A world that stopped talking, and the portfolio I'm building for it.

1 thesis, 3 sectors, 9 companies, and why.

“If you want to be happy, be.” - Aleksei Tolstoï

A soft note to open, because from here on, it’s blood, sweat and tears.

I’m starting from one observation: the geopolitics of diplomacy is giving way to the geopolitics of conflict. Decades-long tensions are crystallizing into wars no one can win.

From that observation, grim but pragmatic, three sectors stand out. They're the ones I expect to shape my portfolio over the decade ahead.

My job here: the thesis for each sector, the names to play it, and why each one earns its place.

Sector 1

The first is the most obvious. Too obvious, on its face: defense.

From 2016 to 2025, global military spending rose 41% in real terms. The military burden reached 2.5% of GDP, the highest since 2009.1 Last year’s NATO summit in The Hague raised the target to 5% of GDP by 2035 (at least 3.5% of it on core defense).2 Europe’s recent Readiness 2030 rearmament plan is designed to mobilize up to €800B.3 The U.S. national-defense 2027 budget request tops $1.5T, the largest request in U.S. history.4

Plenty of billions, plenty of GDP. But the qualitative side matters just as much.

Japan is in the middle of its biggest rearmament since 1945. Turkey is emerging as a military-industrial power. Russia has tipped into a war economy. And the 2027 clock is ticking: the deadline by which Xi has ordered the PLA to be ready for an operation against Taiwan (not an official war date, but close enough to matter).

So far this is first-order analysis. Anyone who regularly reads the right papers gets here. No alpha in that.

(That’s the theory. In practice, I’ve shown plenty of times that the main source of alpha, created or destroyed, has never been the information. It’s who uses it. But I don’t need that argument here.)

Let’s jump straight to the second order: then what?

First point: a budget line is not a cash flow. Any outfit that depends on the government will tell you as much, bitterly.

NATO’s 5% of GDP, Readiness 2030’s €800B, the U.S. national-defense’s $1.5T: these are promises. By definition, a promise is supposed to be unbreakable. In politics, it’s... different.

But a signed contract is a whole different animal. When Finland signed for 64 F-35s in 2022, Lockheed locked in cash flows for decades: deliveries through 2030, so MRO into the 2060s (not all of it; partner contractors take their cut).5

The order book, then, is the buffer against the political cycle. The moment a promise makes it into the order book, it becomes a commitment that will turn into cash flow (though the contract can still be modified, stretched out, even canceled under certain conditions). Watching the order book is therefore the best way to read the sector’s economic reality. And what a reality. The defense backlog has grown for the third straight year (book-to-bill above 1). And combined revenue for the world’s top 100 aerospace and defense groups blew past $1T for the first time in 2025.6

“Fine, okay, this takes a bit more analytical nuance, but nothing earth-shattering either. Still not convinced there’s alpha in it.”

And you’d be right. We’ve still got a few more “then what”s before we get to alpha.

Then what?

The order is only the tip. When Kongsberg sells a NASAMS air-defense system to Denmark for €500M, that €500M is the appetizer.7 The main course is the recurring revenue over the decades that follow: the aftermarket. Decades of recurring revenue, higher-margin than the OEM sale and, above all, non-cyclical. You can defer buying a platform. You don’t defer maintaining a fleet already in service. So a weak order book in any given year has limited impact as long as there’s an installed base to maintain. To sum up: the sector has gone from an industry that sells machines to one that sells “subscriptions” to keep them running.

Then what?

Here we get into a wrinkle you rarely see flagged in sector theses: the shift in the economic unit of recurring revenue. Take a typical MRO invoice from a few years ago: a hydraulic actuator here, a wiring harness there, a set of turbine blades, and so on. Physical parts, plain and simple. They take time, hands and skill to replace. Today, that same invoice can tell a very different story: a mission software update, a threat library subscription, a licensed capability unlock, and so on. Here, once the code is signed off and certified, a few clicks and it's deployed.

We’ve gone from recurring revenue built on hardware and cost-plus contracts to recurring revenue built on electronics and embedded software (physical MRO obviously hasn’t gone away). Investor hats back on: the economic unit of recurring revenue has shifted from tangible assets to intangible ones, with the margin expansion that follows. Code hits margins that metal never will.

Any valuation of the sector has to account for this shift toward non-cyclical, higher-margin recurring revenue. But at best that justifies paying higher multiples. It doesn’t get you to a buy. Where’s the alpha, damn it?!

To find it, let’s recap:

Allocation to the military sector has gone up.

