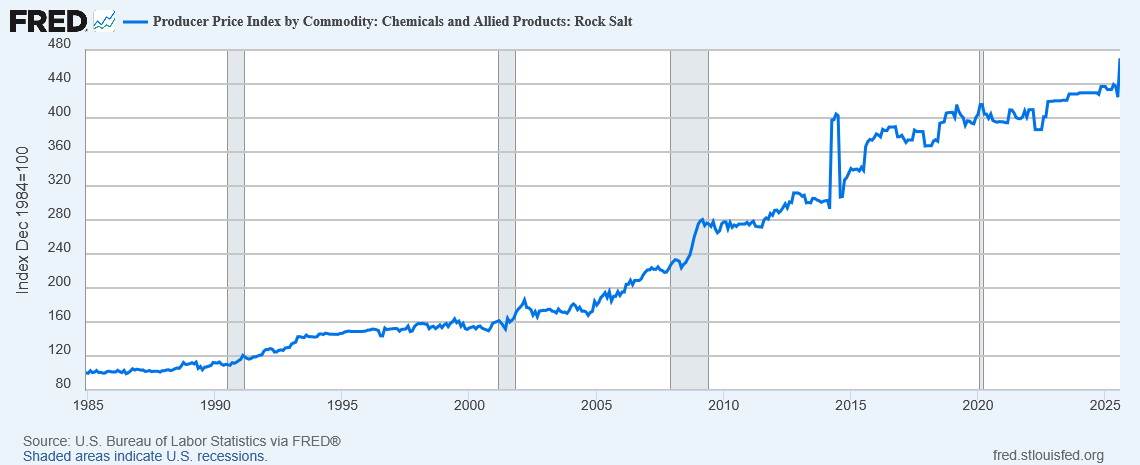

On the downside, demand has a built-in floor. State DOTs and provincial transportation agencies operate with minimum stockpile targets regardless of how mild the previous winter was. A warm season spreads its demand reduction across subsequent years as agencies draw down reserves before reordering. Private contractors operate much the same way, although they are often the last to be supplied and the first to return to the market when winter conditions turn severe. This asymmetric structure is what makes the market so attractive: demand can surge in any given year, but it rarely drifts far below its baseline. And it shows in the price. Over the past 40 years, U.S. rock salt PPI has compounded at 4% per year versus 2.8% for CPI, and the largest cumulative price decline never exceeded 10%, outside of post-spike corrections. On a chart, it looks like a compounder on a log scale.

This chart is one of the most important in this investment thesis. Salt price is the single most important variable in the investment case, by far. The BLS index tracks the prices received by domestic rock salt producers on their first commercial sale, whether to a DOT or through an intermediary. National, weighted, and smoothed by design. It hides three things.

First, geographic price dispersion: a DOT hundreds of miles inland pays far more per tonne than one next to a lake port, because salt’s low value-to-weight ratio means logistics dominate the delivered cost. The national average erases that gap. Second, downstream markups: the index captures what the producer receives, not what the distributor charges a private contractor three layers down. Between the mine gate and the parking lot, margins expand significantly. Third, and most importantly, spot pricing: the channel where both DOTs and private contractors scramble for every available tonne when winter runs harder than the procurement contracts anticipated.

That spot market is where crisis prices live. Ontario’s 2025-26 winter is the extreme case, but the same mechanism plays out at a smaller scale in many harsh winters, invisible in the headline index. The chart is therefore a proxy for producer pricing with the upside spikes flattened. It hides the operating leverage of every salt producer. In the valuation section, this chart will be our base case. Note that spot-price spikes tend to flow through into the next contracting season, as buyers and suppliers reset expectations around scarcity and replacement cost. Given the spot-price spikes observed in several regions during the 2026 winter season, contracted salt prices are likely to move higher in the next tender cycle.

To understand why public buyers end up paying several times the normal price,24 you have to think like them. As always, it comes down to incentives. Research on a 30-mile Iowa highway segment found accidents increased 1,300% when maintenance was disrupted during severe winter weather events, even as traffic volume fell.25 That 14x multiplier translates into lawsuits, emergency response strain, and political cost for whoever made the call. No politician on either side of the border wants to be the person who let roads go unplowed. Cities apply salt at the first sign of freezing precipitation, and keep applying as long as the supply holds. Private snow-removal contractors operate on the same arithmetic, through a different legal regime. A slip on an unsalted parking lot can become a lawsuit against the property owner. The incentive structure is identical; only the courtroom changes. For both public and private entities, when salt is needed, the money is found.

But sometimes there is simply no salt. The 2008-09 season was the clearest example: depleted stockpiles from the prior winter + Mississippi flooding + hurricane-damaged Louisiana mining equipment = a perfect storm. Iowa DOT opened bids for 31 locations and received… zero offers. The first time in the state’s history. I’ll let you imagine what that meant for the municipalities on the other end of those bids.26

And the public buyer still gets the “better” end of the deal. Private contractors sit below municipalities in every producer’s allocation queue. In early 2026, major suppliers like Morton Salt suspended commercial accounts across several states to prioritize public-sector contracts.27 Contractors received a single-line email from their distributors: “Everybody’s cut off. No more salt.”28 Around the same time, American Rock Salt raised its commercial price by $25 per ton in New York.

Demand is locked by public safety mandates and commercial liability, floored by winter stockpile behavior, prone to spike when winter runs harder than planned, with no viable substitute at any point in the cycle. Whatever goes wrong in this market, it won’t be on the demand side.

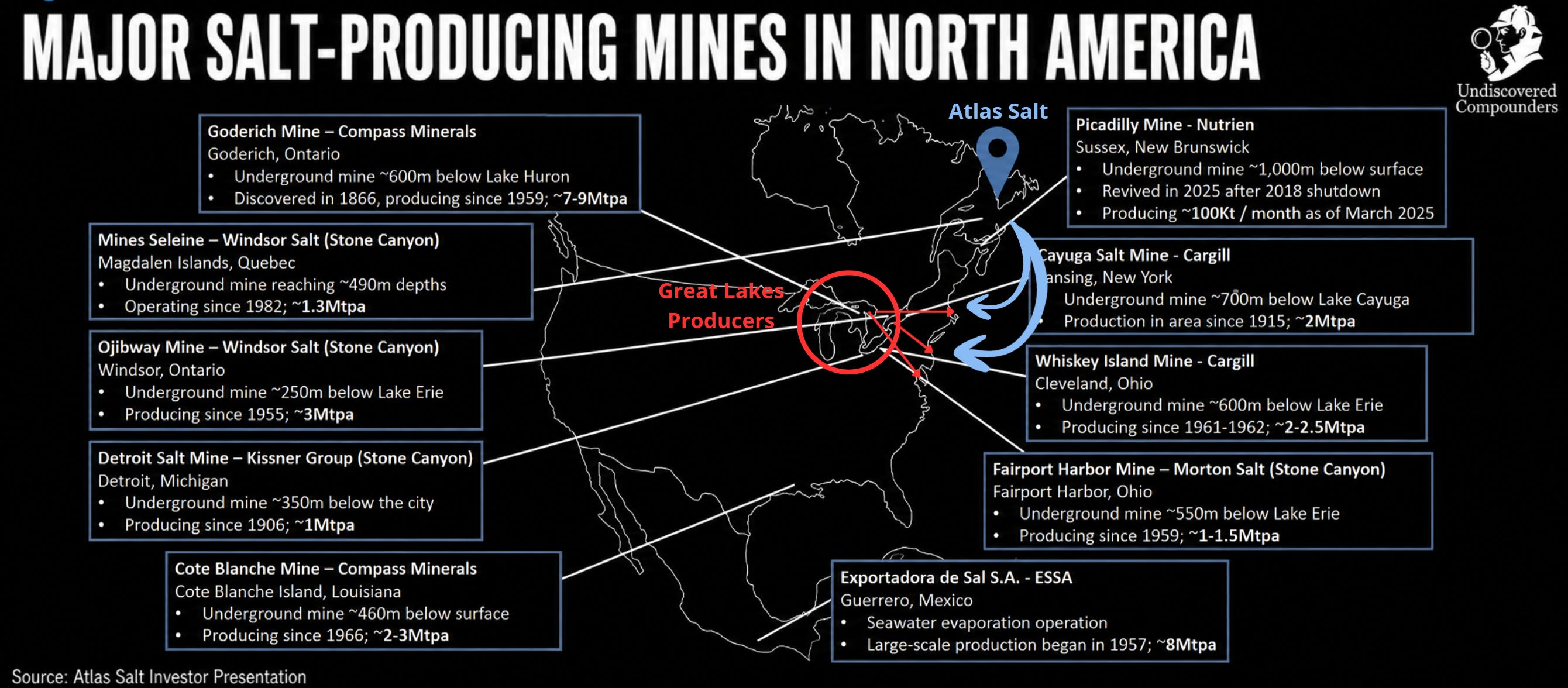

A Supply Base Frozen Since 2001

U.S. rock salt production in 2019 was 19.1 million tonnes.29 North of the border, the eastern supply base is heavily anchored by one asset: Compass Minerals’ Goderich mine, which produces approximately 7.25 million tonnes per year from 1,800 feet beneath Lake Huron. But rock salt does not only serve deicing; it also feeds chemical, industrial, and agricultural markets. Once those volumes are accounted for, domestic North American rock salt production falls well short of deicing demand alone. North America must import 8 to 10 million tonnes of deicing salt every year just to keep roads clear.

