The Science of Not Giving a F*ck About Drawdowns

3 flaws, 4 patches, backed by science.

I don't like drawdowns, you don't like drawdowns, your neighbor doesn't like drawdowns, and his dog doesn't either.

Too bad for us, they’re a constant. Even with perfect foresight, you'd still face 76%. The only variable left is you.

You open your broker app, your portfolio is down too many percent. Red pixels bombard your retinas, your finger hovers over the sell button and… calm down.

Because our good old friend Science is already on it. She named our flaws one by one, and handed us the patches.

From Red Pixels to Capital Loss

Evolution has had exactly one goal for the last few million years: to get us through the next few seconds, over and over, until we reproduce.1

But when you apply tools custom-built for the next few seconds to decade-long objectives like investing, the damage is inevitable.

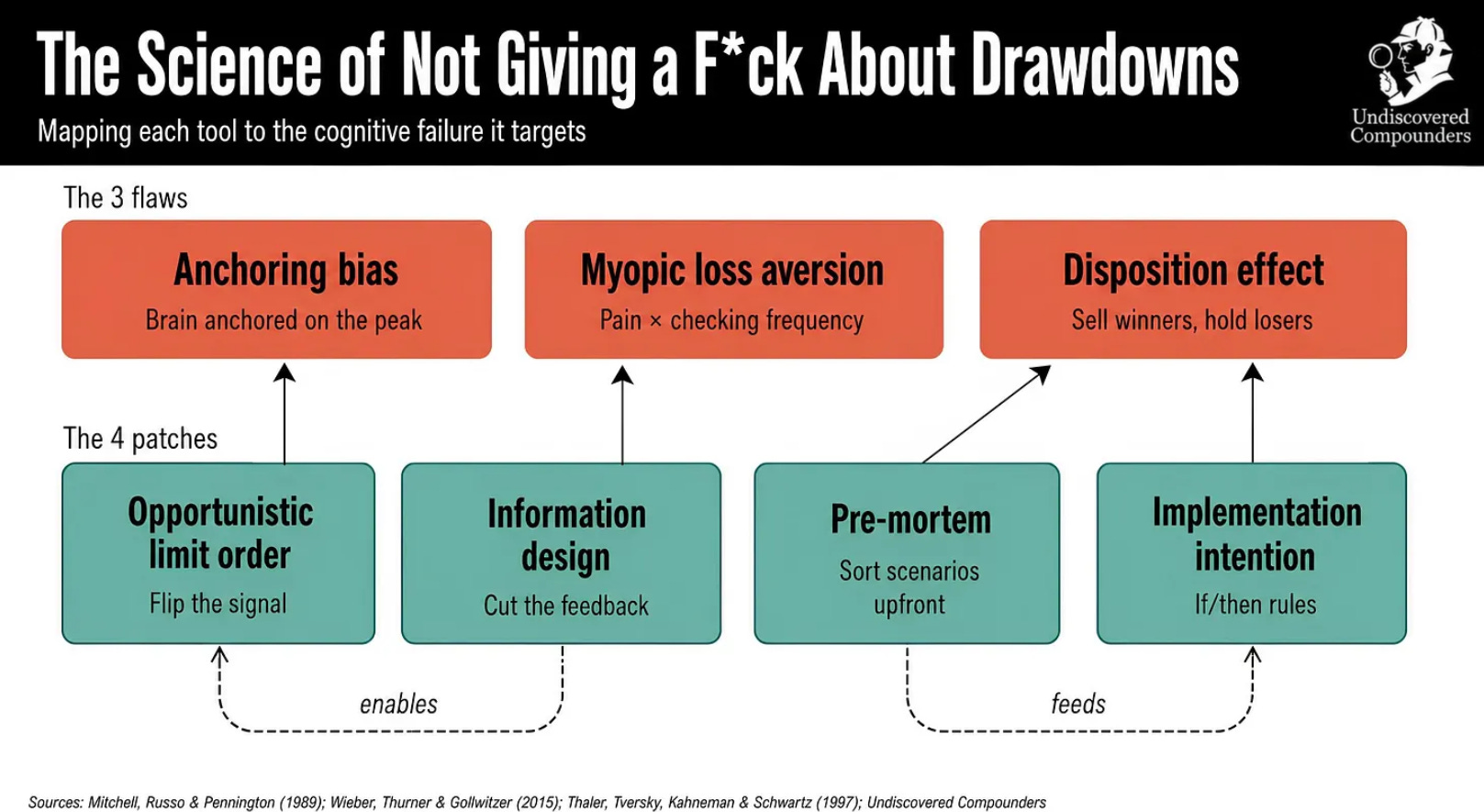

There are three culprits. Or rather, two accomplices and one executioner.

Accomplice #1

It’s just an accomplice, but an accomplice in almost every crime linked to bad decisions.

You’re bound to know it, you experience it dozens of times a day. The aptly named: anchoring bias.