It’s supposed to keep rising, and the only real gauge of that is the order book.

Order books are rising and hit records in 2025.

Those order books are a source of non-cyclical recurring revenue, part of it higher-margin.

Then what?

How do you spot the real winners among all these overflowing order books? Truth is, I’ve already given the answer. Take a few seconds to think about it. Could be fun.

If demand is no longer the constraint, the only thing left is supply. And supply comes down to two questions:

How fast does the company convert its order book into cash flows? (In defense, delay is almost the rule.)

What margin does it make on each unit produced?

The big winners will be the ones that can burn through the order book fast, lean heavily on the aftermarket, and earn the fattest margins there. So a software-led mix (OEM margins are too uniform, and OEM revenue is rarely big enough to matter).

How do you find them, and, above all, at the right price?

Let’s start at the end. Forget the upbeat headlines. As we’ve seen, promises aren’t cash flows, and what little alpha those stories carry has already been scooped up by better-informed players. What we’re after is the bad news. A budget decision postponed. An investment plan scrapped after a change in government, and so on. This is noise. The order books are full, and will stay that way for years. Almost anything that knocks the price down without affecting the order books directly or the company’s ability to convert them efficiently can be read as a buying opportunity.

Okay, that’s the when. Now the what?

Worth your time? Worth someone else's.

The Picks 1

First off, forget the defense majors, even the pure-play defense SaaS names trading at indecent multiples. Alpha lives in small caps almost by definition, and in this case especially in Europe (where the software shift hits hardest).

Unfortunately the sector has already run hard since the Russia-Ukraine war, and today’s micro caps need far more than a sector tailwind to work: an unproven technology, shaky contracts, and so on. So I've set them aside for this sector.

One note that holds for the whole post: I don’t own a single one of these companies. They’re candidates I’m actively tracking to play these sector theses. And for anyone still in doubt: I’m not a financial advisor and this isn’t financial advice. Your money, your judgment, your risks, your returns. The fine print here.