That gap is the persistent consequence of a supply base that has not expanded in over two decades while demand has quietly grown with population, road networks, vehicle miles, and service-level expectations.30

At the mine gate, U.S. rock salt is a low-value commodity, with benchmark prices around $50-$60 per tonne.31 Not an operating cost, but a producer-level selling price. But that mine-gate price can become an afterthought. In some lanes, transportation costs can exceed the value of the salt itself. This is why geography is the moat: the mine closest on the efficient shipping route usually wins. Short-sea shipping moves the same tonne for a fraction of what trucking costs. The mine closest to a deepwater32 port can serve the largest addressable market. A mine without port access serves whatever fits inside its trucking radius.33 Keep that in mind.

The last new rock salt mine built in North America began production around 2001. Before that, there had been no new mine for more than fifty years. The reason is purely economic: salt deposits are vast and widely distributed, but the revenue per unit is too low to justify the capital expenditure of a greenfield operation unless the logistics are exceptional.34 Even expanding existing mines is difficult: regulatory agencies may require complete facility upgrades to current standards if operators seek permits for new sections, creating compliance costs that are simply prohibitive.35

The major producing base is aging.36 Many of these mines sit hundreds of meters underground, beneath lakes or urban areas, with environmental and permitting constraints. Goderich is the clearest illustration. The mine experienced geological movements that disrupted production in 2017, followed by a three-month worker strike in 2018 that tightened supply across both sides of the border.37

And it is getting worse. Since 2021, North America has lost about 1.5-2.5 Mtpa (million tonnes per annum) of domestic capacity with the permanent closure of Cargill’s Avery Island mine (operating since the mid-1800s). Another 5.5 Mtpa remains in uncertain hands: Cargill’s remaining U.S. assets, both beneath lakes, have been listed for sale since 2023 with no buyer in sight.38 Compass Minerals, operator of the continent’s largest mine at Goderich, is under financial pressure: cutting production in 2024-2025 to pay down debt after a failed lithium diversification, a class action settlement, and a particularly damaging food-grade recall.39 Stone Canyon, North America’s largest salt producer by total volume, is digesting $5.2 billion in acquisitions.40 The rest are either absorbed in integrating existing assets or too regional to move the needle.

In this aging and saturated landscape, one name emerges: Atlas Salt, the only greenfield rock salt mine project in North America in 25 years with a completed feasibility study and early works underway. That scarcity is not a coincidence. The project has structural advantages that make the math work where it has not worked for anyone else in a generation. But that is only one project. For now, the continent still has to fill the gap somewhere else. It imports.

Import Dependence, Weeks Away

Deicing is the most important end use for imported salt. The question is where those 8-10 Mtpa come from, and what constraints they face.

After Canada, Mexico is the closest large foreign source for U.S. salt imports. But Mexican solar salt serves the U.S. West Coast and Asia almost exclusively. For the North American East Coast market, Mexican salt is out of the picture.41 Chilean and Egyptian solar/rock salt reaches the East Coast by ocean, a journey of 14 days or more. It is produced cheaply thanks to low labor costs, low extraction costs, and proximity to deepwater ports.42

When everything lines up, this system works. Imported salt can arrive at the same price, sometimes even cheaper, than the domestic product. It takes lower foreign production costs, favorable exchange rates, and ocean freight rates that undercut overland rail and trucking.43 But that cost advantage rests on everything going right, and it can reverse the moment one variable moves against them. Right now, with Brent having doubled in four months, nothing lines up for foreign salt exporters. And even if fuel prices collapsed tomorrow, cost is only the first problem; the others are time, priority, quality, and recourse.

Even when the salt arrives, it is not necessarily reliable. Distance means less visibility and less control over the counterparty. When a buyer sources foreign salt, it may not know whether it is dealing with a broker or the mine owner, whether its order will be prioritized, whether the product delivered will match the quality purchased, how long the vessel will wait before loading, or what dispute process exists if something goes wrong. Available salt can still become a reliability problem. And even if everything goes well, salt sitting two weeks away by boat cannot help a municipality that runs out of inventory in the middle of a storm. Only a few local producers can.

The policy environment has become less… comfortable with distant imports too. Non-USMCA sources like Chile, Egypt, and Morocco have also faced Section 122 surcharges of 10% following the February 2026 Supreme Court decision.44 USMCA-compliant Canadian salt enters duty-free.45 So far, Canadian road salt has remained outside the main U.S.–Canada tariff pressure points. Canadian rock salt qualifies as USMCA-originating by default, and USMCA-compliant goods remain exempt from the IEEPA tariffs hitting most other Canadian exports. Even if that changed tomorrow, the math would not move much. The deficit is too structural for buyers to source elsewhere, the end customer is a municipality that has to keep the road open, and most North American producers run on margins too thin to absorb a tariff themselves.46 The cost would land where it often lands in tight markets: on the U.S. consumer.

The U.S. has tried to promote domestic salt production, but policy cannot override physical reality. New York’s Buy American Salt Act (December 2022) allows state agencies to prefer U.S.-mined salt when the bid is within 10% of the lowest offer.47 But in practice, the policy mainly exposed how fragile domestic logistics still are. After the 2024-25 shortage, New York officials stepped back from applying the preference to the next road salt solicitation, explicitly stating that the Buy American Salt Act preference would not apply to the 2025-26 replacement contracts.48 They still need imports, and they need them nearby.

A demand floor with sharp spikes, and a supply base that shrinks to local producers when winter bites. In the middle of all this, Great Atlantic Salt is 2 km from a deepwater port on the Atlantic seaboard. The project alone cannot close the entire gap, but its economics are built around this market structure.

What’s left is where supply and demand meet: the price.

Pricing Without a Market

Salt has no liquid futures contract, no exchange-traded benchmark, and no transparent spot market. Pricing happens through negotiated physical contracts, awarded months before winter, or through emergency quotes when everyone is chasing the same tonne of salt.

Contract prices tend to move gradually upward, while emergency prices can reset violently when inventories run short. The buying logic is starting to move from pure lowest-cost purchasing toward security of supply, especially after the shortages of 2025 and 2026. That shift structurally favors domestic producers with proximity to end markets and the ability to respond within days. Atlas Salt can deliver salt in under three days to the nearest East Coast cities (Boston, New York, etc.).49

There is another slice of the deicing market I’ve barely touched so far. It is small in volume, but it plays by completely different economics.