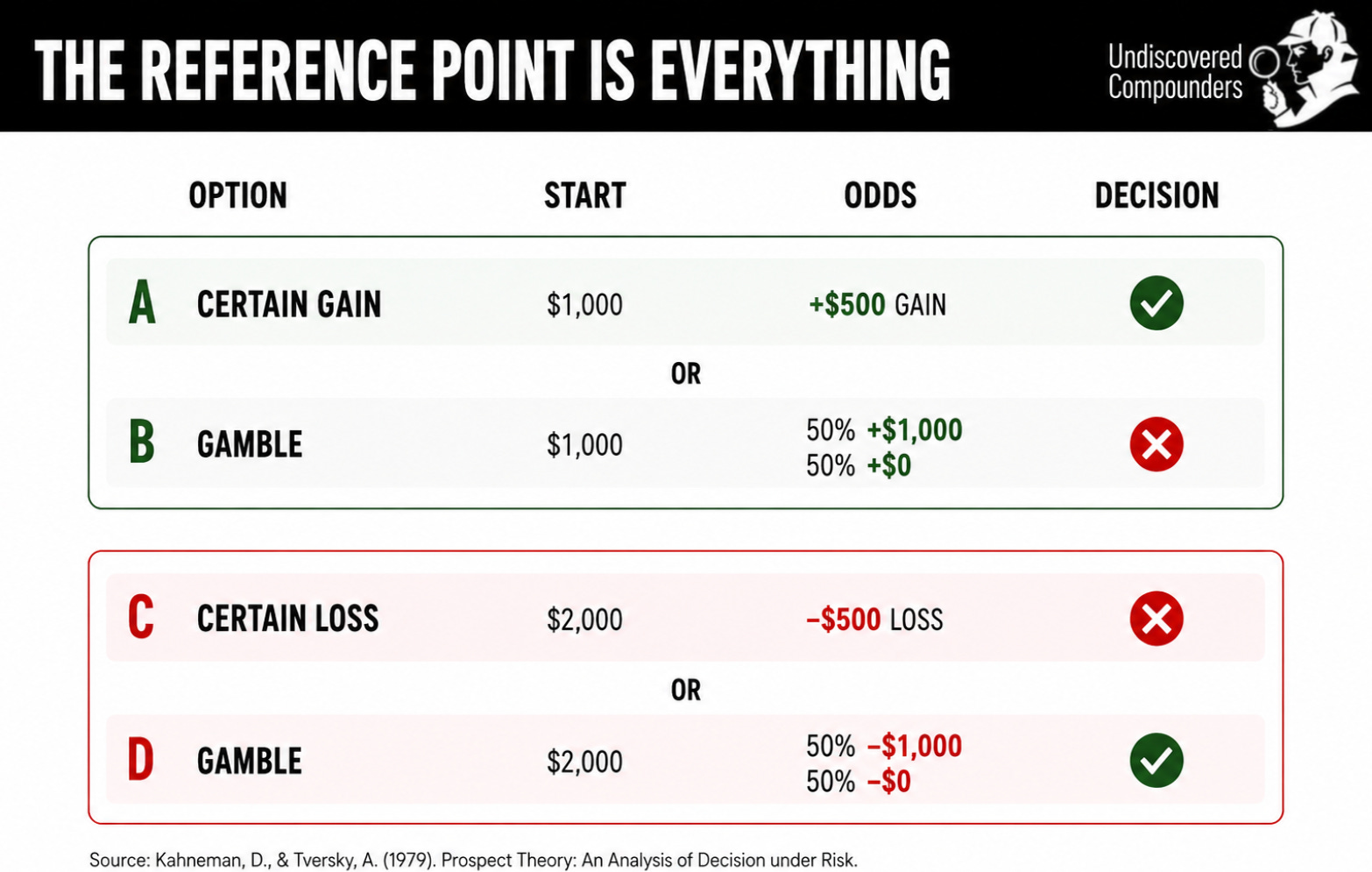

What your brain records is a deviation from a reference point, never an absolute price.2 And with every new high, that reference point resets.

Here is the experiment through which Kahneman & Tversky established it in Prospect Theory (the work that destroyed the homo economicus hypothesis, no less).

They showed that perceiving a situation as a loss feels psychologically twice as painful as perceiving it as a gain, even when the expected value is the same: $1,500 in every case.3

“That’s just psychology students making bad decisions. I’m an investor. Being rational is literally my job.” Okay.

You buy a stock. At random, Atlas Salt. You buy it at $1, it goes to $2. Great, you made a 2x. But you’re a long-term investor (or greedy, your call), so you don’t sell. The stock falls back to $1. So what, you’re flat, right? You sure? Not a single part of you would say: damn, I could have sold at 2x?

Of course you would. This dependence on the reference point is coded into our genes. This simple mechanism is probably responsible for trillions in losses over the years. (I have no proof, it’s just a deep conviction.)

In everyday life, it tends to fly solo. But in investing, it has a very close friend. And that’s our second accomplice.

Accomplice #2

Its name is myopic loss aversion.

If the first one creates the pain, this one multiplies it.

Loss aversion is our natural tendency to suffer more from a loss of X than to enjoy a gain of X (another gift from Kahneman & Tversky, they earned that Nobel Prize).

The myopic part emerges when evaluation frequency gets too high. The effect plays out in two steps: the more you check, the more frequently the reference point shifts, the more the pain multiplies.

With markets trading continuously for 6+ hours a day, five days a week, the myopic part has everything it needs to thrive.