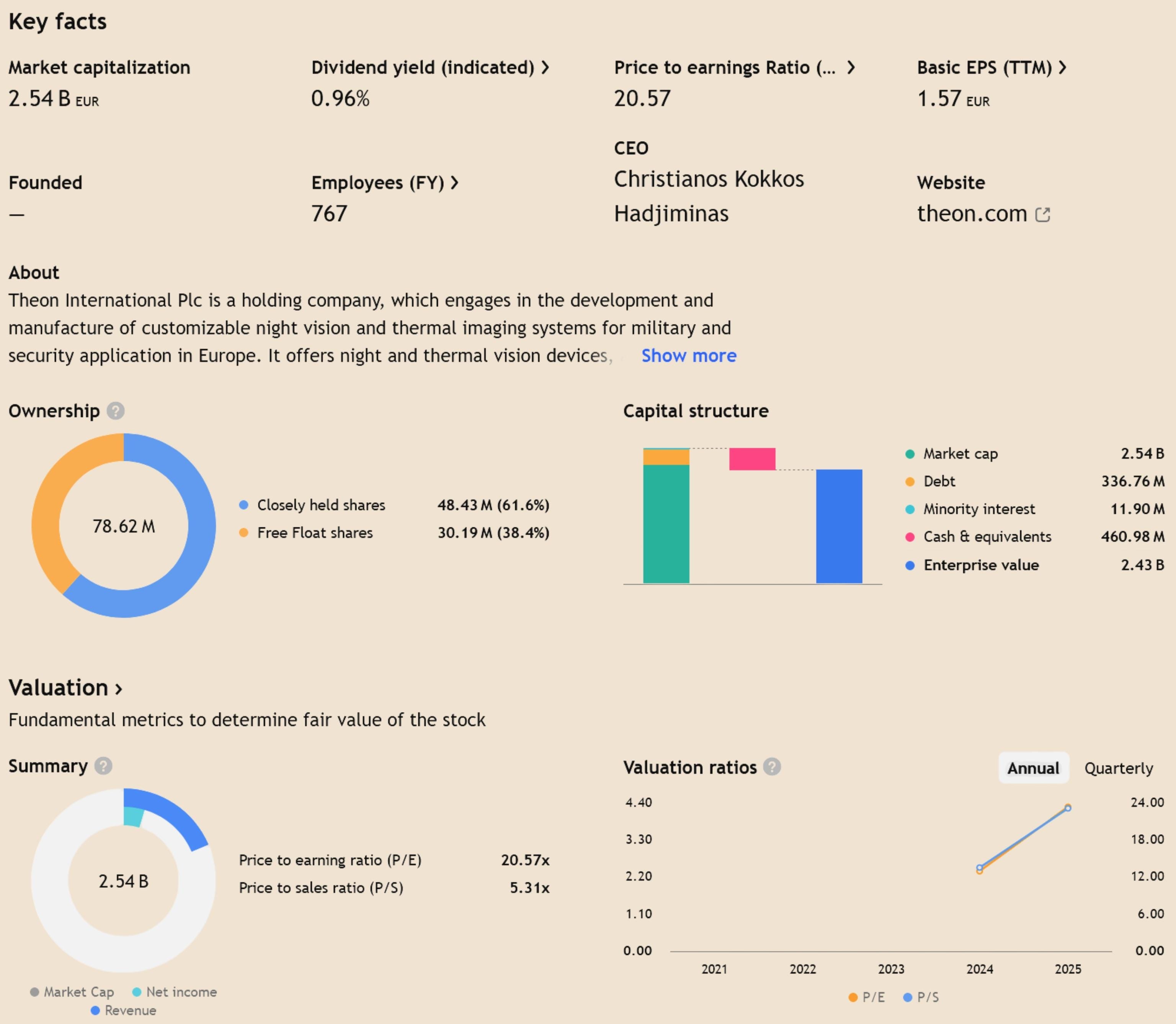

Theon International Plc (EURONEXT:THEON): a bet on the resilience of an exceptional operating margin, with expansion upside from the mix.

In 2025, Theon posted a 26.2% adjusted EBIT margin, high for a company that's still very hardware-heavy. It held that margin even while integrating Harder Digital, a company it acquired to lock in supply of image-intensifier tubes (a critical, supply-constrained component). The legacy business probably runs higher margins than the consolidated figure, though that obviously depends on mix and on the integration. What matters isn't so much the size of the order book as its quality: €2.3B of soft backlog plus options (€1.4B of it pure soft backlog), which gives visibility through 2029.

The real upside is in the mix: the new digital products should more than double in 2026, to roughly 20-25% of revenue, while management targets 20% of revenue from platform products over the medium term. Management has to keep executing, hold the margin on each product, and shift the mix to lift margins overall. The secular trend handles the rest.

At 20x EV/EBITDA and 20x P/E, this isn't a compelling entry (not for me, anyway). The stock is objectively very volatile, so patience stands a good chance of being rewarded.