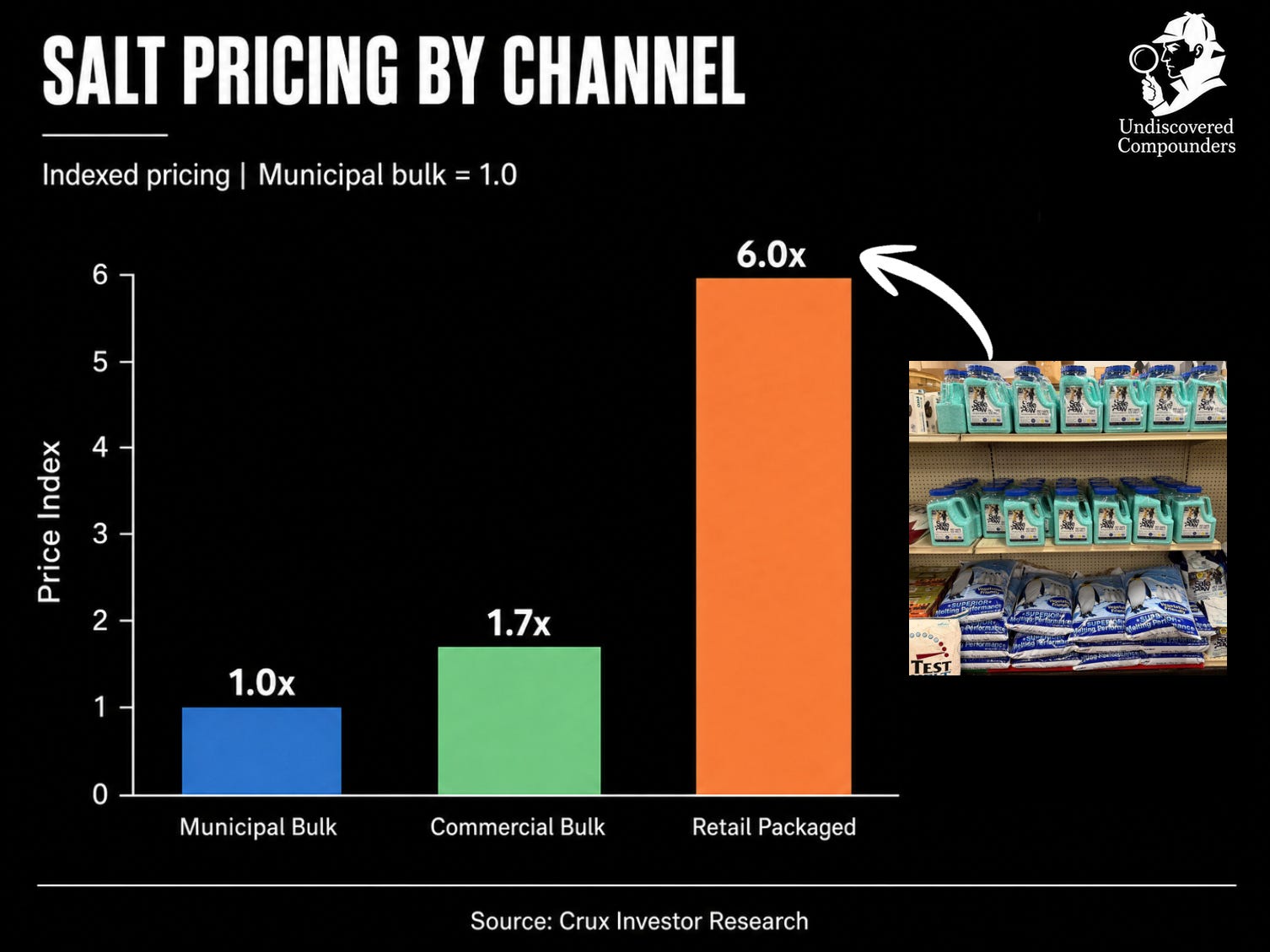

Where the Margins Are

In sales to public buyers, producer margins are thin. The counterparty is a government entity with a public-safety obligation to keep roads usable, and sometimes a legal obligation to do so. This is the floor.

Now take that same salt, bag it, slap a brand on it, and put it on a shelf at Home Depot. At the producer level, packaged salt already sells for almost 2x bulk. By the time it reaches retail, the multiple expands to approximately 6x. Make no mistake: it is the same salt: same NaCl, same purity, same mine. The markup is mostly a function of packaging, distribution, and channel access.

This is why evaluating a salt producer on average revenue per tonne is misleading. What matters is which channels they can reach: packaging lines, logistics networks, and shelf space at major retailers. Few producers have all three. Atlas Salt does not, and probably never will, at least not directly. That said, the company is already trying to capture part of those higher-margin segments through partnerships.

Climate & Environment: The Objections That Do Not Stick

Two objections come up every time someone looks at this market, and they deserve answers before we move to the setup. Both sound reasonable, but neither survives contact with the data.

The first: climate change will kill winter salt demand. No data points in that direction. Instead, climate change is changing the shape of demand. Total precipitation across the Great Lakes states has increased 14% since 1951, while the heaviest 1% of storms have become both wetter and more frequent.50 Warmer average temperatures shift more of that precipitation from snow to rain, and specifically to freezing rain, which can consume more salt per event than snowfall. Researchers studying county-level records from NOAA’s Storm Events Database from 1996 to 2025 found that freezing rain events are not declining. Instead, they are shifting in location and timing, moving later in winter and expanding into regions less prepared for them.51 As one research team put it52:

“We want to make an urgent warning that these kinds of winter hazards won’t be less frequent under a warmer climate.”

Climate change makes deicing salt demand less predictable, more concentrated in peak events, and more punishing when supply cannot respond. That, once again, favors producers with proximity.

The second: environmental regulation will restrict road salt. Here the picture is more nuanced. The pressure is real: chloride accumulates in freshwater systems, and the EPA sets toxicity thresholds at 230 mg/L for chronic exposure. Several states have tightened water quality standards. But the regulatory response on the East Coast has been the same: optimize application, do not eliminate it. Pre-treatment brining, calibrated spreaders, GPS-controlled application, anti-icing strategies, and operator training are already part of the toolkit across public winter-maintenance programs.53 No relevant jurisdiction has moved to ban or materially restrict road salt use. The reason is the same one that makes this market what it is: there is nothing else that works at scale for the price.54

Climate change raises the peaks and, in some regions, the floor. Every efficiency gain of the last fifteen years has been absorbed by rising demand. Rock salt consumption is higher today than it was before chloride in rivers became a water-quality concern.

Where This Leaves Us

Every structural feature of this market shows up in a producer’s income statement: revenues, margins, cash flows.

Six structural facts, each compounding the next:

Demand that does not bend, locked by public safety mandates and by slip-and-fall liability on the commercial side, floored by winter stockpile behavior, compounding at nearly 4% a year for four decades in the floor case.

A supply base that has not expanded in twenty-five years and is showing stress: mines closing, producers under financial pressure, and capacity for sale in a market that still needs more local supply.

An 8-to-10-million-tonne structural import gap filled by salt that takes two to three weeks to cross an ocean.

No economic substitute at scale.

Climate change making demand less predictable and more peak-loaded.

A procurement model shifting from lowest-cost to security-of-supply, rewarding exactly what distant imports cannot offer: proximity and reliability.

This is a market that has already broken, visibly, and repeatedly. The structural conditions that caused the break are getting worse. Ontario in January 2026 was the system behaving exactly as designed, with no slack left.

Into this market, one company is building the only new salt mine in North America in over a generation. A shallow, high-purity deposit. Two kilometers from a deepwater port. An Atlantic port open while the Great Lakes are closed. Completed feasibility study. Environmental approval secured. Early works underway. And a valuation that prices in almost none of it. Even less of the market it sits in.

That brings us to Great Atlantic itself.

03. Atlas Salt’s Mine: Great Atlantic Salt

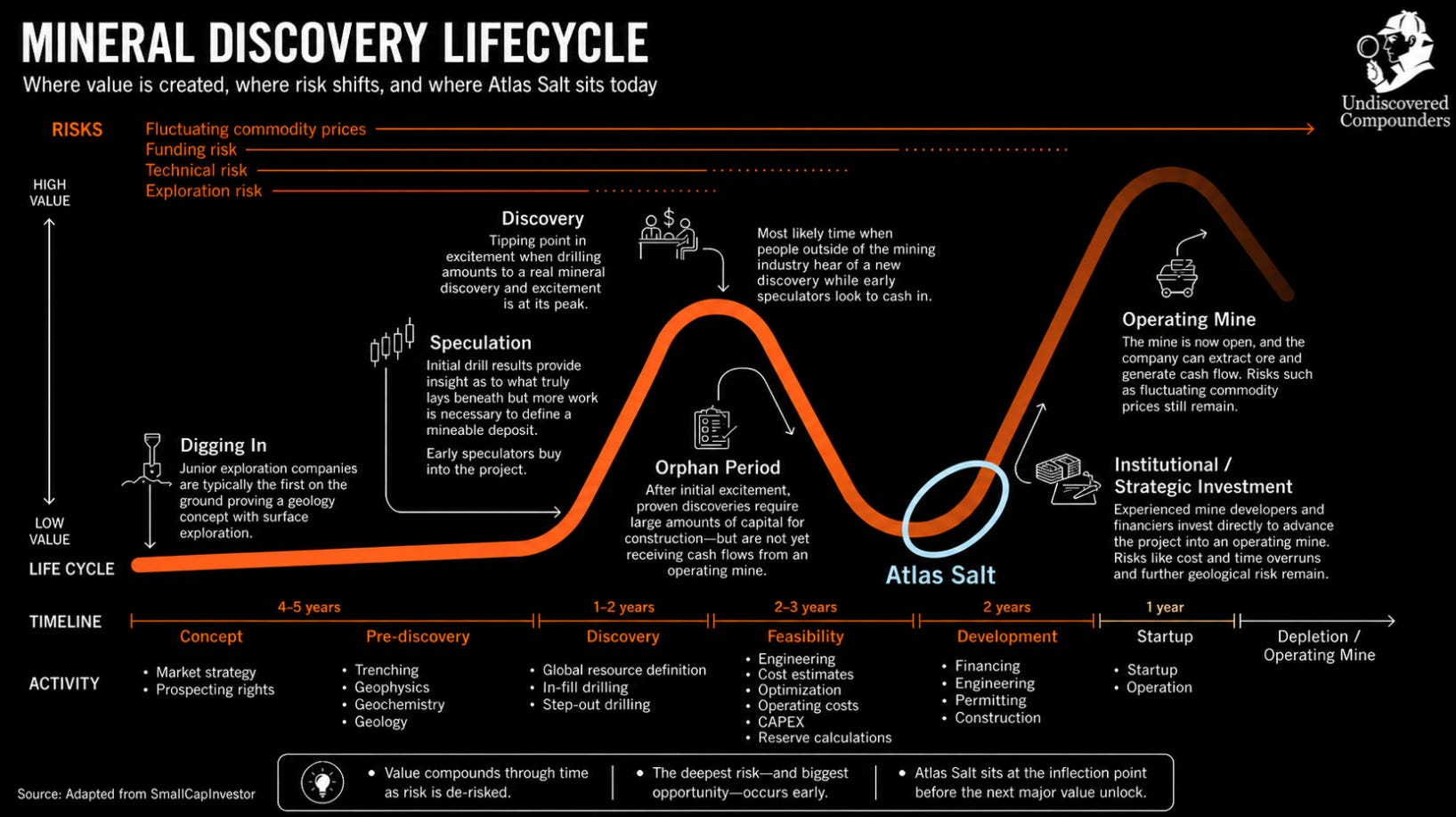

Atlas Salt is, for underwriting purposes, a single-project company. The asset is the Great Atlantic Salt deposit, in western Newfoundland and Labrador (Canada). Here’s why this is the first greenfield rock salt project in 25 years to clear every barrier that has kept new salt mines out of North America.