Take a negative annual return of -30% and show it to two groups.

Low Frequency group (LF): sees the performance once a year.

High Frequency group (HF): sees it once a month.

Both groups are subject to loss aversion (they’re all human). The only variable is frequency, and therefore the impact of myopia. Result: the LF group was willing to invest 69.6% in stocks vs 40.9% for the HF group. A risk aversion almost twice as high, just from seeing the same -30% more frequently.4

And that was the beginner version of the experiment. In reality, investors can check their portfolio multiple times a day, and more importantly, they can buy or sell. That’s where the real culprit steps in.

The Culprit

The executioner finally takes the stage. Its name: the disposition effect.

No need for imaginary skeptical investors here. It has been documented across tens of thousands of real investors, from the beginner who barely knows where to click to the institutional manager running a billion-dollar portfolio.

The deeper investors were in drawdown, the more they acted, and those actions concentrated on keeping or buying more losers and selling winners to compensate.5

If you have any doubt about the quality of that strategy, let me remove it: it is the worst of all. I simulated millions of portfolios to analyze the evolution of opportunity cost, and it is by far the worst strategy. As for the best one, you’ll find the full post here.

One last finding. You have to appreciate the irony: selling randomly would have outperformed their actual sell decisions. A finding that also came up in my own simulation.

Investors spend hundreds, sometimes thousands, of hours a year analyzing companies, and yet a random strategy would have outperformed them on average.6

But it is what it is. Losers tend to keep losing, and winners tend to keep winning.