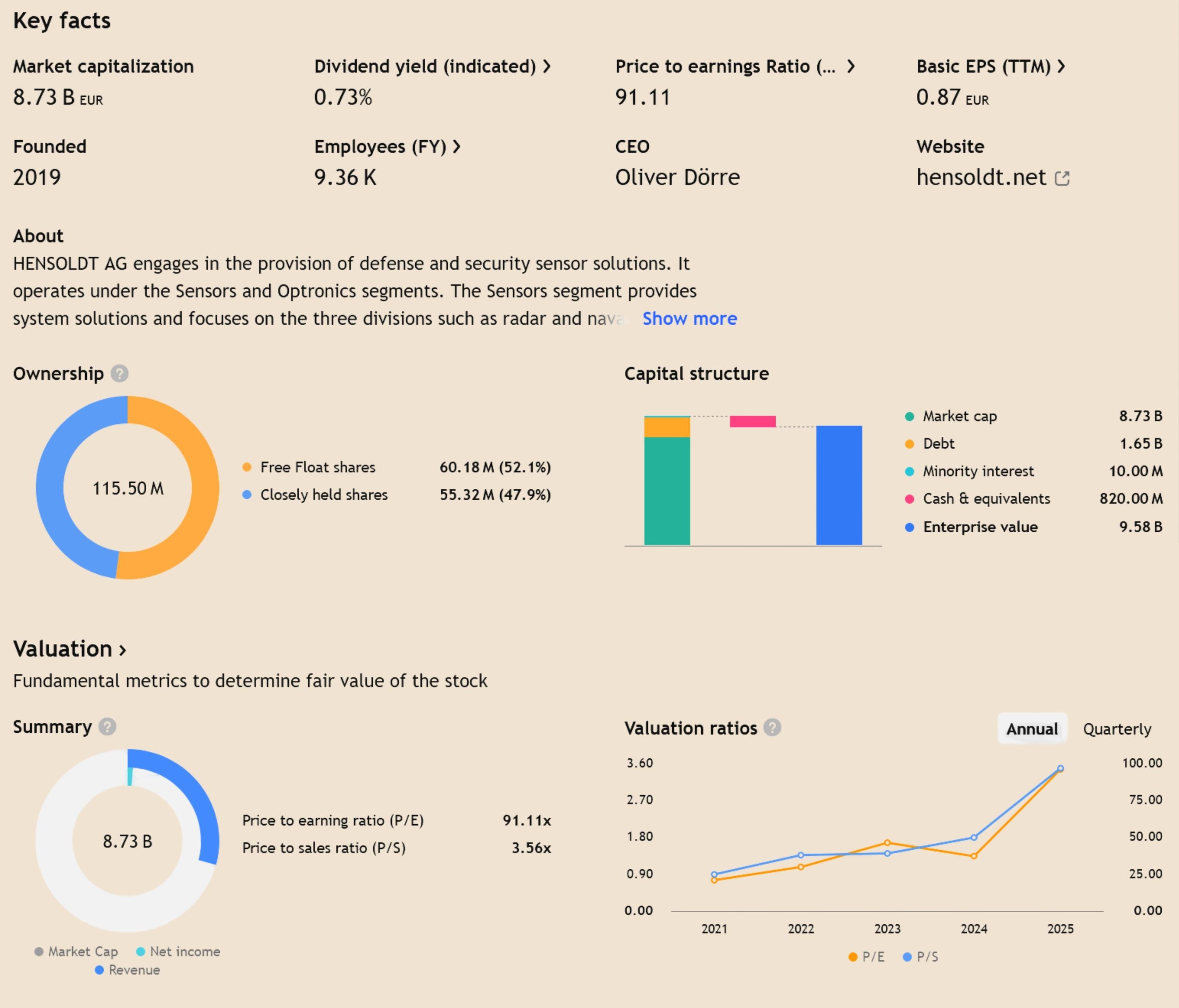

Hensoldt AG (XETR:HAG): a bet on the speed of order-book execution.

The company spans several layers of electronics (radar, optronics, electronic warfare). What we're looking for is self-evident: recurring revenue from upgrades and MRO over long life cycles, layers of software and, of course, analytics.

But what interests me about Hensoldt is its conversion speed. Case in point: book-to-bill jumped to 3x last quarter (guidance is closer to 1.5-2x). Orders are coming in far faster than they turn into revenue, so the whole thesis hinges on that conversion. The 2026 adjusted FCF guidance was raised to 50% of EBITDA, up from 40%. That bump also comes from higher customer prepayments, so it's as much a demand signal as a real conversion gain (assuming the company executes).

The real catch is the price. At 25x EV/EBITDA (18-19x on 2026 TTM), it's objectively still too expensive despite the pullback. But no doubt Mr. Market will hand us better entries.