Methodological note: Unless otherwise footnoted, company-specific information comes from Atlas Salt’s recent public disclosures. Most of it is drawn from four documents: the Updated Feasibility Study, the 2025/2024 MD&A, the 2025/2024 annual financial statements, and the investor presentation.

The Deposit

Start with the rock itself. Atlas’s September 2025 Updated Feasibility Study (UFS; remember this acronym, because I’ll use it a lot) outlines a 24.25-year mine life based on 95.0 million tonnes of Probable Reserves grading 95.9% NaCl (sodium chloride, common salt). Those reserves sit inside a much larger resource envelope: 383 million tonnes of Indicated Mineral Resources at 96.0% NaCl, inclusive of the reserves, and 868 million tonnes of Inferred Mineral Resources at 95.2% NaCl. In plain English, the current mine plan uses 95 Mt, while approximately 288 Mt of additional Indicated Resources and all 868 Mt of Inferred Resources remain outside the reserve-case mine plan. All three categories exceed the 95% NaCl road-salt specification referenced in the UFS. The salt does not need beneficiation or chemical upgrading. Once crushed and screened to specification, it can be sold as road salt.

Mineral Reserves are the drilled, tested, and engineered part of the deposit, with enough confidence to support a bankable mine plan. Indicated Resources carry less confidence than reserves. Inferred Resources carry less confidence again.

The 24.25-year mine life in the UFS has to be understood on those terms. It is a planning horizon built on the Probable Reserve base. SLR, the firm that prepared the UFS, made that explicit: further drilling during production could convert additional material into reserves, and the expansion case extended mine life to 47.5 years, on partial reserve support and with no commitment that the plan would ever be executed.55 The UFS cannot capitalize those later tonnes in reserve-case cash flow today, while management has little economic reason to spend aggressively to prove year 50 before year one exists.

Bedded salt deposits like Great Atlantic tend to convert inferred resources to reserves at rates metal projects rarely match. The deposit is homogeneous, laterally continuous over kilometers, high purity, and grade appears not to vary meaningfully across the envelope. For a mining project, that is exactly the kind of geology you want: boring, repeatable, and hard to misread. Goderich, now Compass Minerals’ flagship mine, became the world’s largest underground salt mine from a remarkably thin original drilling base: 16 vertical core boreholes drilled in the 1950s, later validated by six decades of mining.56 Atlas has drilled forty-eight holes in a shallow, laterally continuous deposit.57

The UFS cannot price what is not yet a reserve. That’s the rule, and SLR follows it: Approximately 288 Mt of Indicated Resources beyond the reserve base, plus the 868 Mt of Inferred Resources, sit outside the reserve-case mine plan and the NPV. I’m not bound by that rule. I could assign part of that 1,156 Mt base a probability-weighted value, based on the geology and the historical track record of bedded salt deposits. I’m not going to. I’m leaving it as free upside. The 95 million tonnes of Probable Reserves are already enough for the thesis.

But there is more. Management’s view is that, once underground, the mine may be able to keep moving horizontally beyond the current reserve, then beyond the current resource, and eventually into undrilled ground. If true, this could translate into lower sustaining capital, lower development cost, and lower unit operating cost than the reserve-constrained UFS can model today. Think of the mine as a stack of levels. Opening a new level is more expensive than extending development horizontally within an existing one. So if Atlas can recover more tonnes than planned from the same level, the economics improve: the fixed development cost is spread over more salt. But again, the UFS cannot include that in the reserve-case economics today. And again, I leave it out, more for lack of data than out of excessive conservatism.

Transport Logistics as a Moat

Once purity and gradation specs are met, deicing rock salt is largely interchangeable. Geography, and the logistics that flow from it, are the moat. Atlas is built around that.

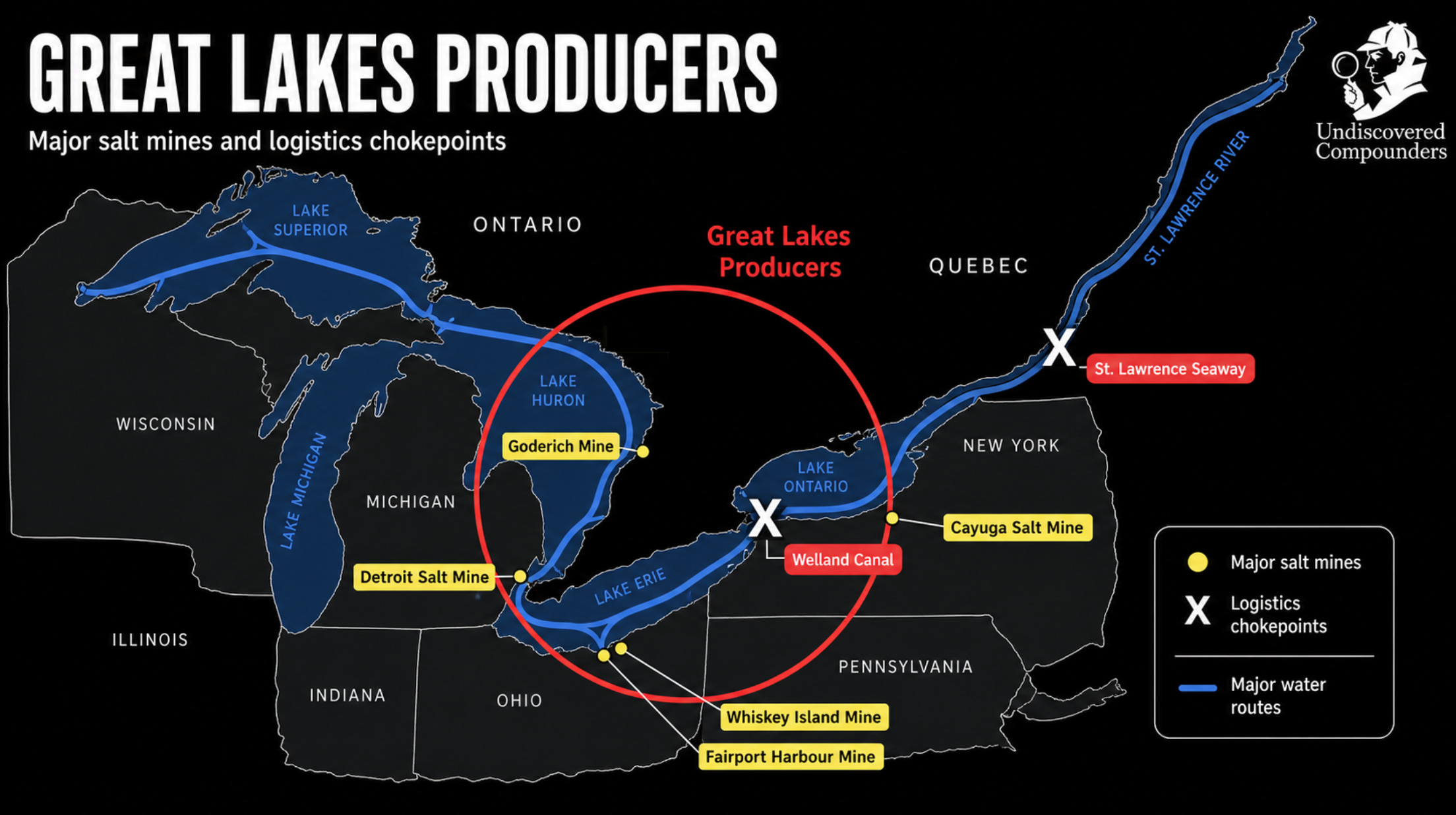

The project sits two kilometers from Turf Point, a deepwater port on the west coast of Newfoundland, with direct access to Atlantic shipping lanes. The design calls for a conveyor linking the mine directly to a ship-loading facility sized for Handysize and Handymax bulk carriers.58 No trucks, just a modest line item in initial CapEx and ongoing maintenance, and the mine-to-port leg is solved upfront. If built as planned, Great Atlantic would be able to serve Boston, New York, Philadelphia, or Baltimore within a 3‑ to 5‑day round trip, narrowing that gap between import lead time and emergency demand in a way Goderich, Cote Blanche, or Chilean and Egyptian salt simply cannot match on the same winter-response basis.

It gets worse inland. Cargill’s remaining U.S. mines and Compass Minerals’ Goderich rely on the St. Lawrence Seaway and the Welland Canal for waterborne access, which close every January and reopen in late March.59 That is exactly when a harsh winter tears through contracted tonnage: DOTs hit their contracted volume ceilings, private contractors run dry, and the spot market takes over. At that point, price is set by whatever tonne can actually reach the customer. Great Lakes producers go silent for ten weeks every winter, restricted to overland delivery within trucking range. Atlas could keep shipping.