Between 3 and 4% of annual returns evaporated (or rather, transferred) because of the disposition effect.

The anchoring bias and myopic loss aversion are the two sidekicks pushing toward violence, but it is the disposition effect that pulls the trigger.

Less trivially:

Anchoring bias: We observe prices and performance from a reference point that shifts with every new comparison.

Myopic loss aversion: The more we compare, the more any given move carries a disproportionate impact.

The disposition effect: The deeper the drawdown, the more we tend toward the most value-destructive behaviors.

Diagnosis complete. On to the cure.

The Patches

It’s psychology, there’s no magic trick on its own. Just a few tricks that become magic with a good dose of discipline.

Patch #1

Let’s start with Kahneman’s own favorite method, “invented” by Gary Klein: the pre-mortem.7

Before a buy, you assume you will eventually sell, with certainty. Then you list as many scenarios as possible and sort them into two piles:

The broken thesis pile

The noise pile

As soon as a scenario unfolds, you check, and based on which pile it’s in, you sell or you hold.

What, sounds too basic? So what? Human psychology tends to be too.

Two groups of participants are asked to imagine causes for a future event (e.g., why would I sell?), with only one change in the prompt:

Group 1: the event might happen.

Group 2: the event will happen, with certainty.

Just by changing the framing from a possible event to a certain event, Group 2 generated 30% more reasons.8

The trick is simple and effective. But it’s clearly not enough.

Patch #2

It’s my second favorite patch.

People are asked to manage a random project with an allocated budget. Everyone goes through 3 phases: positive feedback, then mixed, then downright negative. The idea: build their confidence, then discourage them, to see how far they’ll take the investment project.

Small twist that changes everything, the base instruction varies (again):

Group 1: “We want to judge the project as neutral observers, regardless of past decisions.”

Group 2: “If we are about to make an investment decision, then we will judge the project as neutral observers, regardless of past decisions.”

Group 1 sinks into escalation of commitment despite the negative feedback. Only Group 2 escapes it.9

Yet the only thing that changes is the wording, from vague goal to if + then. And that’s the entire power of implementation intention.

By placing the environment inside a specific "if" and tying it to a precise action through "then", you close the door on dozens of cognitive biases.

It’s prompt engineering, but for biological intelligence.

Patch #3

Myopic loss aversion comes from feedback frequency. So if a cause leads to a negative consequence, just remove the cause.

That’s exactly the advice from Benartzi & Thaler (from accomplice #2): focus on information design. Build an information system where feedback access is limited.

It can be many things: deleting apps with live price quotes, logging off once you’re done, etc.

But this only goes so far. The financial industry is literally designed to bury us in information and noisy feedback.

This is where the final patch comes in.

Patch #4

No study here, it’s a personal (and my favorite) trick backed by my experience and nothing else. But it works incredibly well (at least on me).

The 3 previous solutions share one goal: reduce feedback frequency and its impact on our decisions.

Here, the idea is to flip the feedback’s signal: negative becomes positive.

When I’m building a position, I always leave 5 to 15% of my target final position as a limit order at an absurdly low price.

So every time the price drops, the message shifts: from “I’m losing more money” to “I might get to buy this company at an absurd price.”

Of course, you have to have done the work and have confidence in your thesis. Nothing’s free in investing.

But combine this trick with the previous three, and the drawdown is no longer a danger signal, but rather a boring opportunity you saw coming, or noise until something ticks a box on your thesis-breaker list.

Here's the full list of tricks to put in place:

Pre-mortem: Assume you’ll sell with certainty, and sort as many facts as you can into two piles: noise vs broken thesis.

Implementation intention: When building those piles, write each intention explicitly as if + then.

Information design: Minimize feedback exposure to defuse the myopic loss aversion effect.

Opportunistic limit order: Leave a few limit orders sitting at extremely low prices to flip the drawdown signal from loss to opportunity.

And here's how the system works:

There’s bound to be someone in your contacts who needs this. Be the friend who shares it.

Et voilà, the science of not giving a f*ck about drawdowns.