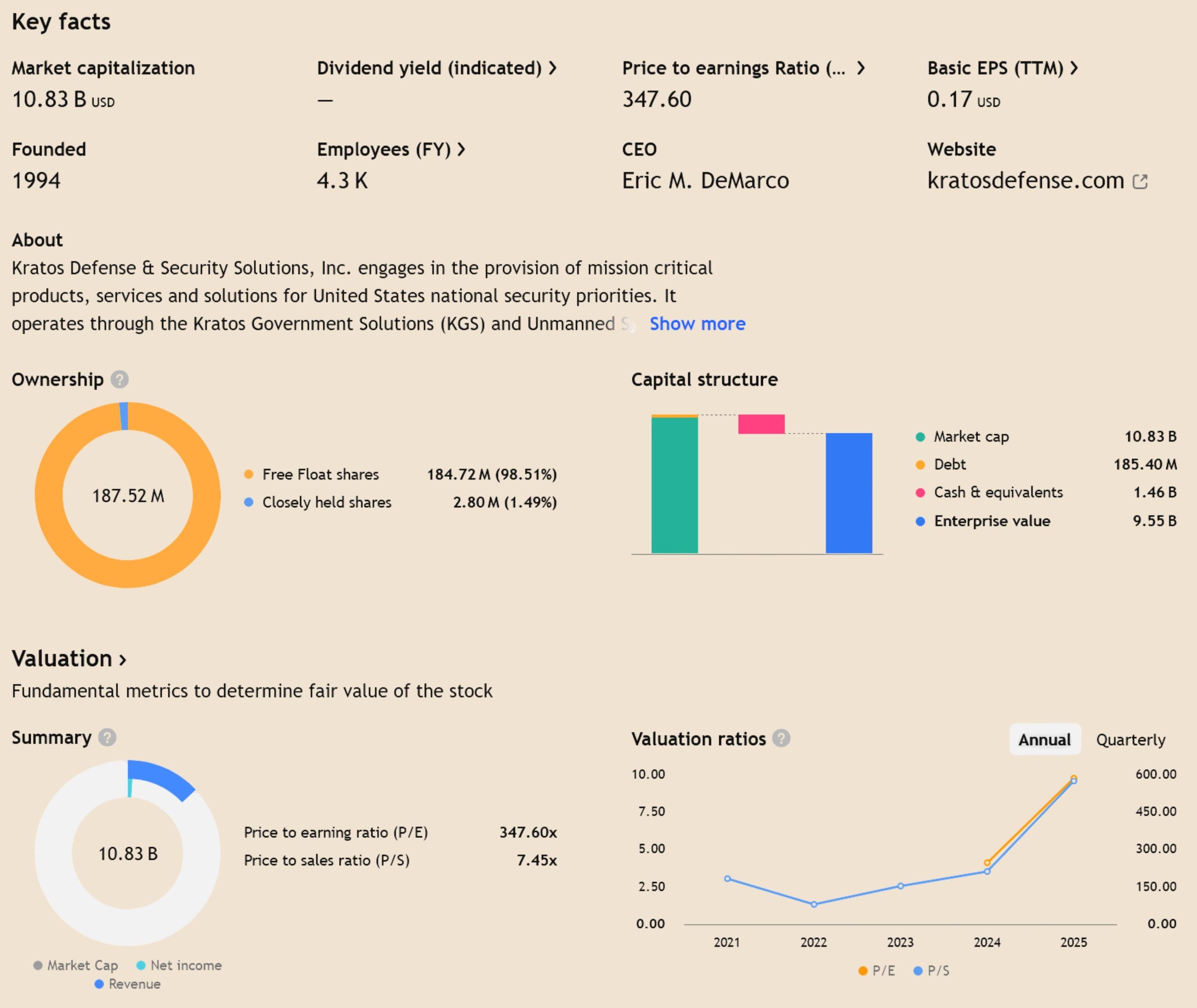

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS): a riskier bet, on execution and margins at once.

Here the starting point is different. The company makes drones, unmanned systems, and propulsion, among other things. It has a clear technological edge. The thesis, if it works, rests on its ability to convert that edge into an installed base, and to turn that base into high-margin recurring revenue.

You can split the company into its two reported segments. Unmanned Systems, about 22% of revenue, home to Valkyrie and the target drones: these are designed to be attritable. Durable recurring-like revenue, if it comes, sits more in parts of the remaining 78%: mainly the ground software that flies the satellites, sold as “software/systems/support,” even if Kratos stays a grab-bag of many other things (and there really are a lot of other things in there; it’s complexity that should widen the margin of safety you demand.)

On the propulsion side, it's a bit trickier: drones and munitions get used up, so they get rebought continuously; once a Kratos engine is qualified on a program, it gets reordered on every production lot for the life of the program. Basically recurring revenue through reorders, just a bit lumpier. For now the EBITDA margin runs around 10%, far from what you'd hope for once the model is at cruising speed. And the cash isn't there yet: management is still guiding to negative FCF of $85-105M in 2026, on $155-165M of CapEx. The potential is enormous, but so are the valuations. I won't even give you the numbers. They're that indecent. Just know that they don't justify risking money on that potential, even factoring in the decade-long tailwind the sector enjoys. But once again, I trust Mr. Market. In the meantime, I'm keeping a close eye on it.

I'll head off the question: I don't see ISSC as a way to play this sector thesis for now. Its military revenue is only about 40% of the total, and its upside in this sector is limited (the F-16 fleet isn't going to double in 10 years). My view could change with the next acquisitions and/or new contracts. Subscribers will be the first to know.

Sector 2

You work at some company... fine, let’s make it a European bank. It’s time for the year-end budget meeting, and neither you nor your colleagues are exactly thrilled. The outlook is grim, and everyone around the table knows cuts are coming.

Every line item goes under the microscope. Cloud migration, pushed back. The two planned hires, frozen. Marketing, it has to come down. Call it 30%. You keep going, line by line, until you hit the IT Security and Compliance lines. Relief, all around. No need to think hard. There’s not much wiggle room here. There are laws, deadlines, audits, and, for good measure, the name of the person sitting at the head of the table on a regulatory filing the day it all breaks. There’s a floor in these lines that’s simply untouchable.