The rest of the year, when the Seaway is open and everyone bids into the same public tenders, Atlas’s positioning should still win on distance to market. A short North Atlantic haul to Boston, New York and Philadelphia beats the Great Lakes detour from Goderich, and beats anything Chilean or Egyptian supply can put on a two-to-three-week ocean route. The geography pays in every season, but it also costs something.

Management has built Atlas’s logistics pitch around this advantage, describing Turf Point as “year-round with no seasonal ice closure.”60 That needs one clarification. Turf Point sits in St. George’s Bay, a sub-basin of the Gulf of St. Lawrence that the Canadian Coast Guard designates as Ice Zone Area 2, with a formal ice season running December 21 to April 15.61 This is not the same as being ice-free. However, the Gulf remains navigable through winter with icebreaker support, while the Seaway physically closes. Commercial vessels over 200 gross tonnage transiting an ice zone during the ice season pay a Canadian Coast Guard icebreaking fee. For the 2025-26 fee, that rate is C$3,818.61 per transit.62 Under plausible assumptions about vessel size, billing mechanics, and how much of Atlas’s shipment calendar falls inside the ice window, that translates into somewhere between C$0.03 and C$0.10 per tonne shipped in direct icebreaking fees.63 Against the UFS LOM operating cost of C$28.17/t, it is a rounding error.64

The logistics advantage is physical, but it is neither free nor fully built. Turf Point is an existing third-party-owned port, already operating as an aggregate export facility. Atlas also ships small amounts of gypsum from its Flat Bay mine through Turf Point.65 The existing trestle, ship loader, and caissons can already handle Handymax vessels. What Atlas plans at Turf Point is a brownfield expansion: a new 47,300-tonne storage building, refurbishment of the trestle and ship loader, reclaim conveyors, dredging, and one additional mooring caisson. The UFS puts the port line at C$58.5 million, about 10% of the C$589 million initial capital. That creates normal construction and logistics risk. A second risk, more upstream: no commercial agreement yet binds Atlas to Turf Point. That is normal at this stage. The port owner has strong reasons to sign, and failure to sign strikes me as very unlikely. But it remains the key binary item of the setup. I treat it in detail in the risks section.

The rest is already in place. The St. George’s substation sits 1.4 kilometers from the project, the Trans-Canada Highway runs alongside it, and a regional airport is within reach. Atlas essentially bolts a shallow, laterally continuous salt deposit onto road, power, and air infrastructure that someone else built decades ago.

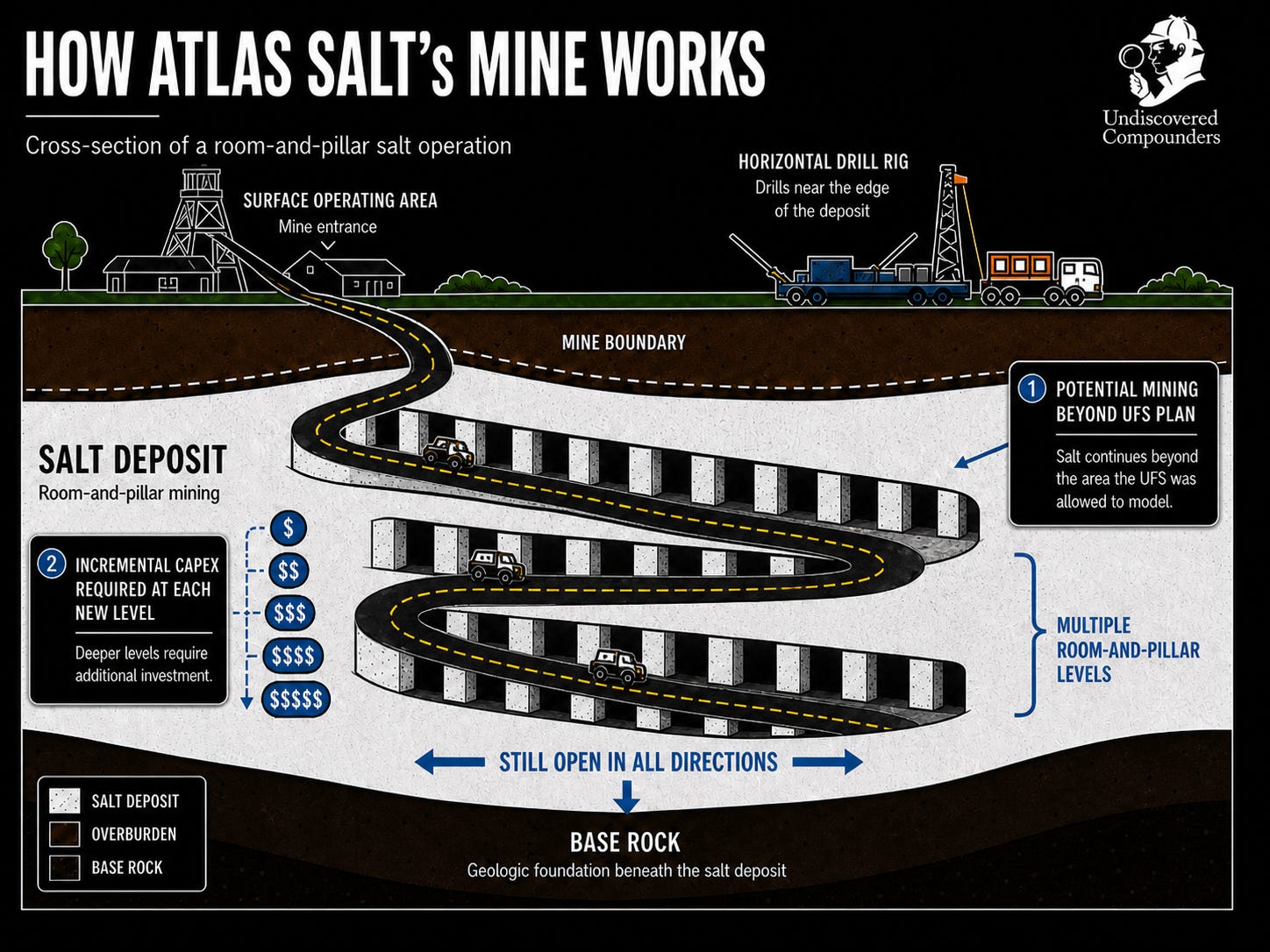

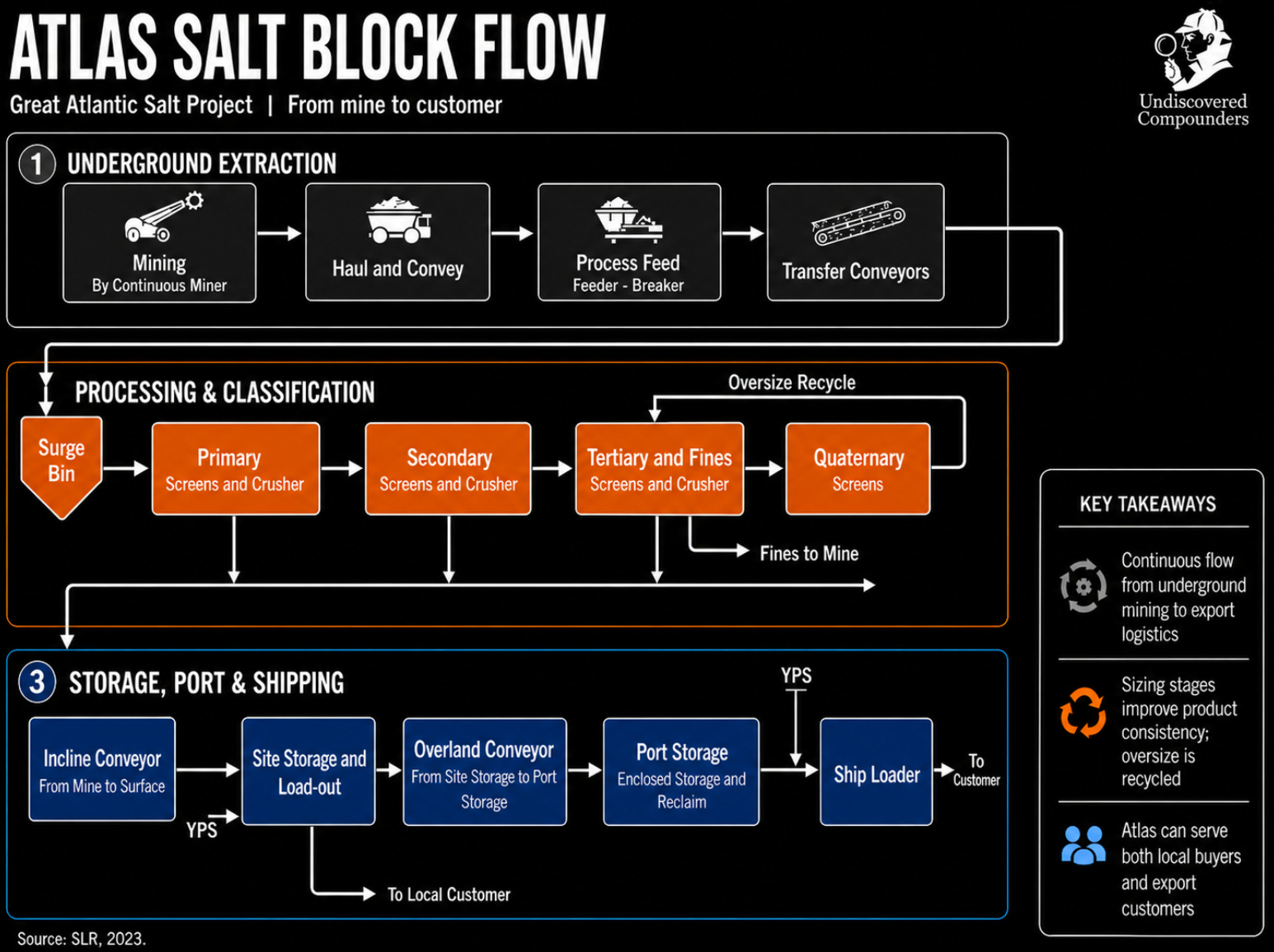

The Operational Design

Goderich’s mine sits at 550 meters. Cayuga’s, beyond 700 m. Great Atlantic’s is around 180 m. A third of the depth changes the entire economics of the project.