Some would say the ultimate patch against bad decisions during a drawdown is experience. I think that gets it backwards.

Experience is the accumulation of data. Wisdom is the ability to extract useful rules from it.

Of course, don't be dumb and learn from your mistakes. But more than that, be smart and learn from others’.

Our good old friend Science is just the most efficient and standardized method to do exactly that.

To keep learning and improving as an investor through science:

One quick last thing: thanks a lot for your feedback on my first two investing theses published in this newsletter. All your messages and comments made the work worth it.

You can find them here.

More coming very soon.

Right back to it.

Take care,

Flo

Calm down, biology nerds. I know natural selection has no goal and reading one into it after the fact is just a huge survivorship bias. But I just like to personify concepts, leave me alone.

I chose a price, but it could be anything that runs through a perceptual system: a smell, a sound, a temperature, etc.

Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263-292.

Tversky & Kahneman (1992). "Advances in Prospect Theory: Cumulative Representation of Uncertainty", Journal of Risk and Uncertainty.

Benartzi, S., & Thaler, R. H. (1999). Risk aversion or myopia? Choices in repeated gambles and retirement investments. Management Science, 45(3), 364-381.

Thaler, R. H., Tversky, A., Kahneman, D., & Schwartz, A. (1997). The effect of myopia and loss aversion on risk taking: An experimental test. The Quarterly Journal of Economics, 112(2), 647-661.

Odean, T. (1998). Are Investors Reluctant to Realize Their Losses? The Journal of Finance, 53(5), 1775-1798.

An, L., Engelberg, J., Henriksson, M., Wang, B., & Williams, J. (2024). The Portfolio-Driven Disposition Effect. Journal of Finance, 79(5), 3459-3495.

Strahilevitz, M. A., Odean, T., & Barber, B. M. (2011). Once Burned, Twice Shy: How Naive Learning, Counterfactuals, and Regret Affect the Repurchase of Stocks Previously Sold. Journal of Marketing Research, 48(SPL), S102-S120.

Barber, B. M., & Odean, T. (2000). Trading Is Hazardous to Your Wealth: The Common Stock Investment Performance of Individual Investors. Journal of Finance, 55(2), 773-806.

Klein, G. (2007). Performing a project premortem. Harvard Business Review, 85(9), 18–19.

Mitchell, D. J., Russo, J. E., & Pennington, N. (1989). Back to the future: Temporal perspective in the explanation of events. Journal of Behavioral Decision Making, 2(1), 25-38.

Wieber, F., Thürmer, J. L., & Gollwitzer, P. M. (2015). Attenuating the escalation of commitment to a faltering project in decision-making groups: An implementation intention approach. Social Psychological and Personality Science, 6(5), 587-595.

This is exactly how the evolution of long term investing morphs into the "I Don't Give a Flying F*ck About Drawdowns", especially after living through the 1999 dot com bubble, 2008 Global Financial Crisis, post 2020 SARS-Cov-2 recession and small 20% dips in between caused by Wall Streets noise of the day.

Preparation begins long before I buy a stock. It starts with thoughtful selection, understanding why a company deserves a place in the portfolio and having an exit plan before the first dollar is ever invested. Whether it's a short-term swing trade or a long-term retirement holding, every position should have both a Plan A and a Plan B. That's institutional level thinking.

Contrast that with my short-term trading and broader retirement portfolios, while they may use different tactics, they share the same foundation of disciplined selection, defined risk and the willingness to let preparation drive my decision-making process. The greatest is of these, IMHO, is pre-defining risk.

Thanks. A great deep dive into my psychology...LOL. Who knew me better than me? Apparently now Substack does too.

One method that a resource investor I follow is that once an investment reaches a double they mentally put a stop loss on the price based on the recent volatility of the stock price. If the price drops below the % determined by the volatility and after it has already doubled they determine whether to take their initial investment off the table or to sell all based on the fundamentals of the company or market (commodity) prices. In this way they let they can let their remaining investment compound or not “risk free”.