Let’s put some numbers on it anyway.

The global cybersecurity market is $213B in 2025 (the number shifts depending on how you slice it). I find that almost laughably small given the stakes, but reality always gets the last word. It grants me one point, though: double-digit growth, with $322B expected by 2029.8 No surprise there. Attack surfaces multiplying faster than lily pads on a pond, because of (or thanks to) the cloud explosion. Ransomware going industrial. And above all: AI.

AI’s impact on the sector is like handing every primate on earth an AK-47. Suddenly it’s very easy to do serious damage to just about anyone, as long as you’ve got two opposable thumbs.

From an investor’s standpoint: it creates an incentive to attack you, and drastically lowers the barrier to entry (less fun when you put it that way). All it takes is an internet connection and a subscription that runs a few dozen dollars a month. You no longer need to know C/C++ to write polymorphic malware. Learn English to run credible phishing campaigns? Not even necessary anymore. You can even uncover a zero-day without knowing what the term means. A total democratization of offensive cyber, from the total amateur to the totalitarian state (or the less totalitarian one).

This isn’t just theory. Just last year, Anthropic disclosed a large-scale espionage operation (probably Chinese) in which almost the entire attack chain was run by AI, from reconnaissance to exfiltration.9 Nobody knows all the rules of the game, not even governments. To be fair to them, the rules change with every new Claude update.

Let’s put some numbers on AI security: $49B in 2025. That’s peanuts. Though in fairness, that's an easy thing to say a year on, in a world that moves this fast. By 2029, the figure is projected at $160B.10 More than a 3x. Worth noting: it’s easy to slap an “AI” label on a product, and properly counting the cyber tools that are genuinely AI-powered isn’t so simple.

My opening scene “showed” it: you don't slash a cybersecurity line. But there are two ways to bring it down (finer trade-offs aside):

Push out an upgrade.

Cut cyber headcount.

In 2025, 36% of companies reported cuts to their cyber budgets, and a big chunk of those came from cutting headcount (about 2/3 cut their cyber teams).11

AI will hit both of these variables:

As noted, the rapid refresh of AI-enabled offensive capabilities forces an equally rapid refresh of defensive tooling. Those refreshes become recurring revenue, probably high-margin, for the cyber companies.

AI should (the conditional matters here) help shrink companies’ in-house cyber headcount (all else equal), but also, maybe above all, shift the skill profile they hire for. If AI automates the attack, it automates part of the defense, so it calls for a skill set suited to that offense/defense automation. That reduction and that shift should free up more budget for software and infrastructure, most of which ends up in the cyber companies’ P&L. More on that later.

Like defense, cyber is in for major growth. But there are three big differences worth flagging.

First, cyber already runs largely like a recurring-revenue SaaS model. There’s infrastructure, sure, but it’s usually not the bulk of a company’s revenue (worst case, stock picking solves that).

Second, contract execution costs tend to run lower than in defense. A cyber vendor adds a little infrastructure, wires the client’s workflow into the existing tools, and trains a few people. After that, it’s maintenance and monitoring, where margins are generally higher.

Third, the barrier to entry for starting a cybersecurity company has dropped sharply, and it’ll probably keep falling with every big new AI model release.

From all this, one variable stands out, the one that, in my view, separates the big winners in this sector: customer stickiness. Secular growth only really compounds for the companies that can hold on to their customers.

Back to the shortage of talent suited to these changes. In 2025, 95% of companies surveyed reported a skills gap across their cyber teams.12 It’s hard to be any good in a field that moves this fast. It’s also a market need that the cyber companies can, and should, fill.

Put it all together, and the profile of the future winners takes shape: a company anchored in compliance, with enormous customer retention, and able to turn the talent shortage to its own advantage.

I dug in. Found 3 that check every box:

A quasi-monopolistic compounder where stickiness is an understatement.

A banking hardware→software transition already well underway, with supranational regulation strengthening the tailwind.

A sovereign mission-critical niche, obviously very sticky, and accelerating.

Pro subscribers can skip this section and jump straight to the full report below. Signal doesn’t wait.

By going Pro, you get the full post, plus every deep dive, past and future (one to two a month, plus follow-ups). For example:

One undiscovered company at the right price makes the cost of this newsletter trivial.

Become a Pro Member

You can get free access to paid content by sharing this newsletter with your network. Rewards compound:

3 new subscribers = 1 month;

8 new subscribers = 3 months;

15 new subscribers = 6 months.