A deep mine needs a vertical shaft: a cage to lower crews, a hoist to lift ore in skips, several years of construction and several hundred million dollars before the first tonne reaches the surface. Atlas can skip that shaft-and-hoist architecture. At 180 meters, the gradient is gentle enough to drive declines that run from the surface down to the orebody. Trucks, conveyors, and personnel can move through ramps (and gravity) instead of relying on a vertical shaft.

The geometry pays a second time. Once underground, you attack the rock. The chosen method is room-and-pillar: you carve a grid of rooms into the salt, leaving pillars of salt untouched between them. The salt mostly holds itself up; that is the point of leaving pillars behind. The method works best on tabular, thick, homogeneous deposits, which is exactly what Great Atlantic is.

Then you have to break the rock. Most underground hard-rock operations still use drill-and-blast: drill holes, pack explosives, fire, clear debris, ventilate and repeat. Atlas chose a continuous miner, a machine that bites into the rock with a rotating head and drops it onto a haulage system. Salt is soft compared to granite or metallic ore, soft enough that mechanical cutting becomes the lower-cost option.

The rest of the flowsheet is deliberately short. An underground crusher and screens size the salt. A conveyor carries it up the declines. At surface, it passes through a 47,300-tonne storage building. From there, a second conveyor carries it the two kilometers to Turf Point, where a dedicated storage and conveyor-fed shiploading system would load vessels for export. But even simplicity carries risks, and the project’s risk profile gets its own section.

In video form (please forgive the music):

Because the design avoids drill-and-blast and uses an electric underground fleet, the ventilation load falls sharply. Great, because ventilation is one of the largest energy line items in a conventional mine. That allows Atlas to design the site as an electric-based operation: electric cutting equipment, battery-electric underground trucks and loaders, power drawn from Newfoundland’s hydroelectric grid. The ESG case wrote itself, and it happened to align with exactly what the province and the local communities wanted to see from a new mine.

The design is not being invented from scratch. Great Atlantic Salt draws heavily on Irish Salt Mining’s Kilroot mine: an underground soft-rock room-and-pillar mine, with an underground conveyor system, and product moved to port for shipment into the deicing market. Atlas’s senior engineers visited Kilroot, and the Great Atlantic study team included engineers with Kilroot experience, especially on ground support, underground conveyor structure, and drift access design. That does not remove execution risk, but it does show that similar mine architecture has worked before. It is also worth noting that Kilroot was developed in the 1960s.

A shallow deposit, a continuous extraction method, a five-step flowsheet, and a conveyor that ends in a ship’s hold. On paper, the operation is about as simple as a salt mine gets. But on the ground, simplicity tends to end where people begin.

The Social Component

A mining project also stands on its ability to clear permits, hold community support, and present a defensible environmental profile.

This part is not necessarily riveting, but it matters. For those who really do not feel like reading it, let me summarize: on these three fronts, Atlas is not only moving without friction but is actively supported by both local stakeholders and the provincial government.

For the rest of you, let’s dissect.

Permitting

Seven weeks. That’s the time it took Newfoundland and Labrador (NL) to release Atlas from its environmental assessment process, from filing to clearance. For mining projects, that is fast. Full environmental assessment processes can run 12 to 18 months, and full environmental-impact-statement cases can stretch over several years. Those seven weeks tell you at least three things. Two are obvious: the file was clean, and the regulator wanted it through. The third is less obvious, and we will get to it when we talk about who runs this company.

At the federal level, the IAAC (Impact Assessment Agency of Canada) confirmed in writing in December 2023 that the project is not subject to a federal impact assessment. Salt mines are not on the list of designated activities, and 4 Mtpa of production does not trigger a designated-project review. Two levels of government and two green lights.

Several approvals and project plans are already in place66: EA, Early Works Development Plan, Environmental Protection Plan, Waste Management, Water Resource Management, Wetland Conservation, Bat Preventative Measures, Gender/Diversity/Equity/Inclusion Plan, and Benefits Plan. What’s left belongs to the construction phase: a separate Capital Development EPP (Environmental Protection Plan), a Mill Licence before operation, and potentially a Fisheries Act Authorization for the in-water works at Turf Point (dredging and new caisson). That last one is the only potential bottleneck, with an up to 18-month process if triggered, but the four-year execution schedule has room for it (I contacted management on this point, and on several others, but as of today I have not received a response). Incentives are aligned across all parties, which makes it unlikely to become a problem.

Jurisdiction and community

NL ranks third among Canadian jurisdictions for mining investment in the Fraser Institute’s 2025 survey, and fourteenth globally. The regulatory framework is stable, the provincial government actively courts mining capital, and the region around the project has an unbroken mining tradition since the 1950s: gypsum for decades (still shipping today), and a limestone mine still operating. St. George’s is not a town meeting its first mining project.

Three stakeholders have formally voiced support: the Town of St. George’s, the Bay St. George’s Chamber of Commerce, and the First Nations Bands of St. George’s, Flat Bay, and Three Rivers. The Qalipu First Nation67 is still considering its support, but has raised no specific concerns. The project site already sits next to an active gypsum quarry, and Qalipu’s administrative base is approximately 70 km away. The probability of friction appears low.

Environmental profile

Credible ESG arguments are rare in mining, but Atlas ticks several boxes that make the defense unusually easy. The mine is designed to be an electric operation, powered by NL Hydro’s hydroelectricity at C$0.062/kWh. Projected Scope 1 emissions: 79 tonnes CO2 per year (approximately what four 4-person households in Newfoundland emit). No tailings, no chemical processing, and no diesel underground fleet. The project’s carbon footprint is a rounding error on a suburb. That helps explain why the environmental assessment approval was granted in less than two months, compared with approximately 1-1.5 years for other mining projects.

Sensitive-species on site? Only one issue has shown up in surveys so far. Bat acoustic monitoring picked up activity in July 2024, with follow-up results still pending. At this stage, that looks like routine procedural work, more likely a small cost line than a thesis risk. Black ash and raptor surveys turned up nothing. No known archaeological sites either.

Now the best “incentive” part: the projected economic return to the community is enormous: 170+ direct long-term jobs, nearly C$2.8 billion in tax revenue over the mine’s life, and active support for Memorial University’s critical minerals research. St. George’s is a rural community whose population declined 5.3% over five years and it is about to inherit a multi-generational employer.

Aligned incentives are rare in mining. It is one of the reasons even projects with exceptional numbers on paper, technically de-risked, stay undervalued for years. They die in the maze of permitting, opposing incentives, and community opposition. Atlas sits outside that maze. And yet it trades at a deeper discount than many projects stuck inside it.

04. The Business Model

Compass Minerals, one of the biggest deicing salt producers in North America, owns and controls: mines, packaging plants, distribution centers, brand names, storage depots, vessels, barges, rail and trucking relationships, and direct contractual relationships with virtually every DOT and public-sector buyer East of the Mississippi. Morton Salt and Cargill have built the same end-to-end machine. They mine the salt, screen it, bag it, brand it, ship it, and sell it directly to the entity that will spread it on a road. These are fully integrated supply chains built over 60 to 130 years.

Atlas controls a planned mine project that is expected to start production in 2030.68

This section is an analysis of what that gap means.

One clarification upfront. As of the date of this report, Atlas has not signed a single binding commercial contract with any relevant counterparty. The key commercial relationships disclosed by management so far are non-binding MOUs (Memoranda of Understanding). Early works are underway on site, but remaining construction-phase permits, project debt, and equity gap funding are still ahead. First production is at least four years away under the schedule disclosed by management. This contractual posture is the normal state for a junior developer at this stage, and it is the starting point from which the rest of this section should be read.

The Product: One Feedstock, Several Commercial Formats

Atlas plans to sell essentially one feedstock: crushed rock salt for road deicing. The same raw material comes off the crusher, then gets separated into different specifications and formats depending on the sales channel, but not in equal proportions. Within the bulk road-salt segment, the UFS distinguishes two commercial specifications coming off the same crusher. Public road-salt tenders typically require the ASTM D632-12 standard.69 Commercial products sold through distributors demand tighter “Screened Mediums” specifications: the same 95% NaCl minimum, but lower moisture, narrower gradation, and fewer fines.70 The two streams would be separated at the processing plant: Atlas produces one product and screens it into commercial grades depending on which sales channel it feeds.

A smaller share could go to packaged consumer salt, sold through branded partners such as Scotwood Industries, the segment where Atlas could capture a meaningful piece of the approximately 6x markup that exists between bulk producer pricing and retail shelf pricing. A marginal residual goes to colored salt for specialty markets, irrelevant to this analysis and not contractually committed in any case.71

Where Atlas Plans to Sell

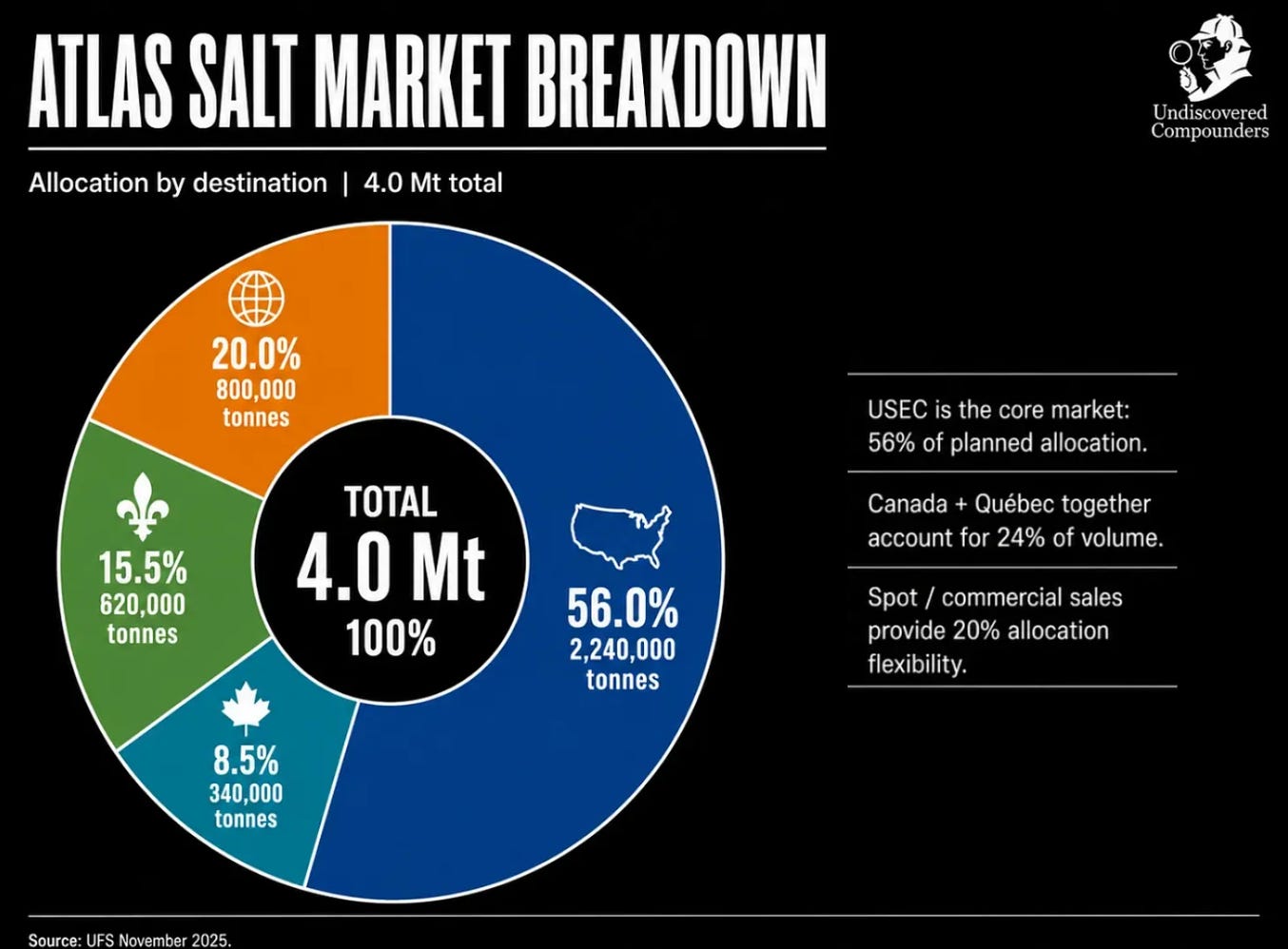

The planned 4.0 Mtpa production splits across four geographic destinations, each with its own logistics profile and pricing dynamics.

The U.S. East Coast represents 56% of planned volume and the bulk of the C$920M NPV. The UFS defines this market as ports along the U.S. East Coast from Maine down to Baltimore, plus inland states reaching as far west as Pennsylvania and West Virginia. This is the region where the 8-10 Mtpa structural import gap concentrates, and where Cargill’s permanent closure of Avery Island in 2022 removed another 2.5 Mtpa of domestic supply from the market. Realistically, 1.5 to 2.5 Mtpa could land somewhere along this coast, displacing the highest delivered-cost suppliers first: Chilean and Egyptian salt with multi-week ocean lead times, but also North American mines whose distance from the East Coast forces freight costs that Atlas’s geographic position simply does not carry.

Québec, at 15.5%, is the defensive line. The St. Lawrence corridor consumes an estimated 3.5 to 5 Mtpa every year, and for ten weeks each winter, Atlas would be one of the few nearby producers with waterborne access into the region while the Seaway is closed. As noted, the 15.5% allocation is not committed. But no new commercial infrastructure is needed to capture it: the corridor is already there, the buyers are already there, and the geography does the rest.

The Maritimes (Nova Scotia, New Brunswick, and Prince Edward Island) at 8.5%, is a smaller target, and a relatively standard one. Atlas would sell salt dockside at ports like Halifax or Saint John, and a local distribution company would handle unloading, storage, and delivery to the final customer. For those provinces, Atlas would become a nearby, reliable source they can tap in volume and during the season. For Atlas, it is a minor share of output with above-average margins. Geography, yet again, tilts the economics.

The 20% allocated to Spot Sales and Commercial is the most economically interesting line in the mix. It captures three distinct flows. First, emergency purchases by municipalities when their contracts run short (the Ontario 2026 dynamic, with spot prices at C$300/tonne). Second, ongoing sales through commercial distributors to private snow contractors, who get pushed to the back of the queue every time municipal demand spikes and end up paying multiples of normal bulk pricing. Third, the local Newfoundland market itself, approximately 0.3-0.35 Mtpa with no internal production, served by truck and short-haul vessel shipments directly to municipalities along the west coast. All three flows pay above tender pricing. And all three favour the producer who can ship year-round.

I’ll say it again: this is a planning allocation by design, and a deliberately conservative one. Atlas appears to want a larger spot-market allocation than the UFS assumes. As a shareholder, I would welcome that (more on that later).

How It Actually Sells: CIF, DAP, FOB

There are three commercial structures, depending on the destination. Each transfers risk and captures margin differently.

CIF (Cost, Insurance, Freight) is the standard structure for the bulk of U.S. East Coast shipments. Atlas would arrange and pay for ocean freight and insurance to the destination port, where a local distribution company manages unloading, storage, trucking to the salt depot, and final sale to the road-spreading entity. Atlas would carry the freight-cost exposure; the distributor would carry everything downstream. This is the dominant structure for the 56% U.S. East Coast allocation.

DAP (Delivered at Place) applies to the western Newfoundland market. Atlas would deliver all the way to the customer (typically a municipality) by truck or short-haul vessel depending on distance. Atlas would control the entire chain to final delivery, but the addressable market is small. Management has not named carriers or routes, but the economics point to contracted trucking rather than an owned fleet (at least in the early production years). At 0.3-0.35 Mtpa, the volume does not justify dedicated vehicle CapEx.

FOB (Free on Board) applies to buyers who arrange their own vessel at Turf Point and take title once the cargo is loaded. Atlas’s risk ends once the salt is loaded aboard the vessel. This is the simplest structure for Atlas operationally, but it can limit pricing power: the buyer’s negotiating leverage is highest when they control the vessel.

I hope you’ve been following closely, because this is where it gets important. Section 19.4.2 of the UFS:

“Regardless of the shipping terms (DAP, FOB, CIF), the pricing assumed by SLR in the financial model is FOB Turf Point Port.”

The entire C$920M NPV runs on a uniform C$81.67 per tonne price on an FOB Turf Point basis, regardless of the commercial shipping terms. The assumption is simple and elegant. If anything goes wrong in the long-distance deicing salt chain (and plenty can), Atlas’s 2 km-to-port geography becomes structurally more valuable than the model assumes. Imported Chilean and Egyptian supply loses competitiveness first. Atlas keeps its relative position intact. The FOB-equivalent pricing assumption is therefore potentially a source of additional margin. Like the 288 Mt of additional Indicated Resources and 868 Mt of Inferred Resources earlier, I’m treating it as free upside. The setup still does not need it.

The Contracts

Section 19.5 of the NI 43-101 technical report captures the current situation perfectly:

“Atlas has had preliminary discussions with potential salt purchasers as well as salt brokers. Similarly, the Company has had preliminary discussions with logistics companies and port operators that would be involved in the process of delivering salt to destination markets. As of the effective date of the UFS, Atlas has not entered into any binding commercial contracts with respect to salt marketing or logistics.”

Nothing abnormal here. Early works on the mine have begun, production is at least four years away, and counterparties rarely commit to binding contracts that far ahead of execution. Atlas has already announced four non-binding MOUs (Memoranda of Understanding; statements of intent) with tier-one counterparties.

MOUs serve two purposes, depending on the counterparty: they can reduce the capital Atlas has to raise upfront, and they tell future lenders that a tier-one counterparty has already diligenced the file and stayed at the table. Take Sandvik. If that equipment MOU converts to binding vendor financing, Atlas could pay for the fleet out of post-production cash flow, not out of equity raised today at a depressed valuation. Each MOU has its own specifics, but the logic is the same: less potential dilution now and/or easier financing later.

Atlas currently has four such MOUs with major counterparties. Each is non-binding, but each is a potential milestone. Especially the first one.

Scotwood Industries, Commercial Offtake + Canadian JV (August 20, 2024)

Atlas signed the MOU thirteen months before the UFS was published. It bundles two things into one deal. First, a proposed strategic offtake: Atlas would supply bulk salt to the partnership. Second, a 50/50 joint venture: the JV packages that salt, brands it, and sells it into the Canadian retail market. A combined target of 1.25 to 1.5 Mtpa, with profits split equally after each side recovers its costs. The deal explicitly excludes bulk road deicing salt (the public-tender channel) and excludes the four Atlantic provinces (the market Atlas can reach on its own). With one important exception: Scotwood’s national Canadian retail accounts (think Walmart Canada, Home Depot Canada) can be supplied anywhere in the country, including the excluded provinces. Remember, this is the channel where the same salt can sell for several times the bulk price.

Why this matters.

Scotwood is the largest packaged retail deicing distributor in the United States: Home Depot, Walmart, big-box mass merchandisers, DIY chains, farm and home retailers, grocery chains, and others. When a distributor that size signs even a non-binding MOU with a junior pre-production developer, the file has passed a filter. Chase Wilson, Scotwood’s President, said so at signing:

“Being the largest distributor of packaged retail deicing salt in the United States we are very selective in choosing new business partners. If completed, we believe Atlas Salt’s long life underground salt project would make Atlas Salt an ideal long-term partner for us in Canada.”

Rick LaBelle, then CEO of Atlas Salt, was equally explicit about Atlas’s side of the logic:

“Since I joined the Company, I’ve been focused on opportunities in the retail market, where supply is more predictable, and margins are generally higher.”

This is where the UFS NPV stops being the full picture.

Every tonne in the C$920M NPV starts from a C$81.67 per tonne base price on an FOB Turf Point basis. SLR chose a single blended price across every destination and every product format, effectively anchored on bulk deicing economics (the lowest-margin channel in the deicing market). Walk into a Home Depot today and look at the shelf: a tonne of packaged deicing salt retails around C$500-600. The UFS prices essentially none of this differential.

Most of that retail spread won’t flow back to Atlas: retailer margin, distribution costs, packaging, and the 50/50 JV split with Scotwood all take their cut. What lands on Atlas’s income statement after those steps could be somewhere between C$60 and C$80 /t above the bulk base case (estimate),72 depending on cost structure and negotiation. At 1.5 Mtpa through Scotwood, that’s C$90 to C$120 million of incremental annual pre-tax contribution attributable to Atlas not captured in the NPV. Discounted at 8%, with no salt-price escalation, over the 24-year mine life, the C$60-80/t uplift on 1.5 Mtpa would imply approximately C$945 million to C$1.26 billion of pre-tax present value.

After taxes and leakage, the incremental present value would land closer to C$630 million to C$840 million.

Let me reframe this. With up to 37.5% of annual production routed through packaged/retail-related channels, the incremental value alone could approach the entire NPV built on bulk pricing. Recalculating the NPV with 37.5% flowing through the packaged/retail-related channel (the high end of what the MOU contemplates) would lift project value by 68% to 91%. Cut that estimate in half as a safety margin and the uplift still lands between 34% and 45%. Just from Atlas selling its salt in bags through a partnership. Back-of-envelope, but the direction is unambiguous. And the company trades at a P/NPV of approximately 0.13x against a project NPV that does not count any of it.

That was the picture at 1.25-1.5 Mtpa. Then the project scaled.

The 2023 Feasibility Study modeled 2.5 Mtpa. The 2025 UFS modeled 4.0 Mtpa. Yet the Scotwood target volume did not move. Yet. Nolan Peterson, who took over from LaBelle in June 2025, addressed this directly:

“For Scotwood, that tonnage was set in the original feasibility study, remember when the project was much smaller. So there is the opportunity to expand that offtake to encompass the larger project production, and we are in discussions with Scotwood and other offtake partners about taking the remainder.”

Management has begun the conversation to expand that offtake, and Peterson’s phrasing (“Scotwood and other offtake partners”) telegraphs that the search has widened. If the binding arrangement eventually routes closer to 50% of nameplate through higher-margin packaged/retail-related channels, the economics per tonne attributable to Atlas could reshape the project entirely.

Peterson added one more line worth hearing:

“It does not mean that we need a partnership like this. We can always develop those relationships ourselves and market the salt ourselves, but it’s very helpful. It’s one less thing for us as miners that are familiar with mining and developing projects that we have to worry about.”

The CEO makes the point explicit: the MOU is not on the critical path. Atlas can walk away from it if the terms do not evolve in its favor. But the shortcut is worth taking, in my opinion, even on less favorable terms. Replicating Scotwood’s retail chain would take Atlas years and a lot of capital, starting after first production, with management bandwidth it does not have today and won’t have at the start of production. Owning the full margin sounds better on a slide, but getting half of it, years earlier, without the CapEx, is probably the better trade. At least through the first debt-repayment window, until cash flow stabilizes. In any case, senior lenders would probably reject a go-it-alone retail buildout. When project lenders underwrite a project, they do it against a specific base case, and they are usually reluctant to accept deviations, especially ones that introduce that much commercial risk.

The NPV holds up fine if Scotwood goes nowhere. The stock could reprice materially if it does. That’s the kind of asymmetry a shareholder wants to own. It shows up, to a smaller degree, in the three MOUs that follow.

Sandvik Mining, Equipment + Vendor Financing (September 2024, expanded February 13, 2026)

The Sandvik MOU, expanded in February 2026, is also the kind of thing we want to see as shareholders. The expanded scope raised the total estimated commercial value from C$73 million to up to approximately C$132 million, covering both initial construction and the multi-year ramp-up to 4.0 Mtpa. Sandvik would supply underground mobile mining equipment, technology, and associated services.73 Sandvik is also Atlas’s Integrated Project Delivery (IPD) partner, which means it would be embedded in the mine design, automation planning, and long-term maintenance architecture from the start.

The financing piece is critical (and easy to misread). It contemplates vendor-supported financing for Sandvik capital equipment within the C$132M commercial scope, potentially less than the full amount, subject to “customary due diligence, receipt of Sandvik’s required internal approvals, and negotiation and execution of the definitive agreements.” It is an expression of intent from a tier-one global equipment supplier that, if converted, could materially reduce Atlas’s upfront cash equipment outlay. If not, Atlas would need to find another partner, or fund the equipment from project debt or equity. We come back to this in the financing section.

Hatch Ltd., Lead Engineering & IPD Partner (November 12, 2025)

Hatch is one of the world’s largest engineering firms (10,000 staff, 150+ countries, over seven decades of engineering experience and a track record in underground soft-rock mines), with an established Newfoundland and Labrador presence. The MOU establishes Hatch as Lead Engineering Partner and IPD Partner. In plain English: Hatch would integrate all engineering disciplines under a single delivery framework, from detailed design through construction support.

The value of the Hatch relationship to Atlas is reputational as much as technical. A tier-one engineering firm putting its name on the project would signal to lenders and equity investors that the technical foundation is being built to institutional standards. For a junior developer with limited internal engineering depth, this matters.

Continental Conveyor, Material Handling, IPD Partner (October 29, 2025)

This is the most operationally specific of the four. Continental would design and supply the complete material handling conveyor package: 28 belt conveyors and head chutes spanning underground crushing, surface storage, the 2-kilometer overland conveyor to Turf Point, and the port loading systems. The equipment would be supported by Continental’s Canadian facilities in Thetford Mines, Quebec, and Napanee, Ontario.

The conveyor system is a critical-path item for the project (without it, neither the mine-to-surface flow nor the surface-to-port flow exists), so lining up a credible Canadian supplier early is operationally sensible.

The four MOUs are straightforward:

Scotwood Industries: Packaged retail offtake + 50/50 Canadian JV. 1.25-1.5 Mtpa. No vendor financing.

Sandvik Mining: Underground mobile mining equipment, technology, and services (commercial scope up to C$132M). Vendor financing contemplated.

Hatch Ltd.: Lead Engineering Partner and IPD Partner. No vendor financing.

Continental Conveyor: 28 belt conveyors, mine-to-port. No vendor financing disclosed.